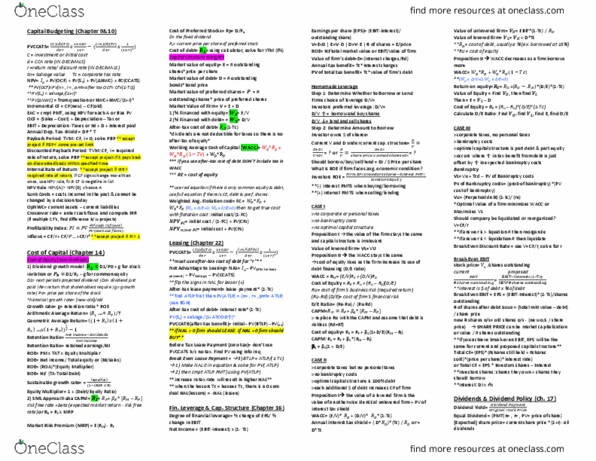

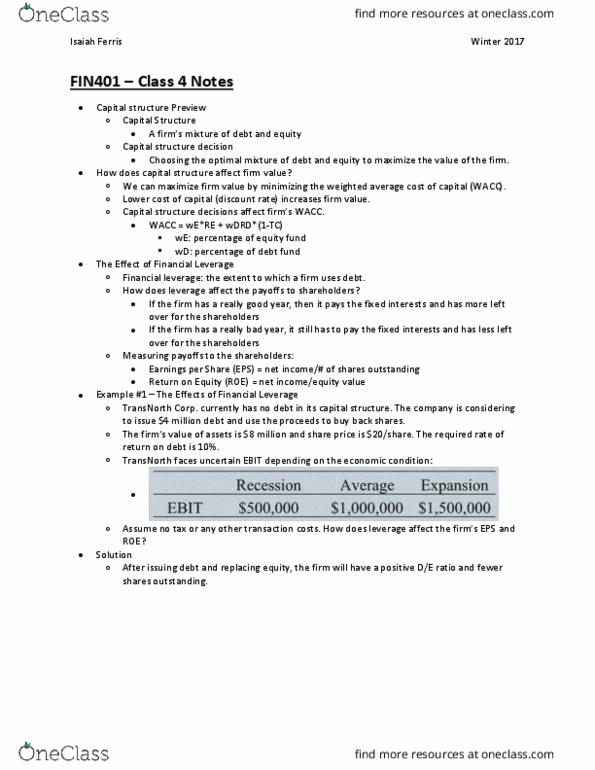

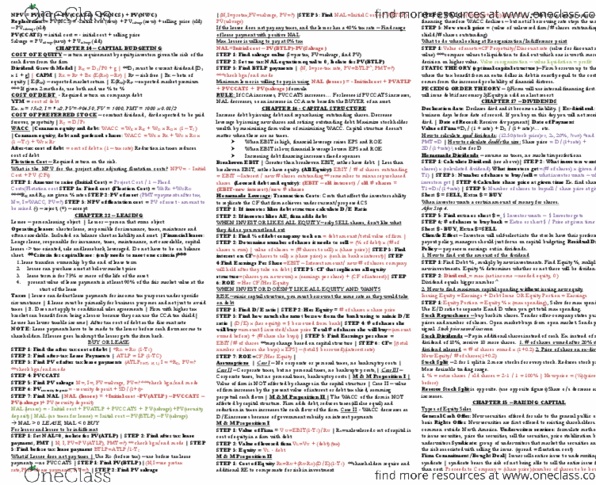

FIN 401 Study Guide - Midterm Guide: Capital Structure, Dividend Policy, Preferred Stock

Document Summary

Get access

Related Documents

Related Questions

Intermediate Financial Management 11th Edition

Chapter 15: Capital Structure Decisions Part 1 Mini Case

Assume you have just been hired as a business manager of PizzaPalace, a regional pizze restaurant chain. The company EBIT was $50 million last year and is not expected to grow. The firm is currently financed with all equity, and it has 10 million shares outstanding. When you took your corporate finance course, your instructor stated that most firms' owners would be financially better off if the firms used some debt. When you suggested this to your new boss, he encouraged you to pursue the idea. As a first step, assume that you obtained from the firm's investment banker the following estimated costs of debt for the firm at different capital structures:

| PERCENT FINANCED WITH DEBT, Wd | rd |

|---|---|

| 0% | - |

| 20 | 8.0% |

| 30 | 8.5 |

| 40 | 10.0 |

| 50 | 12.0 |

If the company were to recapitalize, then debt would be issued and the funds received would be used to repurchase stock. PizzaPalace is in the 40% state-plus-federal corprate tax bracket, its beta is 1.0, the risk free rate is 6%, and the market risk premium is 6%.

