ACG 2071 Lecture Notes - Lecture 4: Direct Labor Cost, Cost Driver, Financial Statement

9 Sep 2018

School

Department

Course

Professor

Document Summary

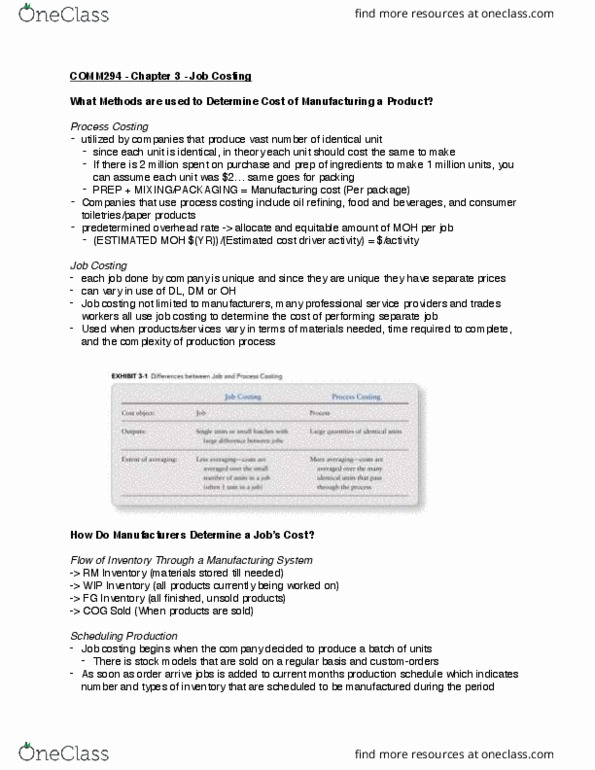

Companies that use job costing: produce unique products or small batches ( jobs , result accumulate costs separately for each job, examples hospitals, consulting firms, home builder. Manufacturing overhead (moh: costs related to production operations as a whole, not feasible to trace to specific jobs, result allocate portion to all jobs using predetermined rate. Moh allocated to a job = predetermined overhead rate(pohr) x actual amount of allocation base used by the job. Pohr = [estimated total annual moh costs / estimated total annual units of allocation base (operating activity)] Steps in calculating pohr: estimate total annual moh costs, select an allocation base, estimate total units of allocation base for year, divide estimated total costs (step 1) by estimated total units of allocation base (step 3) Potential allocation bases: primary factor that causes moh costs to vary ( cost driver , examples direct labor hours, direct labor cost, machine hours, units produced (if just 1 product)