ACCT 2101 Lecture Notes - Lecture 2: Deferral, Financial Statement Analysis, Accounts Payable

14 Sep 2016

School

Department

Course

Professor

Document Summary

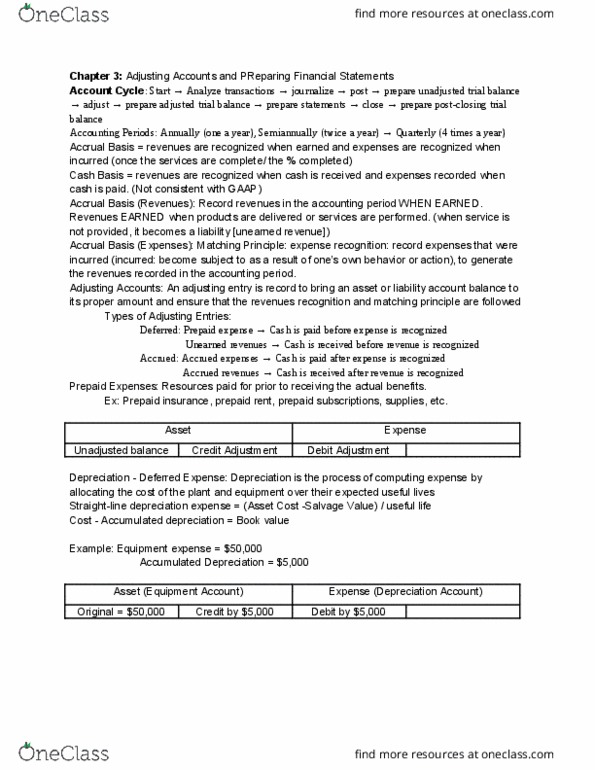

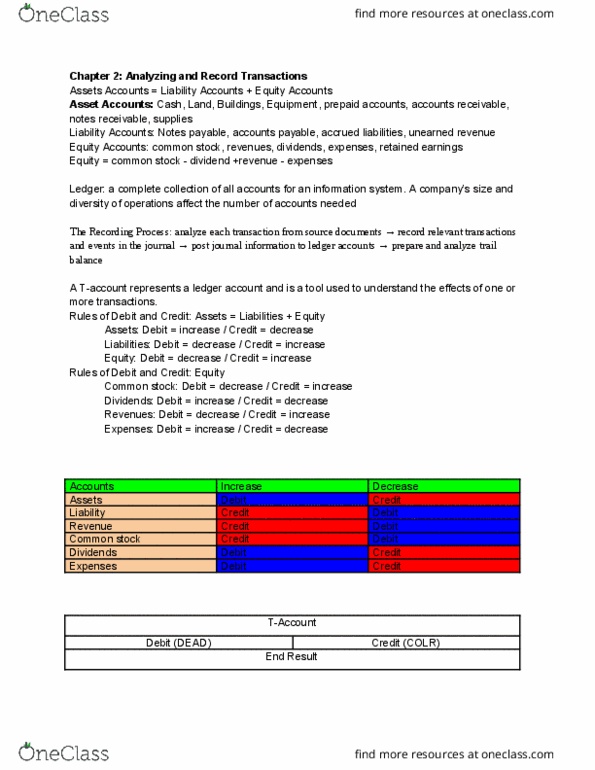

An account is a record of increases and decreases in a specific asset, liability, equity, revenue, or expense. Prepaid expenses: expense paid in advance of receiving a benefit from it; asset that represents prepayments of future benefits. Accrued liabilities: all items owed but not paid. Financial statement analysis focuses on one or more of 4 basic building blocks of analysis. Liquidity: the availability of resources to meet short-term obligations and generate revenues. Current ratio = current assets / current liabilities. Solvency: refers to a company"s long-run financial viability and its ability to generate future revenues. Debt ratio = total liabilities / total assets. Profitability: refers to a company"s ability to use its assets to produce profits (and positive cash flows) Profit margin = net income / net sales. Market prospects = the ability to generate positive market expecta- tions. Price-to-earnings = price per share / earnings per share. Ledger: complete collection of all accounts for an info system.