Please answer All Parts:

Part A: Provide a brief overview of capital structure effects. Be sure to identify the ways in which capital structure can affect the WACC and free cash flows.

Part B: 1) What is business risk? What factors influence a firm's business risk? 2) What is operating leverage, and how does it affect a firm's business risk? Show the operating breakeven point if a company has fixed costs of $200, a sales price of $15, and variable costs of $10.

Part C: Now, to develop an example that can be presented to PizzaPalace's management to illustrate the effects of financial leverage, consider two hypothetical firms: Firm U, which uses no debt financing, and Firm L, which uses $10,000 of 12% debt. Both firms have $20,000 in assets, a 40% tax rate, and an expected EBIT of $3,000. 1) Construct partial income statements, which start with EBIT, for the two firms. 2) Now calculate ROE for both firms. 3) What does this example illustrate about the impact of financial leverage on ROE?

Part D: Explain the difference between financial risk and business risk.

Part E: What happens to ROE for Firms U and L if EBIT falls to $2,000? What does this imply about the impact of leverage on risk and return?

Part F: What does capital structure theory attempt to do? What lessons can be learned from capital structure theory? Be sure to address the MM models.

Part G: What does the empirical evidence say about capital structure theory? What are the implications for managers?

Part H: With the preceding points in mind, now consider the optimal capital structure for PizzaPalace. 1) For each capital structure under consideration, calculate the levered beta, the cost of equity, and the WACC. 2) Now calculate the corporate value for each capital structure.

Part I: Describe the recapitalization process and apply it to PizzaPalace. Calculate the resulting value of the debt that will be issued, the resulting market value of equity, the price per share, the number of shares repurchased, and the remaining shares. Considering only the capital structures under analysis, what is PizzaPalace's optimal capital structure?

Lampkin Manufacturing Company has two projects. The first, Project A, involves the construction of an addition to the firm's primary manufacturing facility. The plant expansion will add fixed operating costs equal to $200,000 per year and variable costs equal to 20% of sales. Project B, on the other hand, involves outsourcing the added manufacturing to a specialty manufacturing firm in Silicon Valley. Project B has lower fixed costs of only $50,000 per year, and thus lower operating leverage than Project A, while its variable costs are much higher, at 40% of sales. Project A has an initial cost of $3.2 million, while Project B will cost $3.4 million.

When the question arose as to what discount rates the firm should use to evaluate the two projects, Lampkin's CFO, Paul Keown, called his old friend Arthur Laux, who works for Lampkin's investment banker.

Art, we're trying to decide which of two major investments we should understake, and I need your assessment of our firm's capital costs and the debt capacities of both projects. I've asked my assistant to email you descriptions of each. We need to expand the capacity of our manufacturing facility, and these two projects represent very different approaches to accomplishing that task. Project A involves a traditional plant expansion totaling $3.2 million, while Project B relies heavily on outsourcing arrangements and will cost us a little more up front, $3.4 million, but will have much lower fixed operating costs each year. What I want to know is, How much debt can we use to finance each project without putting our credit rating in jeopardy? I realize that this is a very subjective thing, but I also know that you have some very bright analysts who can provide us with valuable insight.

Art replied:

Paul, I've got suggestions for you regarding the debt-carrying capacity of your projects and current capital costs for Lampkin. Our guys think that you've probably got room for about $1,200,000 in new borrowing if you do the traditional plant expansion project (Project A). If you decide on Project B, we estimate that you could borrow up to $2,400,000 without realizing serious pressure from the credit rating angencies. If the credit angencies cooperate as expected, we can place that debt for you with a yeild of 5%. Our analysts also did a study of your firm's cost of equity and estimate that it is about 10% right now. SHOW ALL WORK, ANSWER BOTH A AND B

A) Assuming that Lampkin's investment banker is correct, use book value weights to estimate the project-specific cost of capital for the two projects. (Hint: The only difference in the WACC calculations relates to the debt capacities for the two projects. Also, the firm's tax rate is 35%).

