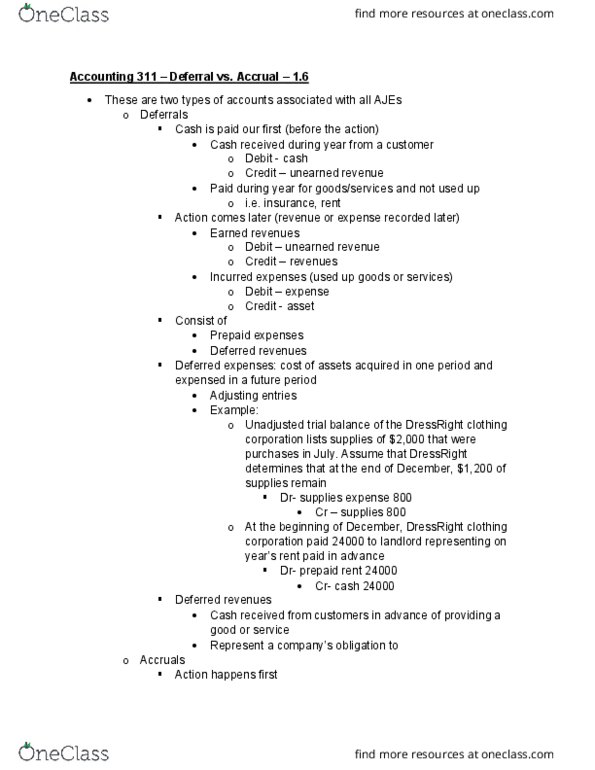

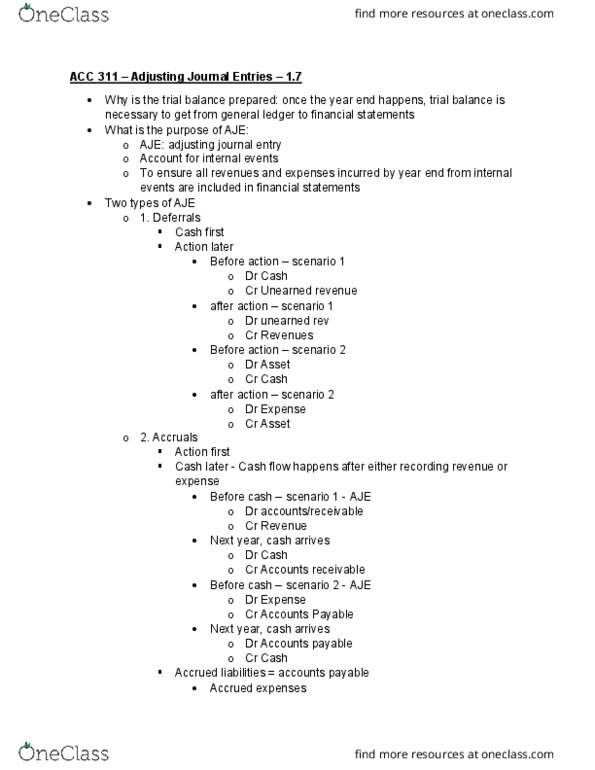

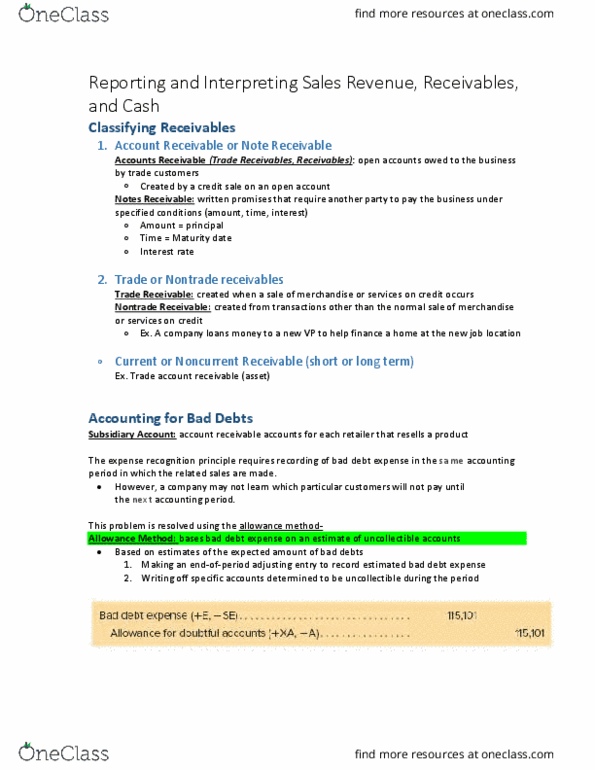

ACC 311 Lecture Notes - Lecture 5: Deferral, Accrual

Get access

Related Documents

Related Questions

The following adjustments need to be made before the financialstatements can be prepared at the end of the year.

Task 1: Enter the necessary journal entries into the templateprovided and provide the journal entry for each.

