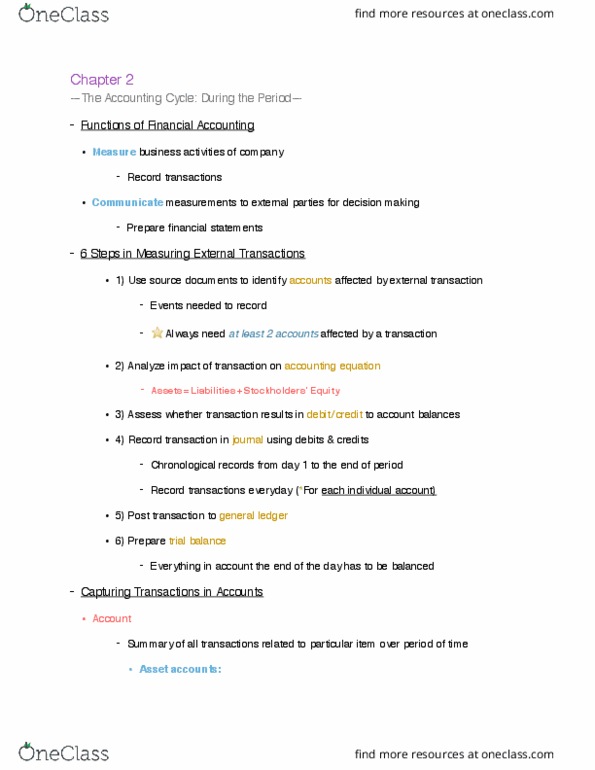

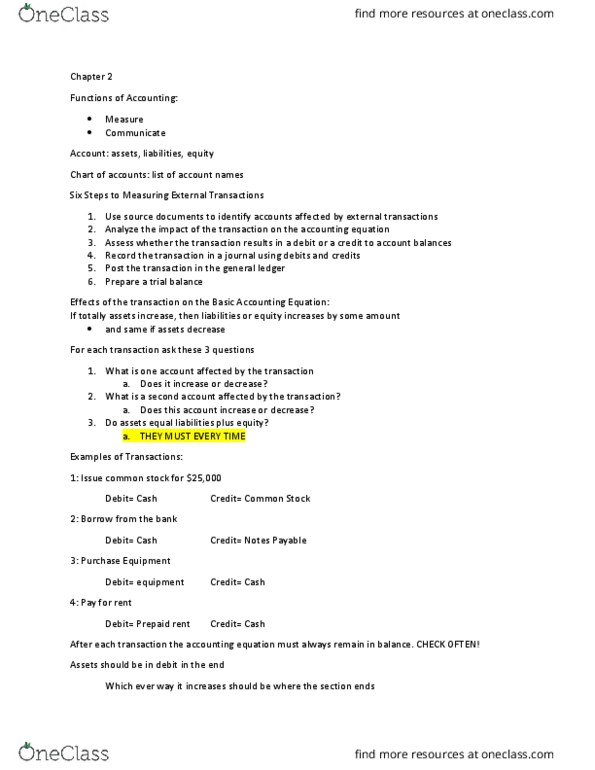

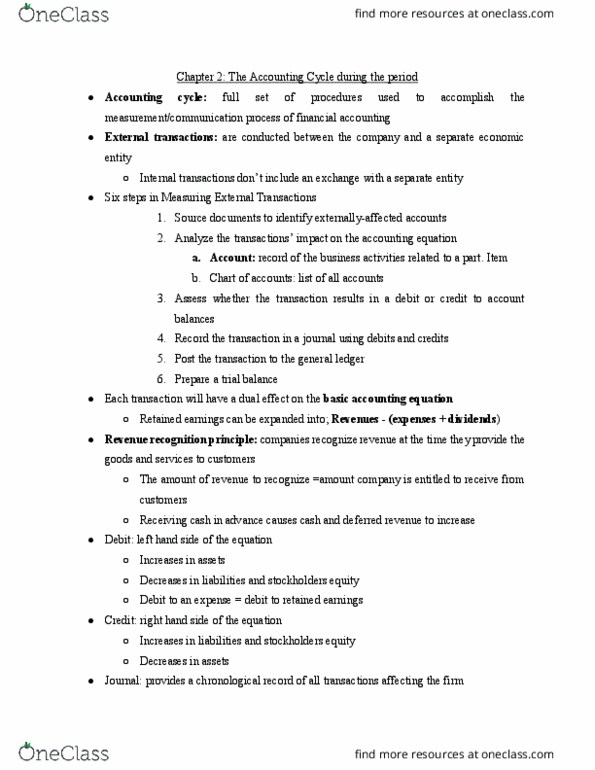

ACC 2010 Lecture Notes - Lecture 2: General Ledger, Trial Balance, Accounting Equation

Get access

Related Documents

Related Questions

PLEASE FOLLOW THE INSTRUCTIONSâ

Assignment: Special Journals: Sales and Cash Receipts (12 Points)

Prepare a cash receipts journal based on the information given below and post it to the Accounts Receivable Subsidiary Ledger.

On Nov 17, Ms. Don & Co. received $1,450 from Gians Graze to apply on account. The source document for this transaction is Receipt 30.

Instructions:

1. Prepare a sales journal entry based on the information given above and post it to the Accounts Receivable General Ledger account and to the Accounts Receivable Subsidiary Ledger. (Use November 7 for this transaction date.) ***This is the same entry that you made for the previous assignment. However, use the transaction date given (Nov. 7).

2. Enter the above transaction (Nov 17) into the Cash Receipts Journal and post it to the Accounts Receivable General Ledger account and to the Accounts Receivable Subsidiary Ledger.

