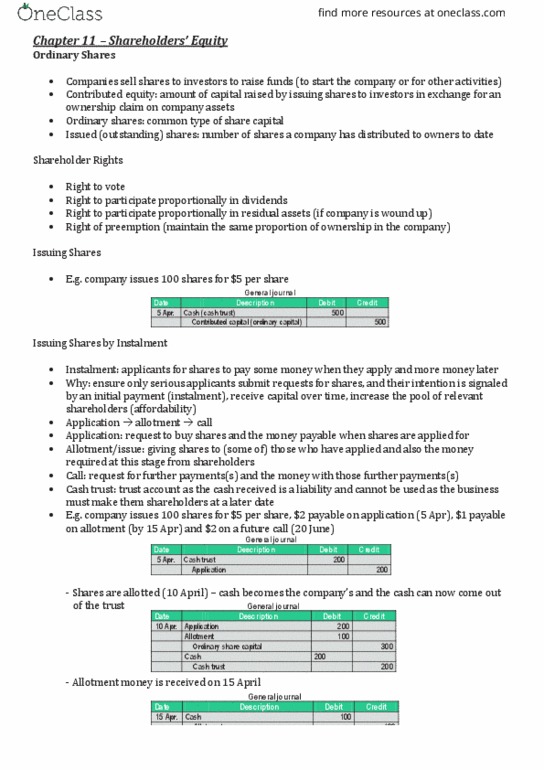

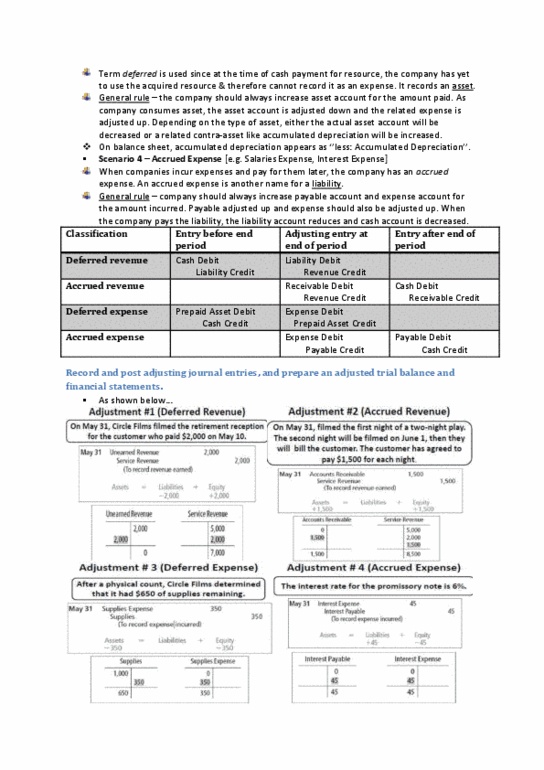

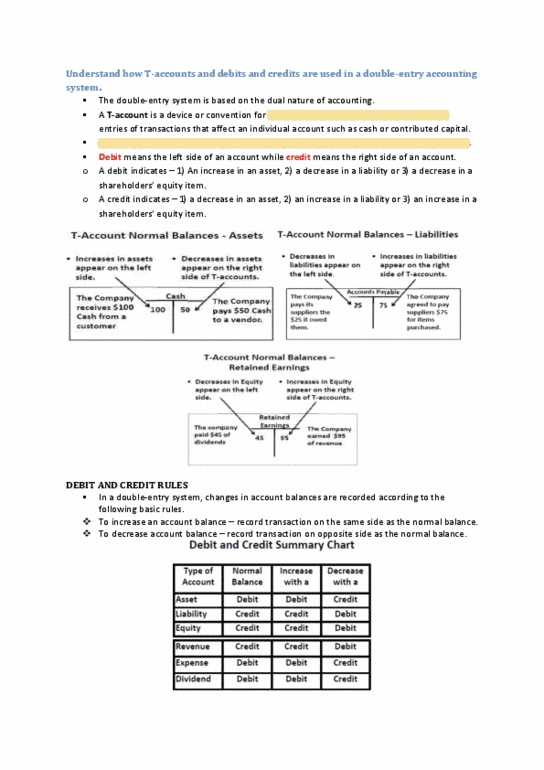

BA 3340 Lecture Notes - Lecture 23: Current Liability, Book Value, Cash Flow

Document Summary

Liquidation: closing down of a business that involves partners taking any remaining assets. Nca are sold, liabilities are paid and the partners receive their share of any cash remaining reduce the balance in all accounts to zero. Nca are sold for their carrying amount at 300. This is shared between a at 10%, b at. Nca are sold for 500 which is above the carrying amount. The profit is shared between a at 10%, b at 20% and c at 70%. Nca are sold for which is less than the carrying amount. The loss is shared between a at 10%, b at 20% and c at 70%. Gain on sale of nca is 000 and is shared between a, b and c in the ratio of 4:3:3. loss to share between a, b and c in the ratio of 4:3:3. Gain on sale (dr gain on sale / cr capital of partners.