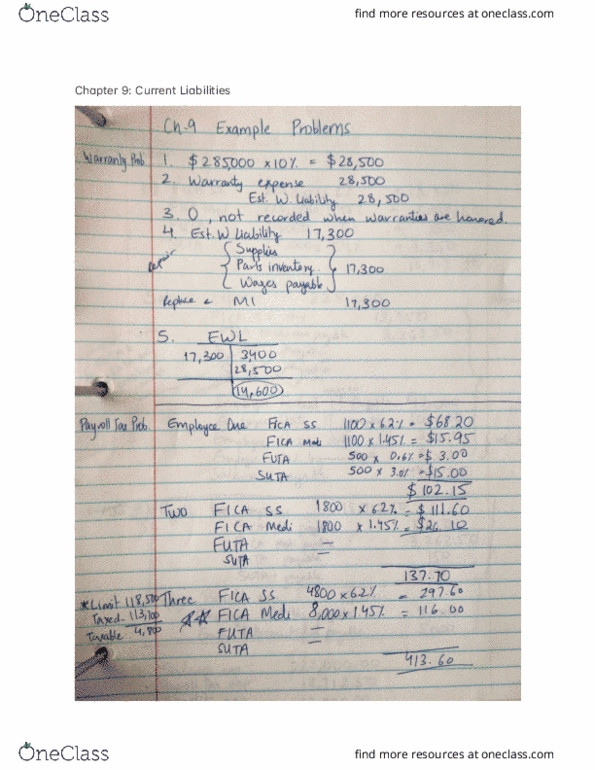

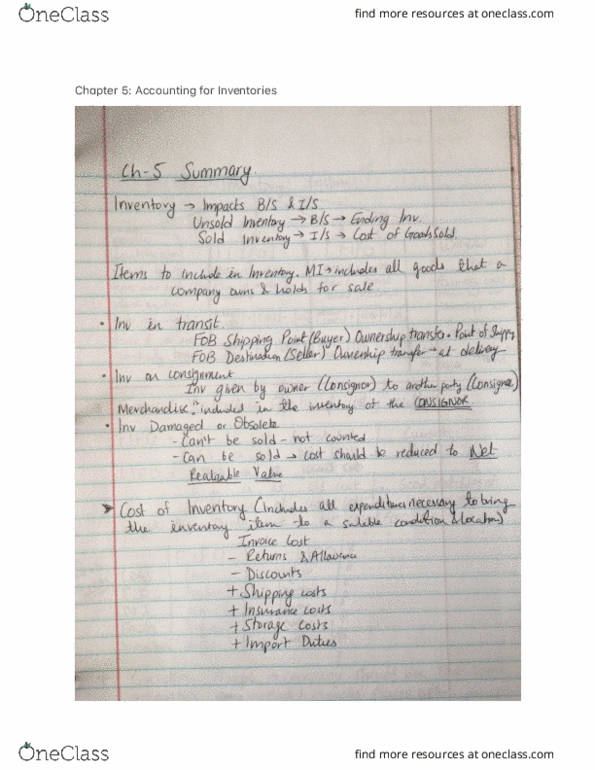

ACCT 2101 Lecture 12: Chapter 12: Statement of Cashflows

This preview shows page 1 of the document.

Unlock all 3 pages and 3 million more documents.

Get access

Related Documents

Related Questions

Receiving Report Number | Amount on Vendorâs Invoice | Amount Presently Included in or Excluded from AccountsPayable | RECEIPT and VENDORâS INVOICE DATA | ||

