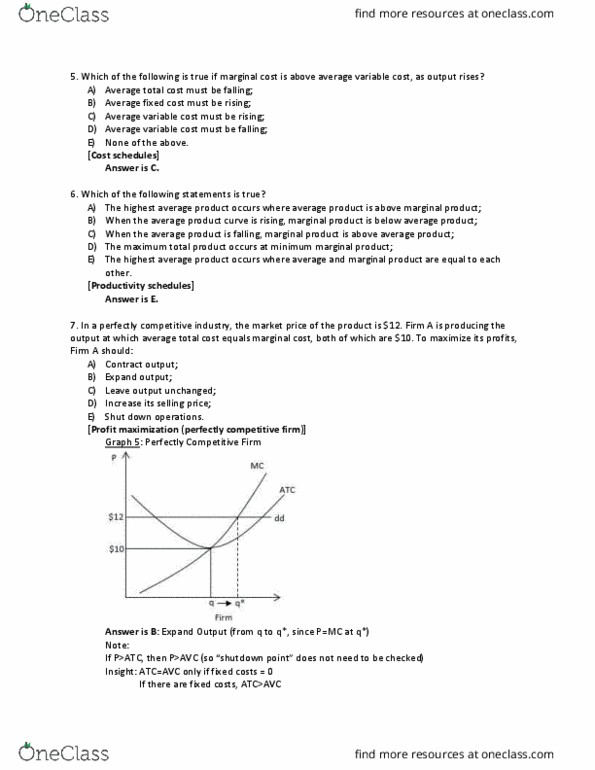

1. In a perfectly competitive industry, the market price is $30. A firm is currently producing 15,000 units of output, its short-run average total cost is $28, its marginal cost is $20, and its average variable cost is $20. Given these facts, explain whether the following statements are true or false or indeterminate at its current rate of production. Please be sure to explain why â not just that the statement is true or false

a. The firm is currently producing the profit maximizing quantity.

b. The firm should produce more output to maximize its profit/minimize its loss.

c. The firm has fixed cost of $20 per unit.

d. The firm is earning a normal profit.

e. The firm is operating in the long run.

f. Draw the graph for the firm and label all of the curves â donât forget the demand and MR curves.

Hint: You should assume normal U-shaped cost curves for this problem.

1. In a perfectly competitive industry, the market price is $30. A firm is currently producing 15,000 units of output, its short-run average total cost is $28, its marginal cost is $20, and its average variable cost is $20. Given these facts, explain whether the following statements are true or false or indeterminate at its current rate of production. Please be sure to explain why â not just that the statement is true or false

a. The firm is currently producing the profit maximizing quantity.

b. The firm should produce more output to maximize its profit/minimize its loss.

c. The firm has fixed cost of $20 per unit.

d. The firm is earning a normal profit.

e. The firm is operating in the long run.

f. Draw the graph for the firm and label all of the curves â donât forget the demand and MR curves.

Hint: You should assume normal U-shaped cost curves for this problem.