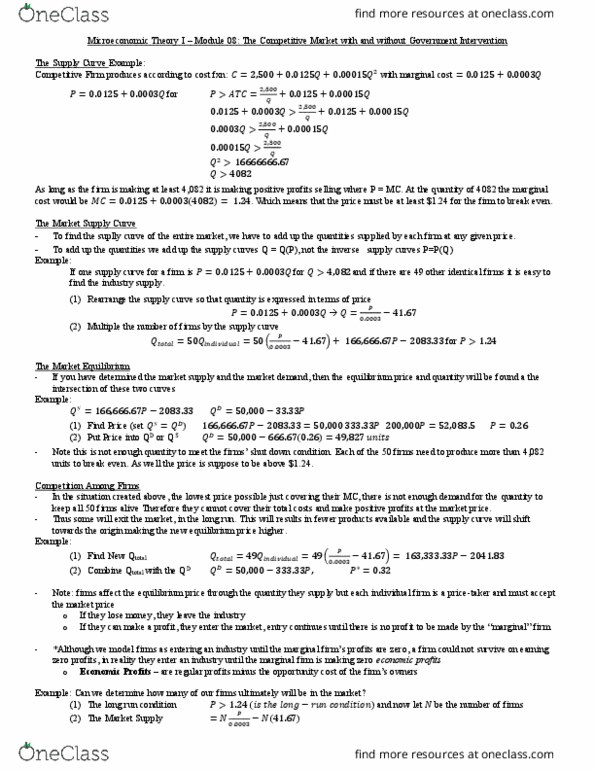

Long-Run Market Equilibrium.

Suppose that in a particular perfectly competitive industry, the technology is characterized by the total cost function:

TC (Q) = 100 + 3Q + (Q^2/25)

*Remember the derivative of a function of the form.

This implies that the marginal cost function is given by MC (Q) = 3 + 2Q/25. Firms incur the fixed cost of 100 only if they enter the industry (or remain in the industry). Suppose that demand for the product is given by D = 200(10 â P) then suddenly shifts to D = 200(13.5 â P). Briefly describe in words what happens to price, quantity, firm profits and number of firms in the market in each scenario:

The short-term, where firms can neither change their quantities nor enter or exit the market.

The medium-term, where firms can change their quantities but cannot enter or exit the market.

The long-term, where firms can change their quantities and can also enter or exit the market.

Long-Run Market Equilibrium.

Suppose that in a particular perfectly competitive industry, the technology is characterized by the total cost function:

TC (Q) = 100 + 3Q + (Q^2/25)

*Remember the derivative of a function of the form.

This implies that the marginal cost function is given by MC (Q) = 3 + 2Q/25. Firms incur the fixed cost of 100 only if they enter the industry (or remain in the industry). Suppose that demand for the product is given by D = 200(10 â P) then suddenly shifts to D = 200(13.5 â P). Briefly describe in words what happens to price, quantity, firm profits and number of firms in the market in each scenario:

The short-term, where firms can neither change their quantities nor enter or exit the market.

The medium-term, where firms can change their quantities but cannot enter or exit the market.

The long-term, where firms can change their quantities and can also enter or exit the market.