MGT 200 Lecture Notes - Lecture 2: Weighted Arithmetic Mean, Standard Deviation

Document Summary

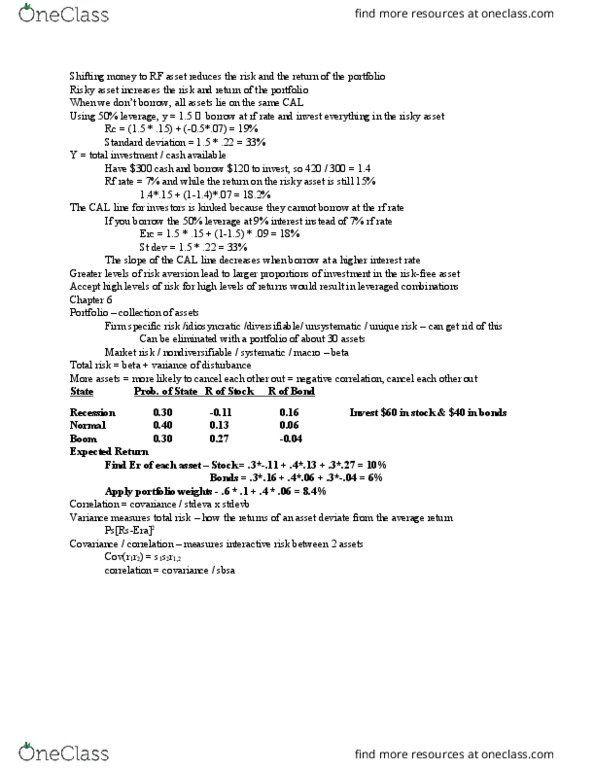

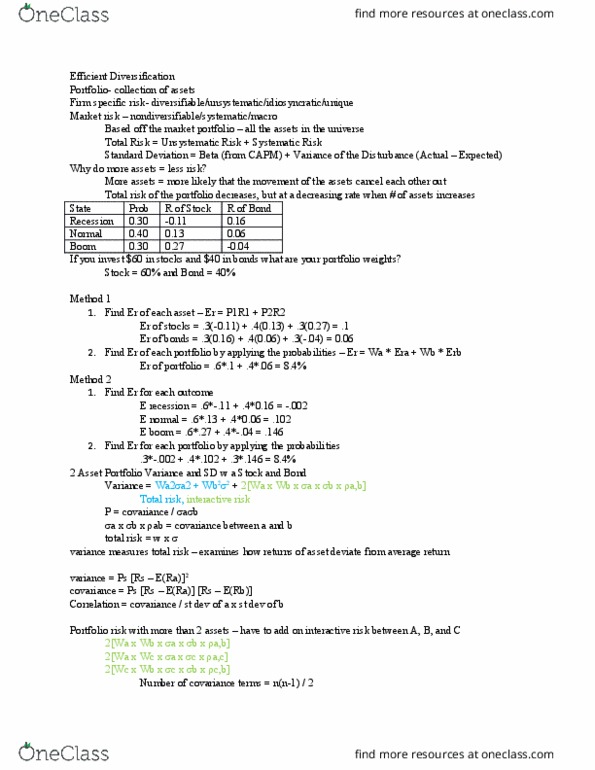

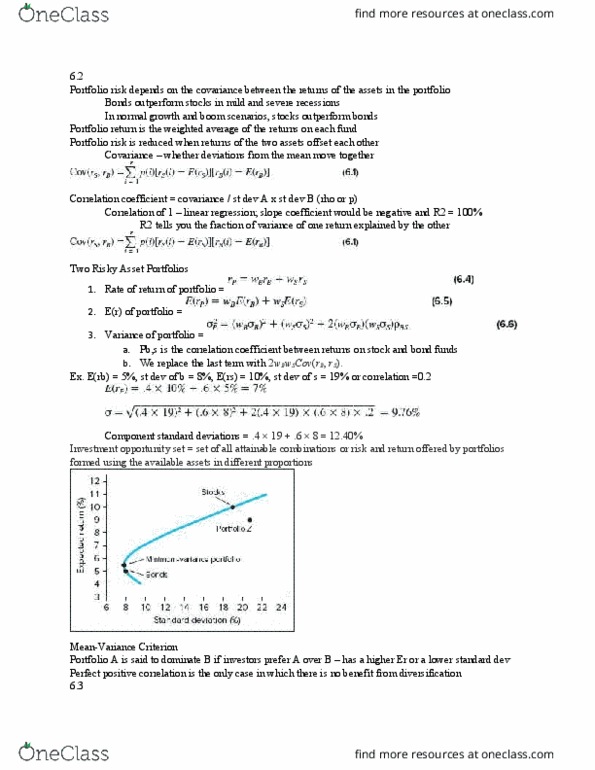

Market/systematic/nondiversifiable risk- risk that remains even after diversification. Diversifiable/nonsystematic/firm-specific/unique risk = risk that can be eliminated after diversification. Portfolio risk depends on covariance- does best when assets offset each other. Probability weighted average- average tendency of assets to vary in tandem. Negative -when one performs well, the other performs poorly. Suppose we invest 85% in bonds and only 15% in stocks. We can construct a portfolio with an expected return higher than bonds (. 85 5) + (. 15 10) = 5. 75% and, at the same time, a standard deviation less than bonds. Using equation 6. 6 again, we find that the portfolio variance is. And, accordingly, the portfolio standard deviation is deviation of either bonds or stocks alone. Taking on a more volatile asset (stocks) actually reduces portfolio risk! Investment opportunity set- set of all attainable combos of risk and return offered by assets in differing proportions.