MAA103 Study Guide - Final Guide: Quick Ratio, Accounts Receivable, Profit Margin

Document Summary

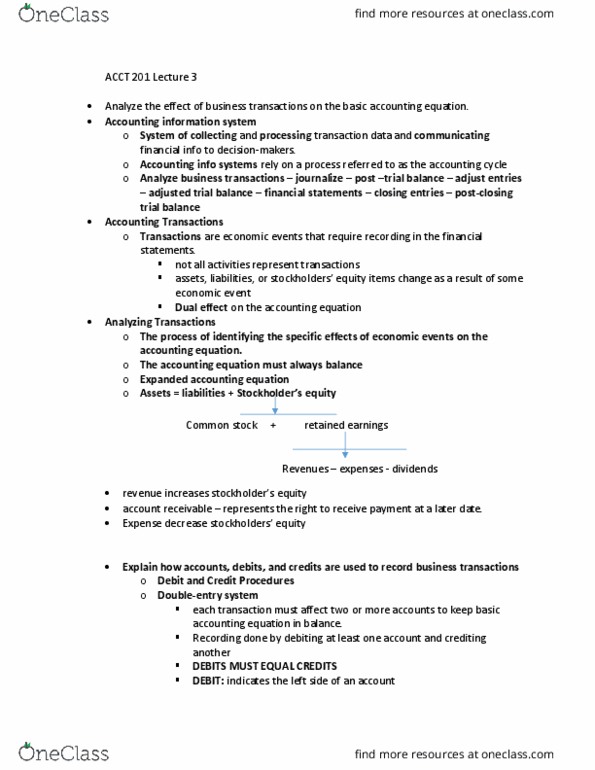

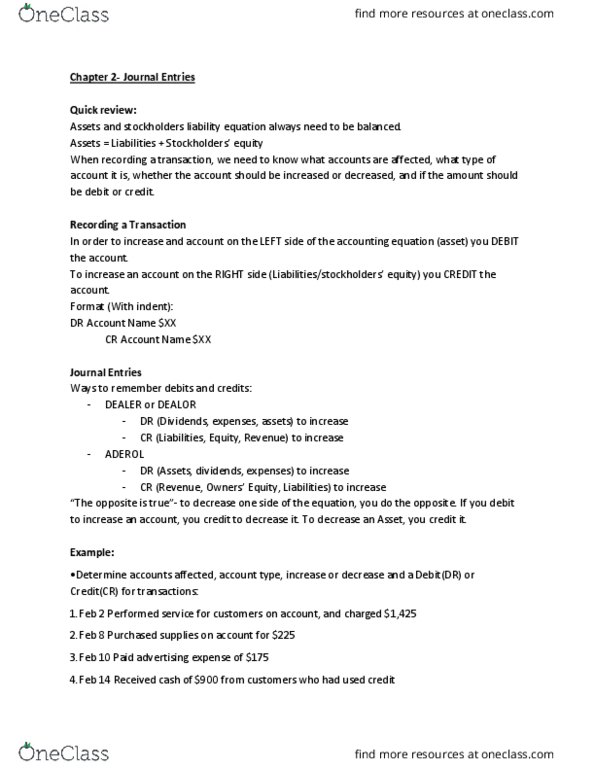

As accounting methods have progressed alongside the use of technology, the need for regulatory processes and monitoring methods in order to ensure all entities are following the laws have also increased. This means regulations must change to account for the different technologies and regulatory bodies must be more informed on its use. This will assist in not only the legalities of accounting but the prevention of financial failure and corporate collapses. A reporting entity is any business or company that is required to provide and create financial statements to the ato. O(cid:374) a (cid:272)ash at (cid:271)a(cid:374)k o(cid:396) (cid:858)t a(cid:272)(cid:272)ou(cid:374)t(cid:859), all de(cid:271)its (cid:894)d (cid:895) i(cid:374)(cid:272)u(cid:396)(cid:396)ed a(cid:396)e pla(cid:272)ed o(cid:374) the left, (cid:449)hilst all c(cid:396)edit(cid:859)s (cr) incurred are placed on the right. Debit (dr): increased by assets, decreased (cid:271)(cid:455) lia(cid:271)ilities a(cid:374)d o(cid:449)(cid:374)e(cid:396)(cid:859)s e(cid:395)uit(cid:455) C(cid:396)edit (cid:894)c (cid:895): i(cid:374)(cid:272)(cid:396)eased (cid:271)(cid:455) o(cid:449)(cid:374)e(cid:396)(cid:859)s e(cid:395)uit(cid:455) a(cid:374)d lia(cid:271)ilities, a(cid:374)d de(cid:272)(cid:396)eased (cid:271)(cid:455) assets. This maintains the accounting equation of assets = lia(cid:271)ilities + o(cid:449)(cid:374)e(cid:396)(cid:859)s e(cid:395)uit(cid:455).