B) How would your analysis of project-specific WACCs be affected if Lamkin's CEO decided that he wanted to delever the firm by using equity to finance the better of the two alternatives (Project A or Project B)?

| Cost of equity | 10% |

| Cost of debt | 5% |

| Tax rate | 35% |

| Project A (expand) | |

| Up-front initial investment | $3,200,000 |

| Annual fixed costs | $200,000 |

| Variable costs | 20% |

| Contribution margin | 80% |

| Degree of Operating Leverage | high |

| Debt capacity | $1,200,000 |

| Debt to value ratio at capacity | ? |

| Project WACC | ? |

| Project B (outsource) | |

| Up-front intitial investment | $3,400,000 |

| Annual fixed costs | $50,000 |

| Variable costs | 40% |

| Contribution margin | 60% |

| Degree of Operating Leverage | low |

| Debt capacity | $2,400,000 |

| Debt to value ratio at capacity | ? |

| Project WACC | ? |

1a- What are the direct costs and indirect costs of financial distress, from default that leads to bankruptcy? Explain in a well-stated description and discussion, not over a page in length.

1b- What are the impacts of the following on BECA Corporation's value, given the following information? SHOW ALL CALCULATIONS, and make a summary about the impact on equity owners between leveraged and unleveraged capital structures, and the impact on firm value from Financial Distress Costs.

BECA Corporation faces an uncertain future in a challenging business environment. Due to increased competition from foreign imports, its revenues have fallen dramatically in the past year. BECA's managers hope that a new product in the company's pipeline of new products will restore its fortunes. While the new product represents a significant advance over BECA's competition, whether that product will be a hit with consumers remains uncertain. If it is a hit, revenues and profits will grow, and BECA will be worth $200 million at the end of the year. If it fails, BECA will be worth only $130 million at the end of the year.

BECA Corporation may employ one of two alternative capital structures at the beginning of the year to provide the funding for this new project: (1) it can use all equity financing or (2) it can use debt that matures at the end of the year with a total of $150 million due.

Look first at the consequences of these capital structures when the new product succeeds, and when the new product fails, in a setting of perfect capital markets. Calculate what the debt and equity values will be for success and for failure, in both the unlevered and levered capital structures, at the end of the year. Show the totals to all investors (debt + equity) as well.

Now, since it has been assumed that BECA Corporation is operating in a perfect capital market, according to the M&M Proposition I, the investors (debt and equity total) will NOT be worse off because BECA may have some leverage at the beginning of the year. In other words, the value of BECA will be the same whether it has incurred the $150M of debt or not.

So, you are to show if that is indeed the case for BECA Corporation, under the following scenario.

Suppose the risk-free rate is 5%, and BECA's new product is equally likely to succeed or to fail. For simplicity, suppose that BECA's cash flows are unrelated to the state of the economy (i.e., the risk is diversifiable), so that the project has a Beta coefficient of 0 and the cost of capital is the risk-free rate. Compute the value of BECA's securities (that means both debt and equity, as applicable) at the beginning of the year with and without the $150M debt, and show whether or not the M&M Proposition I holds. That is, show if the value of the securities with or without leverage (the debt of $150M) have the same total value or not.

Now, to "get at" the value, VL or VU of the BECA Corporation, you have to discount the value of the cash flows to investors, per equation 9.23 in Chapter 9. But, what you need to know about the M&M Propositions is they assumed that the entire earnings (EBIT) in each year are paid out to the shareholders in the form of dividends or to the debtholders in the form of interest. So, regardless, the owners of the firm receive all the cash flows. So, for equation 9.23, you only have one year of FCFs, and the discount rate is 5%. What is the FCF? Since it is all of the cash flows with no taxes existing, and all of it is paid out to the equity and debt holders in a perfect capital market, what you find out is that the numerator is nothing more than the equity or debt values you calculated above. This is illustrated in Example 16.1 on page 554 of the texbook (I just provided an explanation of why the equity and debt values are used in the numerator instead of cash flows...in this case, they are the same).

2.Suppose you are a rational investor and looking at the following tax rates:

|

(The 2012 tax rates were revised in 2013 by the U.S. Congress, and signed into law by the President, but that is for information only). The tax rates shown are for financial assets held for one year or more. For assets held less than one year, capital gains are taxed at the ordinary income tax rate (currently 35% for the highest bracket); the same is true for dividends if the assets are held for less than 61 days.

Your assignment: What is the effective dividend tax rate for a buy and hold individual investor in 2006 ?

Show all of your calculations.