ECON 132A Lecture Notes - Lecture 7: Capital Asset Pricing Model, Efficient-Market Hypothesis, Expected Return

26 Apr 2016

School

Department

Course

Professor

Document Summary

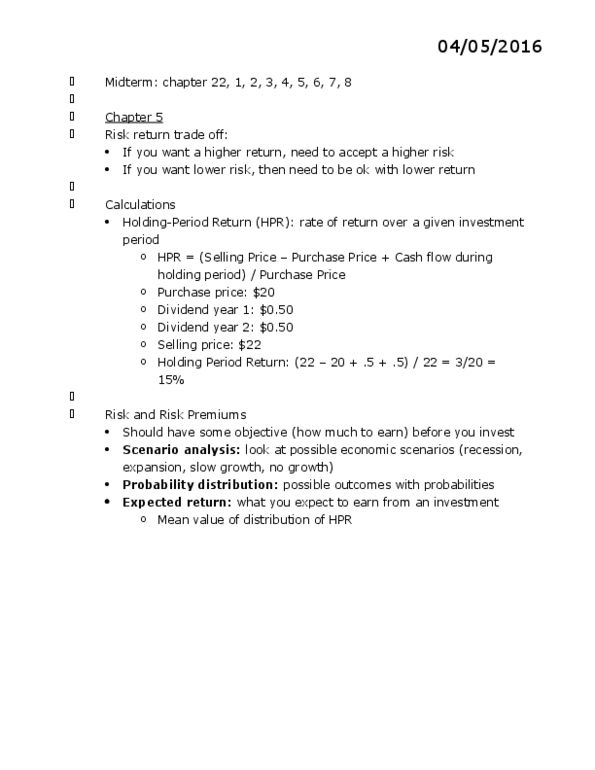

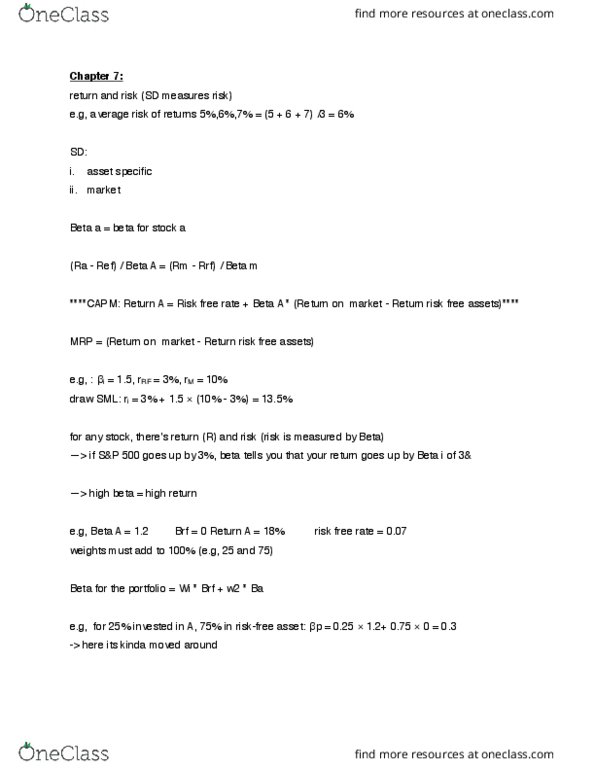

Midterm: chapter 22 (light), 1 (medium), 2 (medium), 3 (medium), 4 (heavy), 5 (heavy), 6 (medium), 7 (medium), 8 (heavy) Expected return = risk free rate + beta[expected market return risk free rate] Beta: an overall measure of the sensitivity of the behavior of the market. 3 + 1. 2[8-3] = 9% this is what you. Yes, because the holding period gain is greater than the capm. You would buy it because it"s undervalued and the current price is too low. No, because it is overvalued and it is less than capm so you wouldn"t buy. If holding period gain < capm, don"t buy. Properly price and provide all information for the stock market. Weak-form emh: stock prices already reflect all information contained in the history of trading. Semi strong-form emh: stock prices already reflect all public information. Strong-form emh: stock prices already reflect all relevant information, including inside information.