MGMT 1A Lecture Notes - Lecture 4: General Ledger, Deferral, Retained Earnings

Document Summary

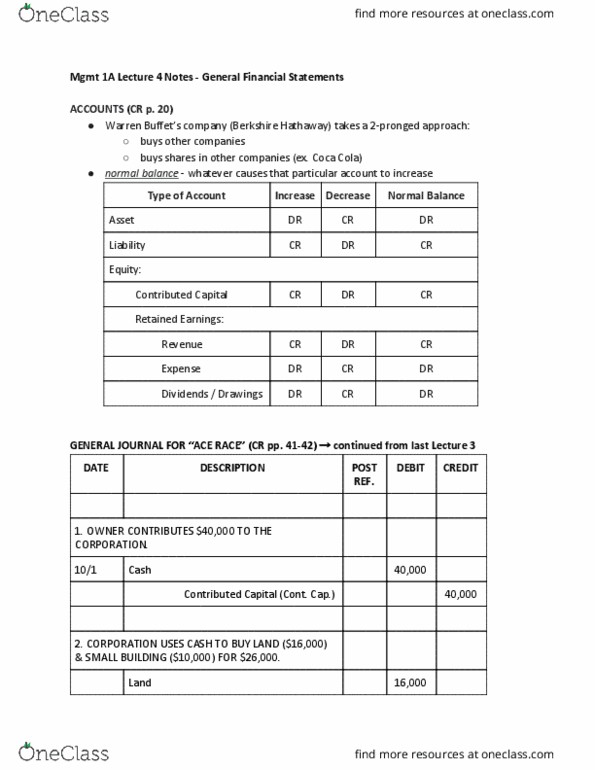

Contra accounts: they are always attached to another account, ex. accumulated depreciation is always attached to . Equipment or (pp&e: they have the opposite balance of the normal account balance, contra-assets have cr. balances, contra- liabilities have dr. balances, they reduce the account to which they are attached to, accumulated depreciation reduces equipment. Ex. credits increase retained earnings, credit is the normal balance of retained earnings. Investments or marketable securities (stocks and bonds: cash & cash equivalents. 2: accounts receivable - amount owed to a company, merchandise inventory, prepaid expenses - services and goods purchased in advance of use, supplies. Creating financial statements from the general ledger (t-accounts) Each statement needs 3 things: name of the company, name of the statement, date. This means that transactions are only recorded when cash actually changes hand, it is not recorded if cash is not yet paid.