December Interest on a bank loan is due on January 2nd of thefollowing year: accrue $1,000.

A contractor (outside services) has finished work on December 31st,but the invoice will not be received until January 7th of thefollowing year: accrue $750. A rent payment was made on December1st for three months from December 1st to February 28th of thefollowing year (6,000 in total). Record the transactionproperly.

The companyâs part-time employees worked a total of 50 hours inDecember, but will get paid only by January 5th. The hourly rate is$15.

The company must record the payment of its annual insurance premiumfor next year. The annual premium is $1,200, an adjustment isnecessary to prepaid insurance.

Task 2: Provide the adjusted trial balance (combine exercises2.1 and 2.2 to show the adjusted trial balance).

| 1 | Interest Expense | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Interest Payable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record December interest expense to bepaid in January | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2 | Expense for Outside Services | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accounts Payable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record liability towardscontractor | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3 | Rental Expenses | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Prepaid Rent | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record the appropiate rental expensefor the month | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4 | Wage Expense | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wages Payable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record liability towards employees | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5 | Prepaid Insurance | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record insurance payment for thefollowing year | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $0 | $0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

NEED ANSWERS ASAP

Question 23

If a resource has been consumed but a bill hasnot been received at the end of the accountingperiod, then

an expense should be recorded when the bill is received. | ||

an expense should be recorded when the cash is paid out. | ||

an adjusting entry should be made recognizing the expense. | ||

it is optional whether to record the expense before the bill isreceived. |

3 points

Question 24

Prepaid expenses are

paid and recorded in an asset account before they are used orconsumed. | ||

paid and recorded in an asset account after they are used orconsumed. | ||

incurred but not yet paid or recorded. | ||

incurred and already paid or recorded. |

3 points

Question 25

If a business has received cash in advance of services performedand credits a liability account, the adjusting entry needed afterthe services are performed will be

debit Unearned Service Revenue and credit Cash. | ||

debit Unearned Service Revenue and credit Service Revenue. | ||

debit Unearned Service Revenue and credit Prepaid Expense. | ||

debit Unearned Service Revenue and credit AccountsReceivable. |

3 points

Question 26

The preparation of adjusting entries is

straight forward because the accounts that need adjustment willbe out of balance. | ||

often an involved process requiring the skills of aprofessional. | ||

only required for accounts that do not have a normalbalance. | ||

optional when financial statements are prepared. |

3 points

Question 27

On January 1 of the current year, Doolittle Company purchasedfurniture for $7,560. The company expects to use the furniture for3 years. The asset has no salvage value. The book value of thefurniture at December 31of this year is

$0. | ||

$2,520. | ||

$5,040. | ||

$7,560. |

3 points

Question 28

Husker Du Supplies Inc. purchased a 12-month insurance policy onMarch 1 of the current year for $1,800. At March 31, the adjustingjournal entry to record expiration of this asset will include a

debit to Prepaid Insurance and a credit to Cash for $1,800. | ||

debit to Prepaid Insurance and a credit to Insurance Expense for$200. | ||

debit to Insurance Expense and a credit to Prepaid Insurance for$150. | ||

debit to Insurance Expense and a credit to Cash for $150. |

#16 Adjusting Entries

Journalize the adjusting entry needed on December 31, end of thecurrent period for each of the independent cases. Assume for allthe different situations that prior adjusting entries were NOTcompleted.

On June 1, Brown Company received $24,000 cash for a one yearsubscription to its monthly magazine. The term of the subscriptionbegins on June 1. The company uses an account called unearnedsubscription Revenue. Make the appropriate adjusting entry onDecember 31.

Date | Account Name | Acct. Type | Debit | Credit |

| ||||

|

Clark Company pays its employees every Friday for a five-daywork week. The amount of weekly Payroll is $100,000. December 31 ofthe current year is a Thursday. Make the appropriate adjustingentry on December 31.

Date | Account Name | Acct. Type | Debit | Credit |

| ||||

|

On September 1 of the current year, Williams Company rented toanother company some excess space in one of its buildings. WilliamsCompany received $30,000 cash on September 1. The rental periodextends for eight months, starting on September 1.Williams Company credited the Unearned Rent revenue account uponreceipt of the rent paid in advance. Make the appropriate adjustingentry on December 31.

Date | Account Name | Acct. Type | Debit | Credit |

| ||||

|

At the beginning of the year, the company had $1000 in supplieson hand. During the year the company purchased $5,300 in supplies.At the end of the year, the company had $2,000 of supplies stillavailable. Make the appropriate adjusting entry on December 31.

Date | Account Name | Acct. Type | Debit | Credit |

| ||||

|

Interest was incurred for a loan (Note Payable) in the amount of$3,000. Make the appropriate adjusting entry on December 31.

Date | Account Name | Acct. Type | Debit | Credit |

| ||||

|

Interest was earned on a Note receivable in the amount of$2,000. Make the appropriate adjusting entry on December 31.

Date | Account Name | Acct. Type | Debit | Credit |

| ||||

|