ADM 3346 Midterm: Notes for Midterm

3 Oct 2017

School

Department

Course

Professor

Document Summary

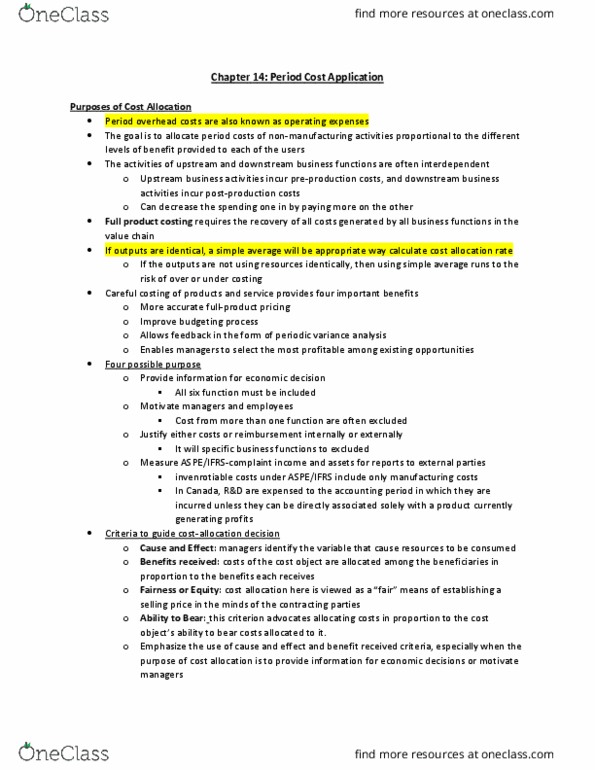

Chapter 2: an introduction to cost terms and purpose. Classifications of manufacturing costs: direct material are the acquisition costs of all material that become part of cost object. Direct and indirect costs: direct costs can be traced to a cost object in a cost-effective way. It can include direct material, direct manufacturing labour and direct non- manufacturing labour or manufacturing costs. Fixed and variable costs: variable costs are costs that remain constant on a per unit basis, fixed costs are costs that remain unchanged in total despite changes in quantity of output units produced. Period and inventoriable costs: period costs is non-production costs, either upstream or downstream of productions, under gaap, period costs are expensed when incurred. If no finished goods are sold, then all manufacturing costs are costs goods available for sale. Inventoriable costs become cost of goods sold when finished goods are sold: only for companies in the manufacturing sector.