3. Prepare a Schedule of Accounts Receivable and check to see that the total agrees with the Accounts Receivable ledger account.

| Sales Journal | ||||||

| Date | Doc. No. | Customer's Account Name | Post Ref. | Sales Credit | Sales Tax Payable Credit | Accounts Receivable Debit |

| Cash Receipt Journal | ||||||||

| Date | Doc. No. | Account Name | Post Ref. | Sales Credit | Sales Tax Payable Credit | Account Receivable Credit | Sales Discount Credit | Cash in Bank Debit |

| Date | Particulars | Post ref. | Debit | Credit | Balance | |

| Debit | Credit | |||||

| Ms. Don & Co. Schedule of Accounts Receivable November 30, 20xx | ||

| Account Name | Amount | |

| Total Accounts Receivable | $ |

The Polaris Company uses a job-order costing system. Thefollowing transactions occurred in October:

Raw materials purchased on account, $210,000.

Raw materials used in production, $190,000 ($152,000 directmaterials and $38,000 indirect materials).

Accrued direct labor cost of $48,000 and indirect labor cost of$21,000.

Depreciation recorded on factory equipment, $105,000.

Other manufacturing overhead costs accrued during October,$130,000.

The company applies manufacturing overhead cost to productionusing a predetermined rate of $5 per machine-hour. A total of76,100 machine-hours were used in October.

Jobs costing $511,000 according to their job cost sheets werecompleted during October and transferred to Finished Goods.

Jobs that had cost $449,000 to complete according to their jobcost sheets were shipped to customers during the month. These jobswere sold on account at 30% above cost.

Required:

1. Prepare journal entries to record the transactions givenabove.

2. Prepare T-accounts for Manufacturing Overhead and Work inProcess. Post the relevant transactions from above to each account.Compute the ending balance in each account, assuming that Work inProcess has a beginning balance of $34,000.

Raw materials purchased on account, $210,000.

Note: Enter debits before credits.

|

Record the raw materials issued to production, $190,000($152,000 direct materials and $38,000 indirect materials).

Note: Enter debits before credits.

|

Record the entry for accrued direct labor cost incurred,$48,000; indirect labor cost incurred, $21,000.

Note: Enter debits before credits.

Depreciation recorded on factory equipment, $105,000. Note: Enter debits before credits.

Other manufacturing overhead costs accrued during October,$130,000. Note: Enter debits before credits.

|

Record the cost of goods sold.

Note: Enter debits before credits.

|

Record the sales on account.

Note: Enter debits before credits.

|

Prepare T-accounts for Manufacturing Overhead and Work inProcess. Post the relevant transactions from above to each account.Compute the ending balance in each account, assuming that Work inProcess has a beginning balance of $34,000.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

American Laser, Inc., reported the following account balances on January 1. Accounts Receivable $ 5,000 Accumulated Depreciation 30,000 Additional Paid-in Capital 90,000 Allowance for Doubtful Accounts 2,000 Bonds Payable 0 Buildings 247,000 Cash 10,000 Common Stock, 10,000 shares of $1 par 10,000 Notes Payable (long-term) 10,000 Retained Earnings 120,000 Treasury Stock 0 The company entered into the following transactions during the year. Jan. 15 Issued 5,000 shares of $1 par common stock for $50,000 cash. Feb. 15 Reacquired 3,000 shares of $1 par common stock into treasury for $33,000 cash. Mar. 15 Reissued 2,000 shares of treasury stock for $24,000 cash. Aug. 15 Reissued 600 shares of treasury stock for $4,600 cash. Sept. 15 Declared (but did not yet pay) a $1 cash dividend on each outstanding share of common stock. Oct. 1 Issued 100, 10-year, $1,000 bonds, at a quoted bond price of 101. Oct. 3 Wrote off a $500 balance due from a customer who went bankrupt.

Prepare the journal entries to record each transaction. Review the accounts as shown in the General Ledger and Trial Balance tabs. If no entry is required for a transaction/event, select "No journal entry required" in the first account field.

1

Issued 5,000 shares of $1 par common stock for $50,000 cash. Record the transaction.

2

Reacquired 3,000 shares of $1 par common stock into treasury for $33,000 cash. Record the transaction.

3

Reissued 2,000 shares of treasury stock for $24,000 cash. Record the transaction.

4

Reissued 600 shares of treasury stock for $4,600 cash. Record the transaction.

5

Declared (but did not yet pay) a $1 cash dividend on each outstanding share of common stock. Record the transaction.

6

Issued 100, 10-year, $1,000 bonds, at a quoted bond price of 101. Record the transaction.

7

Wrote off a $500 balance due from a customer who went bankrupt. Record the transaction.

8

Prepare the closing entry for Dividends. Record the transaction.

Each journal entry is posted automatically to the general ledger. Use the drop-down button to view the unadjusted, adjusted, or post-closing balances.

UnadjustedPost-closing Unadjusted

Unadjusted

Post-closing

Dates:Jan 01

Jan 01

Jan 31

Jan 01

Jan 31

Jan 15

Jan 31

Feb 15

Feb 28

Mar 15

Mar 31

Aug 15

Aug 31

Sep 15

Sep 30

Oct 01

Oct 03

Oct 31

to:Oct 03

Jan 01

Jan 31

Jan 01

Jan 31

Jan 15

Jan 31

Feb 15

Feb 28

Mar 15

Mar 31

Aug 15

Aug 31

Sep 15

Sep 30

Oct 01

Oct 03

Oct 31

| General Ledger Account | ||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

| |||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||