ECON 200 Lecture 37: Competitive Markets Supply Curve

22

ECON 200 Full Course Notes

Verified Note

22 documents

Document Summary

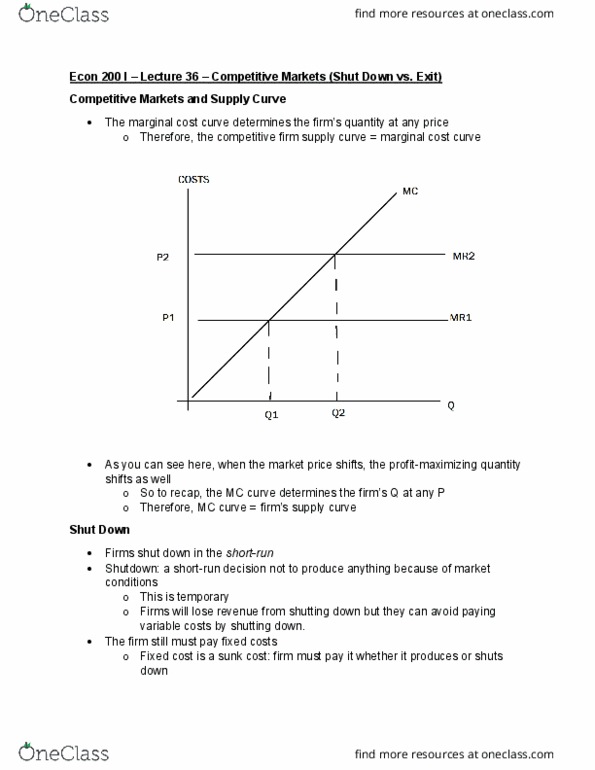

Econ 200 i lecture 37 competitive firm supply curve. All existing firms and potential entrants have identical costs. Each firm"s costs do not change as other firms enter or exit the market. The number of firms in the market is: fixed in the short run (because of fixed costs, variable in the long run (because of free entry and exit) Each firm"s short-run supply curve is its mc curve above avc: as long as p > avc, each firm will produce q where p = mc. The short-run market supply curve adds up quantity supplied by each firm at every given price. Number of firms can change because of free entry and exit in the long run. If existing firms profit (p > atc), new firms will enter: thus, the short-run market supply curve will shift right (because more firms), p falls.