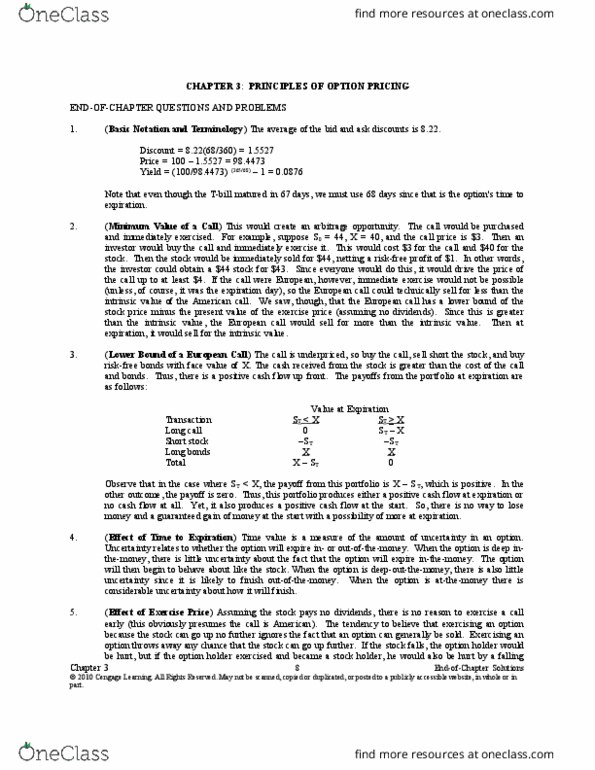

An investor executed an arbitrage trade three month ago by selling a protective put and buying a fiduciary call. At expiration, the stock price was below the same strike price of the call and put options involved in the trade.

At expiration, to close out all positions, the investor will:

A receive a bond payoff, buy stock via the call option, and deliver the stock to settle a short stock position.

B receive a bond payoff, buy stock via the put option, and deliver the stock to settle a short stock position.

C sell stock via the call option, and then take proceeds from stock sale to pay off the risk-free loan.

D sell stock via the put option, and then take proceeds from stock sale to pay off the risk-free loan.

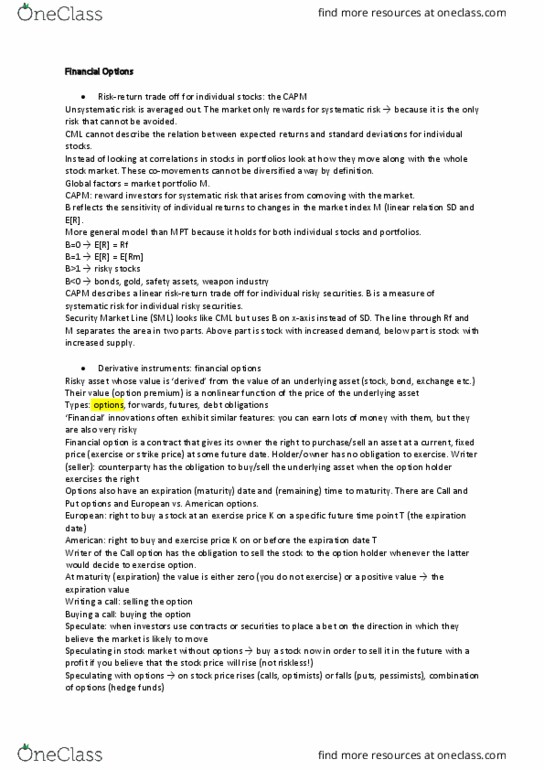

An investor executed an arbitrage trade three month ago by selling a protective put and buying a fiduciary call. At expiration, the stock price was below the same strike price of the call and put options involved in the trade.

At expiration, to close out all positions, the investor will:

| A | receive a bond payoff, buy stock via the call option, and deliver the stock to settle a short stock position. |

| B | receive a bond payoff, buy stock via the put option, and deliver the stock to settle a short stock position. |

| C | sell stock via the call option, and then take proceeds from stock sale to pay off the risk-free loan. |

| D | sell stock via the put option, and then take proceeds from stock sale to pay off the risk-free loan. |

Related questions

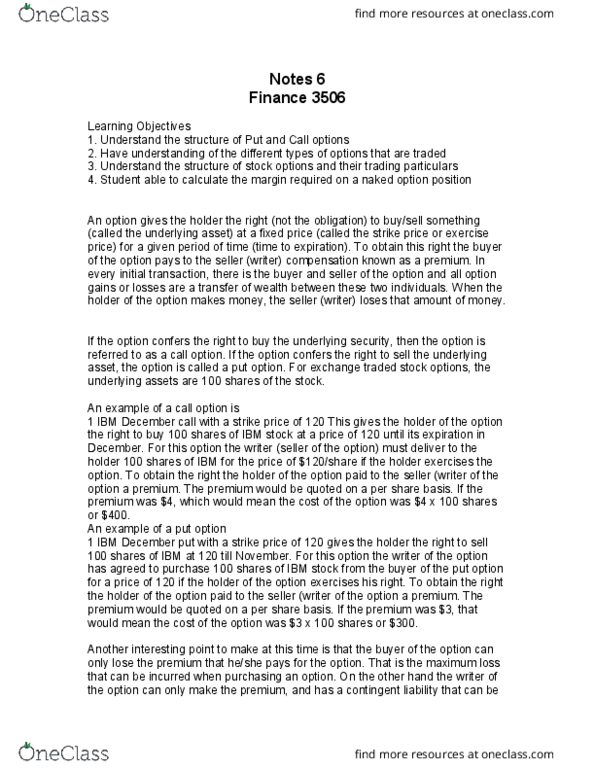

Consider a single-stock futures contract on Wal-Mart common stock. Assume that no dividends will be paid until after the expiration of the futures contract. Consider the following scenario:

Continuously compounded, annualized risk-free interest rate: r = 5%.

Current spot price of Wal-Mart stock: $65 per share.

Futures price on Wal-Mart single-stock futures: $65 per share.

Contract expiration: T = 0.25 year.

Does a risk-free arbitrage opportunity exist? If so, what is the basic strategy?

| a.) No arbitrage opportunity exists at the moment. |

| b.) | Yes. Buy Wal-Mart stock, invest at the risk-free rate, and enter a long position in Wal-Mart single-stock futures. |

| c.) | Yes. Take a loan at the risk-free rate, buy Wal-Mart stock, and enter a short position in Wal-Mart single-stock futures. |

| d.) | Yes. Sell Wal-Mart stock short, invest the proceeds at the risk-free rate, and enter a long position in Wal-Mart single-stock futures. |

| e.) | Yes. Take a loan at the risk-free rate, sell Wal-Mart stock short, and enter a short position in Wal-Mart single-stock futures. |