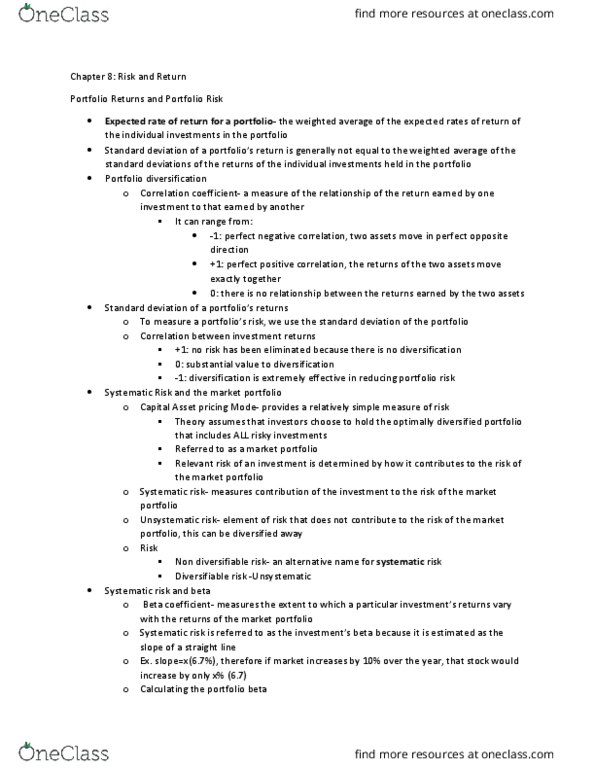

QUESTION 17

Unsystematic risk:

A. can be effectively eliminated through portfolio diversification.

B. is compensated for by the risk premium.

C. is measured by beta.

D. cannot be avoided if you wish to participate in the financial markets.

E. All of the above.

3 points

QUESTION 18

The diversification effect of a portfolio of two stocks:

A. increases as the correlation between the stocks declines.

B. increases as the correlation between the stocks rises.

C. decreases as the correlation between the stocks rises.

D. Both A and C.

E. None of the above.

3 points

QUESTION 19

Irene Adler is considering investing in the common stock of Holmes and Watson. The following data are available for the two securities.

................... Expected Return ..... Standard Deviation

Holmes .............. 0.12 ......................... 0.08

Watson ............. 0.19 .......................... 0.25

If she invests 60% of her funds Holmes and 40% in Watson, and if the correlation of returns between these two securities is 0.45, what is the portfolioâs expected return and standard deviation?

A. 14.8% and 12.89%

B. 13.6% and 11.03%

C. 14.6% and 13.94%

D. 14.4% and 11.03%

E. 13.21% and 10.08%

QUESTION 17

Unsystematic risk:

| A. | can be effectively eliminated through portfolio diversification. | |

| B. | is compensated for by the risk premium. | |

| C. | is measured by beta. | |

| D. | cannot be avoided if you wish to participate in the financial markets. | |

| E. | All of the above. |

3 points

QUESTION 18

The diversification effect of a portfolio of two stocks:

| A. | increases as the correlation between the stocks declines. | |

| B. | increases as the correlation between the stocks rises. | |

| C. | decreases as the correlation between the stocks rises. | |

| D. | Both A and C. | |

| E. | None of the above. |

3 points

QUESTION 19

Irene Adler is considering investing in the common stock of Holmes and Watson. The following data are available for the two securities.

................... Expected Return ..... Standard Deviation

Holmes .............. 0.12 ......................... 0.08

Watson ............. 0.19 .......................... 0.25

If she invests 60% of her funds Holmes and 40% in Watson, and if the correlation of returns between these two securities is 0.45, what is the portfolioâs expected return and standard deviation?

| A. | 14.8% and 12.89% | |

| B. | 13.6% and 11.03% | |

| C. | 14.6% and 13.94% | |

| D. | 14.4% and 11.03% | |

| E. | 13.21% and 10.08% |

Related questions

1. You wish to invest in a portfolio of stocks A (50%) and B (50%). The risk free rate is 4%.

A B

Expected return (%) 10 20

Beta 1.2 1.8

Correlation coefficient between returns 0.3

Whatâs the portfolio return? (In percent without % sign, E.g. 33)

2. Whatâs the portfolio beta in Question 1?

3. The risk reduction through diversification in a portfolio of two stocks

| a. | decreases as the correlation between the stocks rises. |

| b. | (Not enough information.) |

| c. increases as the correlation between the stocks declines. |

| d. (Both statements are correct.) |