Received Date | Invoice and Shipping Date | FOB Origin or Destination | |||

101 | $2,619.26 | Included | 12-30-04 | 12-30-04 | Origin |

102 | 3,709.16 | Included | 12-26-04 | 12-15-04 | Destination |

103 | 5,182.31 | Included | 12-31-04 | 12-26-04 | Origin |

104 | 6,403.00 | Included | 12-16-04 | 12-27-04 | Destination |

105 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

106 | 5,916.20 | Included | 01-03-05 | 12-31-04 | Destination |

107 | 7,515.50 | Included | 01-05-05 | 12-26-04 | Origin |

108 | 3,709.16 | Included | 12-26-04 | 12-15-04 | Destination |

109 | 5,182.31 | Included | 12-31-04 | 12-26-04 | Origin |

110 | 6,403.00 | Excluded | 12-16-04 | 12-27-04 | Destination |

111 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

112 | 5,916.20 | Excluded | 01-03-05 | 12-31-04 | Destination |

113 | 7,515.50 | Included | 01-05-05 | 12-26-04 | Origin |

114 | 6,403.00 | Included | 12-16-04 | 12-27-04 | Destination |

115 | 3,709.16 | Included | 12-26-04 | 12-15-04 | Destination |

116 | 5,182.31 | Included | 12-31-04 | 12-26-04 | Origin |

117 | 6,403.00 | Included | 12-16-04 | 12-27-04 | Destination |

118 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

119 | 5,916.20 | Excluded | 01-03-05 | 12-31-04 | Destination |

121 | 7,515.50 | Included | 01-05-05 | 12-26-04 | Origin |

122 | 3,709.16 | Included | 12-26-04 | 12-15-04 | Destination |

124 | 5,182.31 | Included | 12-31-04 | 12-26-04 | Origin |

125 | 6,403.00 | Excluded | 12-16-04 | 12-27-04 | Destination |

126 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

127 | 5,916.20 | Excluded | 01-03-05 | 12-31-04 | Destination |

128 | 7,515.50 | Excluded | 01-05-05 | 12-26-04 | Origin |

129 | 6,403.00 | Excluded | 12-16-04 | 12-27-04 | Destination |

130 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

Given the data on above Table, in your opinion, is a moredetailed look at all of the transactions necessary? Why? Pleaseassume that the acceptable amount of misstatement is 5% of thetotal amount of the vendor invoices shown.

Receiving Report Number | Amount on Vendorâs Invoice | Amount Presently Included in or Excluded from AccountsPayable | RECEIPT and VENDORâS INVOICE DATA | ||

Received Date | Invoice and Shipping Date | FOB Origin or Destination | |||

101 | $2,619.26 | Included | 12-30-04 | 12-30-04 | Origin |

102 | 3,709.16 | Included | 12-26-04 | 12-15-04 | Destination |

103 | 5,182.31 | Included | 12-31-04 | 12-26-04 | Origin |

104 | 6,403.00 | Included | 12-16-04 | 12-27-04 | Destination |

105 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

106 | 5,916.20 | Included | 01-03-05 | 12-31-04 | Destination |

107 | 7,515.50 | Included | 01-05-05 | 12-26-04 | Origin |

108 | 3,709.16 | Included | 12-26-04 | 12-15-04 | Destination |

109 | 5,182.31 | Included | 12-31-04 | 12-26-04 | Origin |

110 | 6,403.00 | Excluded | 12-16-04 | 12-27-04 | Destination |

111 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

112 | 5,916.20 | Excluded | 01-03-05 | 12-31-04 | Destination |

113 | 7,515.50 | Included | 01-05-05 | 12-26-04 | Origin |

114 | 6,403.00 | Included | 12-16-04 | 12-27-04 | Destination |

115 | 3,709.16 | Included | 12-26-04 | 12-15-04 | Destination |

116 | 5,182.31 | Included | 12-31-04 | 12-26-04 | Origin |

117 | 6,403.00 | Included | 12-16-04 | 12-27-04 | Destination |

118 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

119 | 5,916.20 | Excluded | 01-03-05 | 12-31-04 | Destination |

121 | 7,515.50 | Included | 01-05-05 | 12-26-04 | Origin |

122 | 3,709.16 | Included | 12-26-04 | 12-15-04 | Destination |

124 | 5,182.31 | Included | 12-31-04 | 12-26-04 | Origin |

125 | 6,403.00 | Excluded | 12-16-04 | 12-27-04 | Destination |

126 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

127 | 5,916.20 | Excluded | 01-03-05 | 12-31-04 | Destination |

128 | 7,515.50 | Excluded | 01-05-05 | 12-26-04 | Origin |

129 | 6,403.00 | Excluded | 12-16-04 | 12-27-04 | Destination |

130 | 8,484.91 | Included | 12-28-04 | 12-31-04 | Origin |

Using the following Purchase Order Receipts (Table 1 above), howmight you approach using audit sampling to determine if theaccounting data in the table has a material amount of errors ormisstatements as of December 31, 2004?

