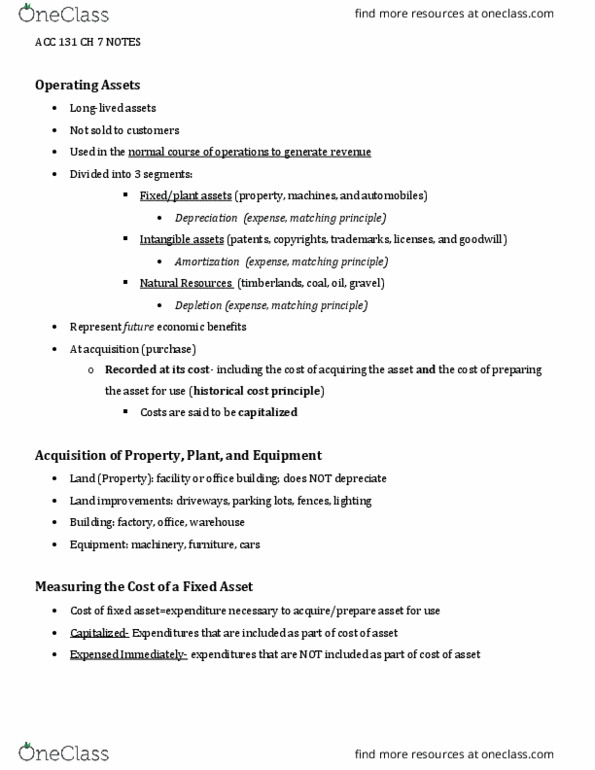

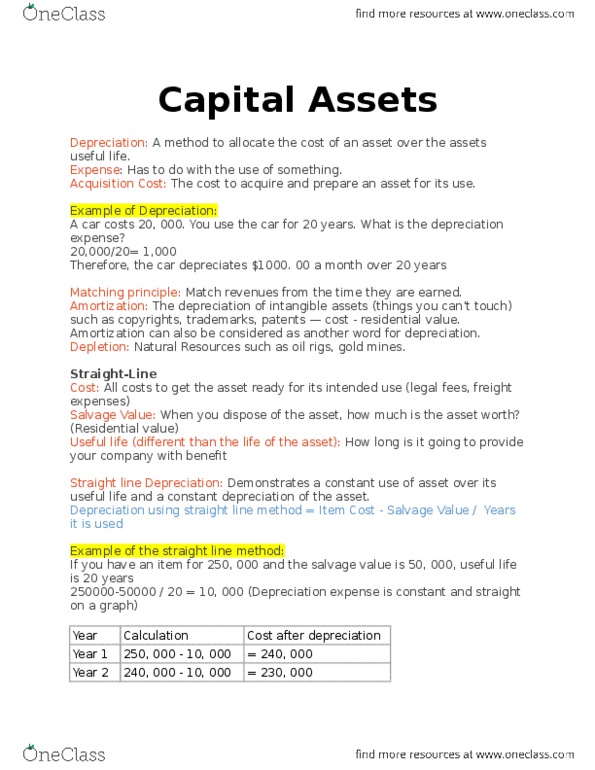

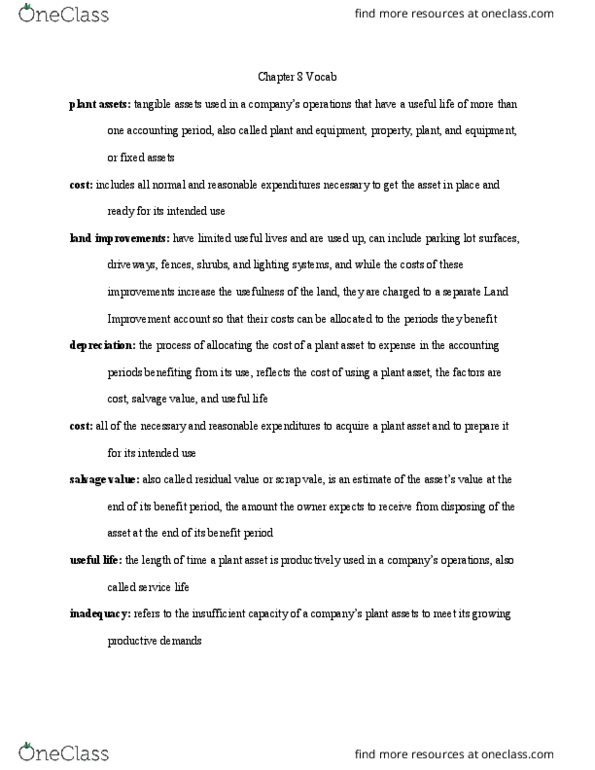

The fact that generally accepted accounting principles allowcompanies flexibility in choosing between certain allocationmethods can make it difficult for a financial analyst to compareperiodic performance from firm to firm.

Suppose you were a financialanalyst trying to compare the performance of two companies. CompanyA uses the double-declining-balance depreciation method. Company Buses the straight-line method. You have the following informationtaken from the 12/31/16 year-end financial statements for CompanyB:

Income Statement Depreciationexpense $ 7,000

Balance Sheet Assets: Plant and equipment, at cost $ 140,000 Less: Accumulated depreciation (28,000 ) Net $ 112,000

You also determine that all of theassets constituting the plant and equipment of Company B wereacquired at the same time, and that all of the $140,000 representsdepreciable assets. Also, all of the depreciable assets have thesame useful life and residual values are zero.

Required:

1. In order to compare performance with Company A, estimate whatB's depreciation expense would have been for 2016 if thedouble-declining-balance depreciation method had been used byCompany B since acquisition of the depreciable assets.

2. If Company B decided to switch depreciation methods in 2016 fromthe straight line to the double-declining-balance method, preparethe 2016 adjusting journal entry to record depreciation for theyear, assuming no journal entry for depreciation in 2016 has beenrecorded. (If no entry is required for a transaction/event,select "No journal entry required" in the first accountfield.)

The fact that generally accepted accounting principles allowcompanies flexibility in choosing between certain allocationmethods can make it difficult for a financial analyst to compareperiodic performance from firm to firm. |

Suppose you were a financialanalyst trying to compare the performance of two companies. CompanyA uses the double-declining-balance depreciation method. Company Buses the straight-line method. You have the following informationtaken from the 12/31/16 year-end financial statements for CompanyB: |

| Income Statement | |||

| Depreciationexpense | $ | 7,000 | |

| Balance Sheet | |||

| Assets: | |||

| Plant and equipment, at cost | $ | 140,000 | |

| Less: Accumulated depreciation | (28,000 | ) | |

| Net | $ | 112,000 | |

You also determine that all of theassets constituting the plant and equipment of Company B wereacquired at the same time, and that all of the $140,000 representsdepreciable assets. Also, all of the depreciable assets have thesame useful life and residual values are zero. |

| Required: |

| 1. | In order to compare performance with Company A, estimate whatB's depreciation expense would have been for 2016 if thedouble-declining-balance depreciation method had been used byCompany B since acquisition of the depreciable assets. |

| 2. | If Company B decided to switch depreciation methods in 2016 fromthe straight line to the double-declining-balance method, preparethe 2016 adjusting journal entry to record depreciation for theyear, assuming no journal entry for depreciation in 2016 has beenrecorded. (If no entry is required for a transaction/event,select "No journal entry required" in the first accountfield.) |