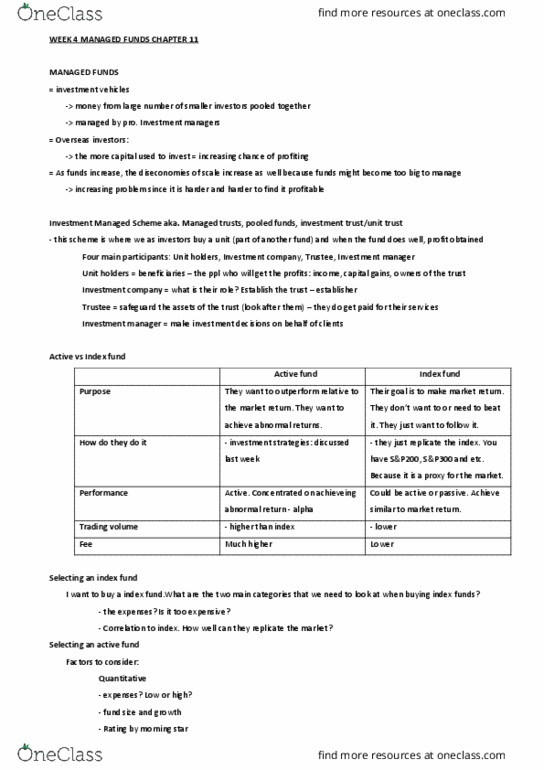

1

answer

0

watching

427

views

26 Feb 2019

here are the alphas and betas for intel and conagra for the 60 months ending april 2009. alpha is expressed as a percent per month. explain how these estimates would be used to calculate an abnormal return.

Alpha Beta

Intel

here are the alphas and betas for intel and conagra for the 60 months ending april 2009. alpha is expressed as a percent per month. explain how these estimates would be used to calculate an abnormal return.

Alpha Beta

Intel

Patrina SchowalterLv2

28 Feb 2019