ACCT 2001 Lecture Notes - Lecture 5: Profit Margin, Trial Balance, Retained Earnings

67

ACCT 2001 Full Course Notes

Verified Note

67 documents

Document Summary

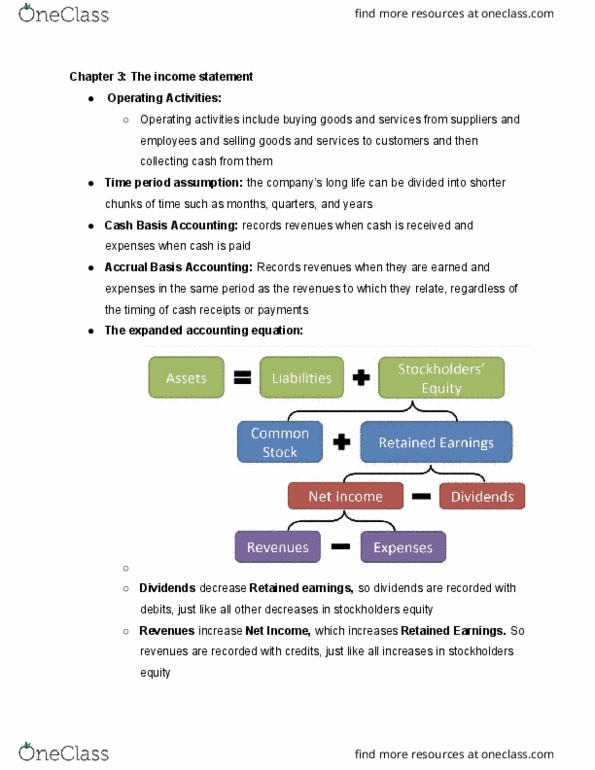

The income statement: occur regularly and often have a shorter duration of effect, includes buying goods and services from suppliers and employees and selling goods and services to customers and collecting cash from them, operating cycle. Calculated by subtracting expenses from revenues: time period assumption. Balance sheet accounts are considered permanent, whereas income statement accounts are considered temporary. The balance sheet takes stock of what exists at a point in time whereas the income statement depicts a flow of what happened over a period of time: study the accounting methods, cash basis accounting. Reports revenues when cash is received and expenses when cash is paid; not allowed under gaap: doesn"t measure financial performance very well when transaction are conducted using credit rather than cash, accrual basis accounting. Reports revenues when they are earned and expenses when they are incurred, regardless of the timing of cash receipt or payment; required under gaap.