BA 3301 Lecture Notes - Lecture 48: Myer, Ordinary Income, Capital Asset

Document Summary

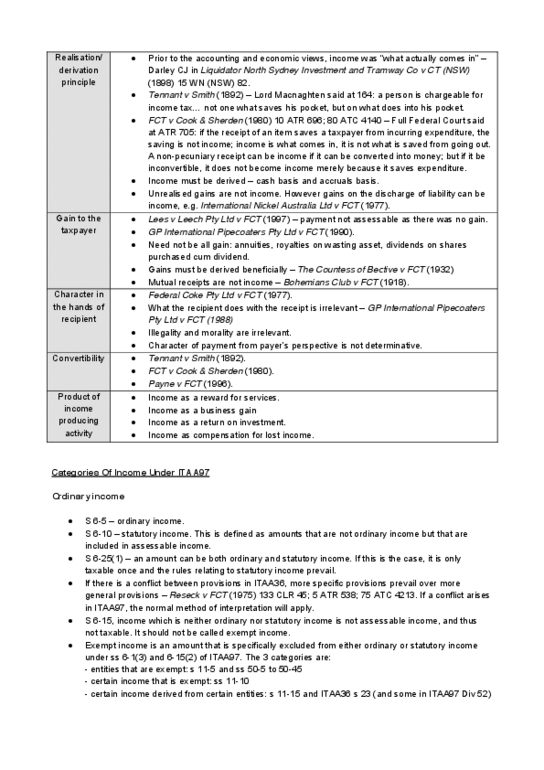

Taxpayer"s business. (cid:120) federal coke co pty ltd v fct (1977) 7 atr 519; 77 atc 4255 bowen cj at. A payment is likely to be a substitute for lost income when the inconvenience is incident to that type of business. Correspondence (cid:120) there is no symmetry between itaa97 s 6-5 (ordinary income) and itaa97 s 8- principle. In fct v rowe, the high court held that an amount paid as compensation or reimbursement of a deductible expense is not income by ordinary concepts. Owen j at aitr 7: the company"s business was that of a saw-miller. It was in that capacity that it paid royalties for the timber cut by it for the purposes of the business and it was in that capacity that it received the amounts refunded. Itaa36 s 6(1) income from property refers to income other than income from personal exertion.