AFM479 Study Guide - Final Guide: Credit Event, Credit Risk, Cash Flow

27 Dec 2019

School

Department

Course

Professor

Document Summary

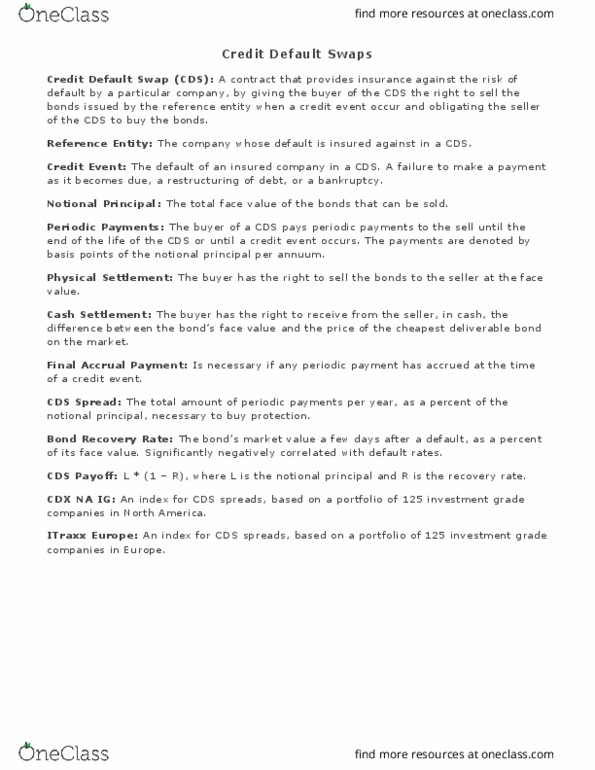

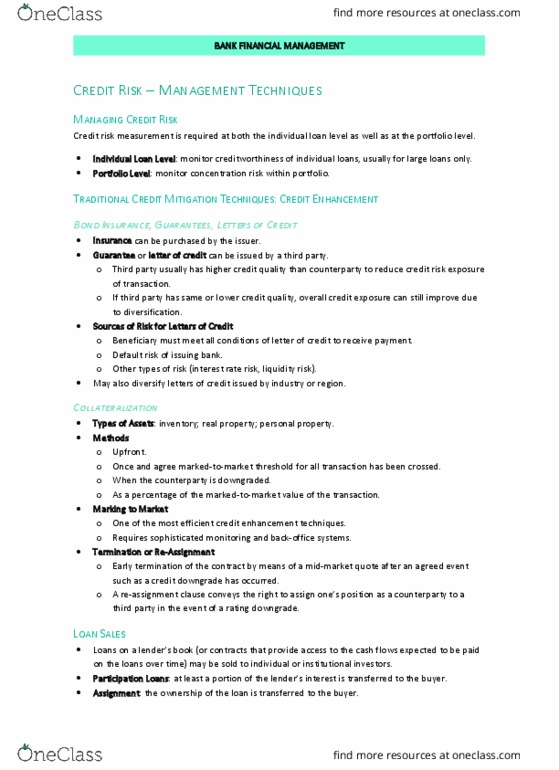

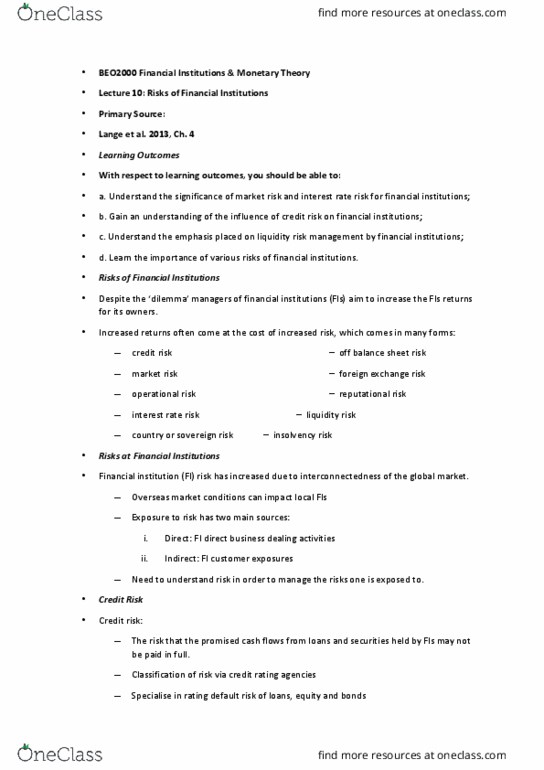

Credit risk: the economic loss suffered due to the default of a borrower or counterparty. Default: failure to fulfill contractual obligations in a timely manner, due to inability or unwillingness. Trading (counterparties, money market, and debt securities) Actions that reduce credit risk: risk-based pricing, transaction collaterals, insurance policies (cds) Principal and interest: banks need to assess the risk of both interest cash flow and the principal. Banks lean on cash flow first and capital second. Expected loss (el): the anticipated average rate of loss that an organization should expect to suffer on its credit risk portfolio over time. Viewed as a cost of doing business, and managed with pricing and general provisions. E(exposure): the expected exposure at the time of the credit event. For loans, usually just the amount of the loan. E(default): the expected frequency of defaults within an overall portfolio , reflecting the underlying credit risks of the borrowers and counterparties.