ACCT 305 Lecture Notes - Lecture 22: Financial Statement, Retained Earnings, Accrued Interest

Document Summary

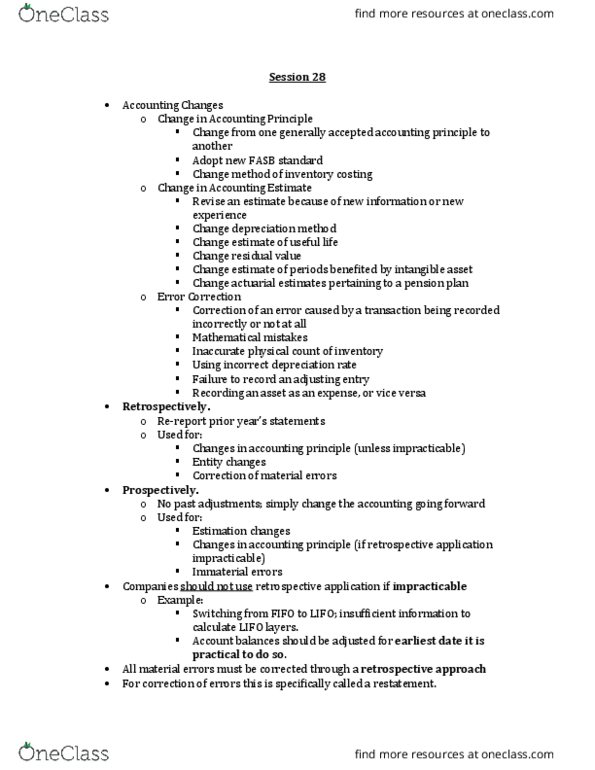

Accounting alternatives: diminish the comparability of financial information, obscure useful historical trend data. Types of accounting changes: change in accounting policy, changes in accounting estimate, change in reporting entity. Changes in accounting principle: change from one accepted accounting policy to another, examples include, average cost to lifo, completed-contract to percentage-of-completion. *adoption of a new principle in recognition of events that have occurred for the first time or that were previously immaterial is not an accounting change: three approaches for reporting changes, currently, retrospectively, prospectively (in the future) *if any of the above conditions exists, the company prospectively applies the new accounting principle. Retained earnings balance is ,360,000 at the beginning of 2012. Examples of estimates: uncollectible receivables, inventory obsolescence, useful lives and salvage values of assets, periods benefitted by deferred costs, liabilities for warranty costs and income taxes, recoverable mineral reserves, change in depreciation methods.