P8-4A The bankportion of the bank reconciliation for Backhaus Company at November30, 2010, was as follows.

BACKHAUS COMPANY

Bank Reconciliation

November 30, 2011

Cash balance perbank $14,367.90

Add: Deposits intransit 2,530.20

16,898.10

Less: Outstanding checks

CheckNumber Check Amount

3451 $2,260.40

3470 720.10

3471 844.50

3472 1,426.80

3474 1,050.00 6,301.80

Adjusted cash balance perbank $10,596.30

The adjusted cash balance per bankagreed with the cash balance per books at November 30.

The December bank statement showedthe following checks and deposits.

Bank Statement | |||||

Checks | Deposits | ||||

Date | Number | Amount | Date | Amount | |

12-1 | 3451 | $2,260.40 | 12-1 | $2,530.20 | |

12-2 | 3471 | 844.50 | 12-4 | 1,211.60 | |

12-7 | 3472 | 1,426.80 | 12-8 | 2,365.10 | |

12-4 | 3475 | 1,640.70 | 12-16 | 2,672.70 | |

12-8 | 3476 | 1,300.00 | 12-21 | 2,945.00 | |

12-10 | 3477 | 2,130.00 | 12-26 | 2,567.30 | |

12-15 | 3479 | 3,080.00 | 12-29 | 2,836.00 | |

12-27 | 3480 | 600.00 | 12-30 | 1,025.00 | |

12-30 | 3482 | 475.50 | Total | $18,152.90 | |

12-29 | 3483 | 1,140.00 | |||

12-31 | 3485 | 540.80 | |||

Total | $15,438.70 | ||||

The cash records per books forDecember showed the following.

Cash Payments Journal | Cash Receipts Journal | |||||||

Date | Number | Amount | Date | Number | Amount | Date | Amount | |

12-1 | 3475 | $1,640.70 | 12-20 | 3482 | $475.50 | 12-3 | $1,211.60 | |

12-2 | 3476 | 1,300.00 | 12-22 | 3483 | 1,140.00 | 12-7 | 2,365.10 | |

12-2 | 3477 | 2,130. 00 | 12-23 | 3484 | 798.00 | 12-15 | 2,672.70 | |

12-4 | 3478 | 621.30 | 12-24 | 3485 | 450.80 | 12-20 | 2,954.00 | |

12-8 | 3479 | 3080.00 | 12-30 | 3486 | 1,889.50 | 12-25 | 2,567.30 | |

12-10 | 3480 | 600.00 | Total | $14,933.20 | 12-28 | 2,836.00 | ||

12-17 | 3481 | 807.40 | 12-30 | 1,025.00 | ||||

12-31 | 1,690.40 | |||||||

Total | $17,322.10 | |||||||

The bank statement contained twomemoranda:

A credit of $4,145 for the collection of a $4,000 note forBackhaus Company plus interest of $160 and less a collection fee of$15. Backhaus Company has not accrued any interest on the note.

A debit of $572.80 for an NSF check written by D. Chagnon, acustomer. At December 31, the check had not been redeposited in thebank.

At December 31, the cash balance perbooks was $12,985.20, and the cash balanced per the bank statementwas $20,654.30. The bank did not make errors, but two errors weremade by Backhaus Company.

Instructions

Prepare a bank reconciliation at December 31.

Prepare the adjusting entries based on the reconciliation.(Hint: The correction of any errors pertaining to recording checksshould be made to Accounts Payable. The correction of any errors torecording cash receipts should be made to Accounts Receivable.)