ECON 101 Lecture Notes - Lecture 10: Economic Equilibrium, Flat Tax, Economic Surplus

30

ECON 101 Full Course Notes

Verified Note

30 documents

Document Summary

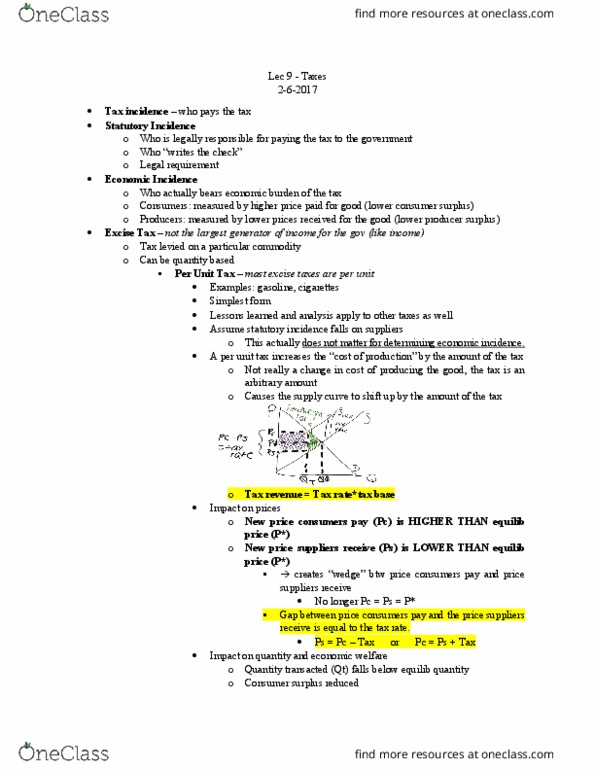

Market forces operate so that price and quantity move towards the equilibrium. The market does many things: pricing, quantity, allocation and production, efficient rationing, incentives. Specific (quantity) tax tax per unit: price demanders pay: pd, price suppliers receive: ps, before tax: p = pd = ps, after tax: pd = ps + t (tax) Tax incidence how the burden of a tax is distributed between buyers and sellers. A tax causes the price consumers pay to increase and at the same time the price producers get to decrease drives a wedge between pd and ps. Supply curve shifts up by the amount of the tax. Price suppliers keep = price paid tax: p" = old equilibrium price, incidence on buyers = pd p", incidence on sellers = p" ps. Tax something, and the equilibrium quantity becomes lower. Sin tax discourages consumption and boosts government revenue. Deadweight loss the cost of the economic inefficiency caused by the tax.