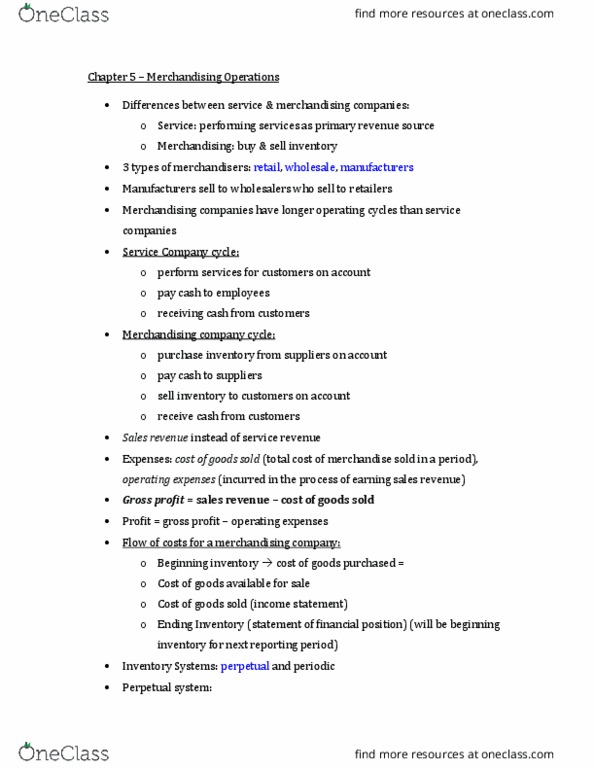

1

answer

0

watching

167

views

15 Jul 2018

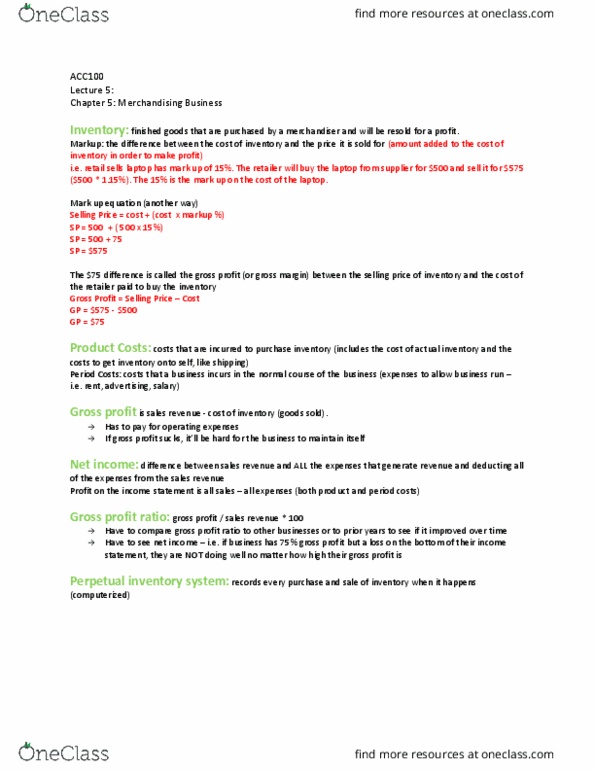

1. What is the differencebetween inventory and cost of goods sold? Cost of goods sold andsales revenue?

2. Is gross profit an account?

3. ComstockCompany counted their inventory at the end of the year and had 220units. Included in that amount were 20 units Comstock held onconsignment from Davidson Inc. Comstock purchased 50 units ofinventory on December 27, FOB shipping point. How many units ofinventory should Comstock report on its year-end balancesheet?

4. Assume Comstock wasunable to count its ending inventory because it was destroyed in afire. Use the gross profit method to estimate the ending inventory.The gross profit rate is 52%.

Beginninginventory

Endinginventory

Netpurchases

Net sales

$ 10,000

?

110,000

175,000

1. What is the differencebetween inventory and cost of goods sold? Cost of goods sold andsales revenue?

2. Is gross profit an account?

3. ComstockCompany counted their inventory at the end of the year and had 220units. Included in that amount were 20 units Comstock held onconsignment from Davidson Inc. Comstock purchased 50 units ofinventory on December 27, FOB shipping point. How many units ofinventory should Comstock report on its year-end balancesheet?

4. Assume Comstock wasunable to count its ending inventory because it was destroyed in afire. Use the gross profit method to estimate the ending inventory.The gross profit rate is 52%.

| Beginninginventory Endinginventory Netpurchases Net sales | $ 10,000 ? 110,000 175,000 |

Jarrod RobelLv2

15 Jul 2018