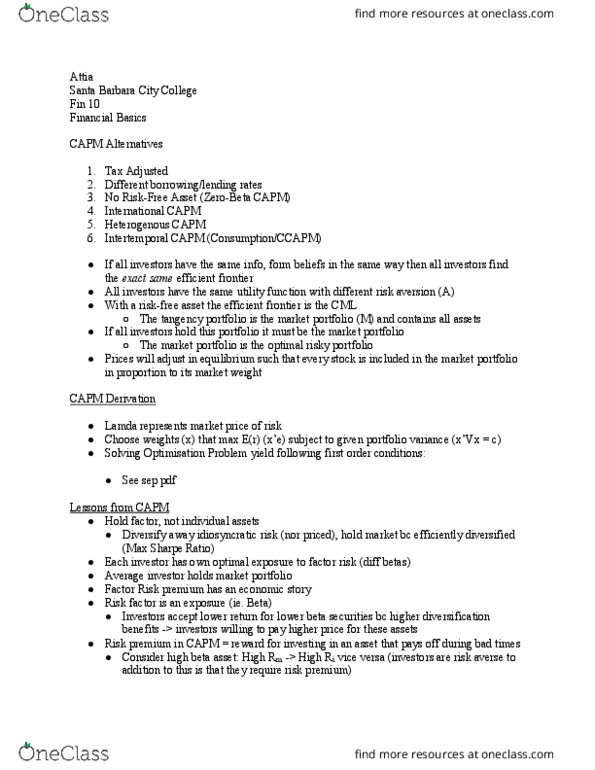

You manage a $20M mutual fund that has a beta of 1.40 and a 10.30% expected return. The risk-free rate is 3.30%. You now receive an additional $5M, which you invest in stocks with an average beta of 0.80. The expected return of the new portfolio is _________%

You manage a $20M mutual fund that has a beta of 1.40 and a 10.30% expected return. The risk-free rate is 3.30%. You now receive an additional $5M, which you invest in stocks with an average beta of 0.80. The expected return of the new portfolio is _________%

Related questions

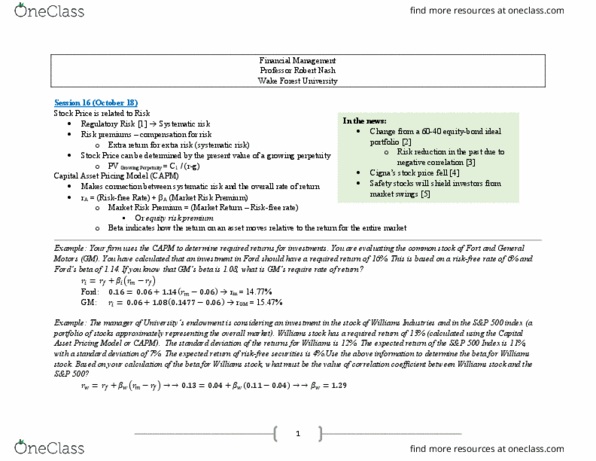

| A mutual fund manager expects her portfolio to earn a rate of return of 10% this year. The beta of her portfolio is .7. The rate of return available on risk-free assets is 4% and you expect the rate of return on the market portfolio to be 14%. |

| What expected rate of return would you demand before you would be willing to invest in this mutual fund? (Do not round intermediate calculations. Enter your answer as a whole percent.) |

| Expected rate of return | % |

| Is this fund attractive to you? | ||||

|

A mutual fund manager expects her portfolio to earn a rate of return of 14% this year. The beta of her portfolio is .9. Assume rate of return available on risk-free assets is 6% and you expect the rate of return on the market portfolio to be 16%.

| a. | Calculate the expected rate of return that investors will demand of the portfolio. |

| Expected rate of return | % |

| b. | Should you invest in this mutual fund? | ||||

|