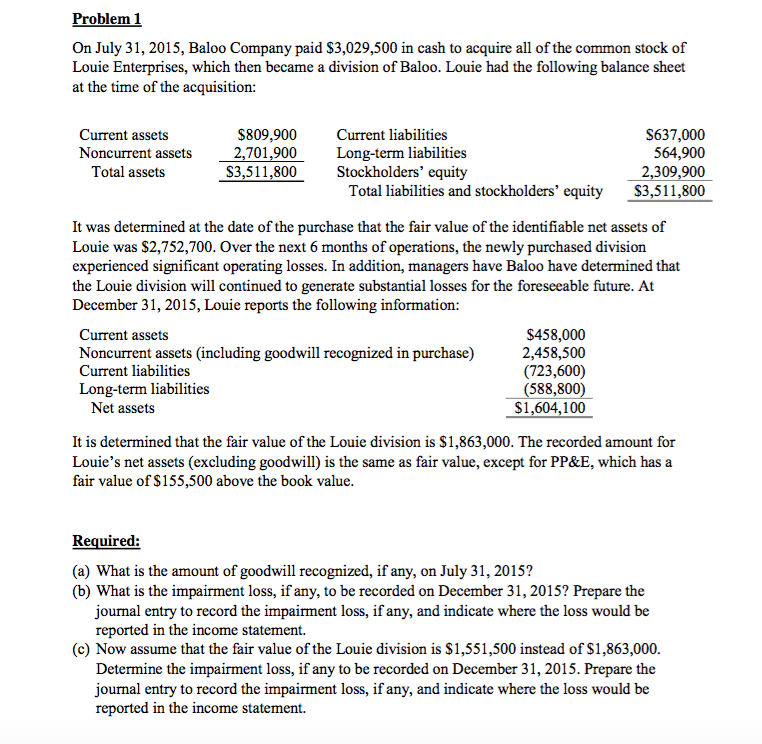

On July 31, 2015, Baloo Company paid $3,029,500 in cash to acquire all of the common stock of Louie Enterprises, which then became a division of Baloo. Louie had the following balance sheet at the time of the acquisition: It was determined at the date of the purchase that the fair value of the identifiable net assets of Louie was $2,752,700. Over the next 6 months of operations, the newly purchased division experienced significant operating losses. In addition, managers have Baloo have determined that the Louie division will continued to generate substantial losses for the foreseeable future. At December 31, 2015, Louie reports the following information: It is determined that the fair value of the Louie division is $1,863,000. The recorded amount for Louie's net assets (excluding goodwill) is the same as fair value, except for PP&E, which has a fair value of $155,500 above the book value. Required: What is the amount of goodwill recognized, if any, on July 31, 2015? What is the impairment loss, if any, to be recorded on December 31, 2015? Prepare the journal entry to record the impairment loss, if any, and indicate where the loss would be reported in the income statement. Now assume that the fair value of the Louie division is $1,551,500 instead of $1,863,000. Determine the impairment loss, if any to be recorded on December 31, 2015. Prepare the journal entry to record the impairment loss, if any, and indicate where the loss would be reported in the income statement.

Show transcribed image textOn July 31, 2015, Baloo Company paid $3,029,500 in cash to acquire all of the common stock of Louie Enterprises, which then became a division of Baloo. Louie had the following balance sheet at the time of the acquisition: It was determined at the date of the purchase that the fair value of the identifiable net assets of Louie was $2,752,700. Over the next 6 months of operations, the newly purchased division experienced significant operating losses. In addition, managers have Baloo have determined that the Louie division will continued to generate substantial losses for the foreseeable future. At December 31, 2015, Louie reports the following information: It is determined that the fair value of the Louie division is $1,863,000. The recorded amount for Louie's net assets (excluding goodwill) is the same as fair value, except for PP&E, which has a fair value of $155,500 above the book value. Required: What is the amount of goodwill recognized, if any, on July 31, 2015? What is the impairment loss, if any, to be recorded on December 31, 2015? Prepare the journal entry to record the impairment loss, if any, and indicate where the loss would be reported in the income statement. Now assume that the fair value of the Louie division is $1,551,500 instead of $1,863,000. Determine the impairment loss, if any to be recorded on December 31, 2015. Prepare the journal entry to record the impairment loss, if any, and indicate where the loss would be reported in the income statement.

It was determined at the date of the purchase that the fair value of the identifiable net assets of Conchita was $2,500,000. Over the next 6 months of operations, the newly purchased division experienced operating losses. In addition, it now appears that it will generate substantial losses for the foreseeable future. At December 31, 2017, Conchita reports the following balance sheet information.

Current assets

$470,000

Noncurrent assets (including goodwill recognized in purchase)

2,360,000

Current liabilities

(620,000

)

Long-term liabilities

(420,000

)

Net assets

$1,790,000

It is determined that the fair value of the Conchita Division is $1,850,000. The recorded amount for Conchitaâs net assets (excluding goodwill) is the same as fair value, except for property, plant, and equipment, which has a fair value $110,000 above the carrying value.

Determine the impairment loss, if any, to be recorded on December 31, 2017.