ECO 211 Lecture Notes - Lecture 8: Perfect Competition, Takers, Fixed Cost

9 Sep 2016

School

Department

Course

Professor

1

ECO 211 Full Course Notes

Verified Note

1 document

Document Summary

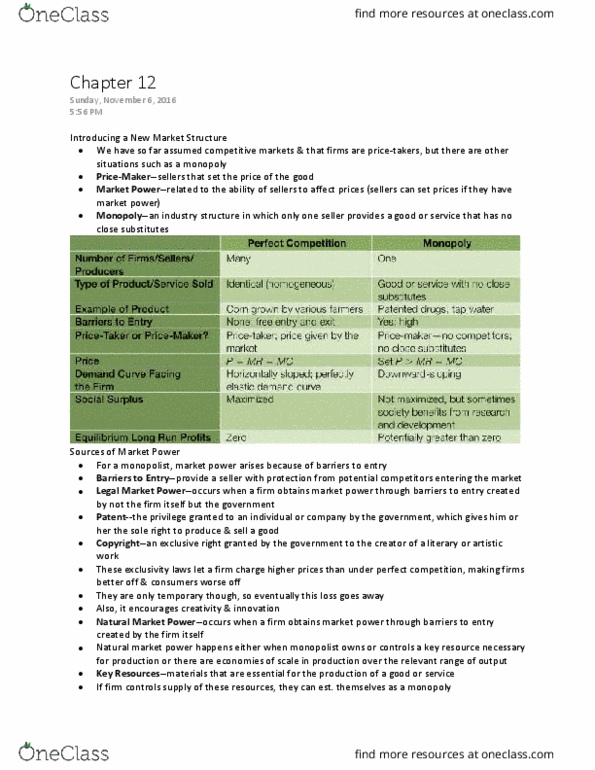

Questions over whether there really exists perfect competition anywhere. Prices different sometimes even within same thing (ex: gas price differs by location such as near airport) Assumptions underlying the competitive model (perfect competition) (competition=perfect competition) Buyers small relative to total market, so are sellers. Free entry & exit zero profit in long run. Easy for firms to get into market, easy to get out. They do(cid:374)"t i(cid:374)flue(cid:374)ce price (cid:894)there are so (cid:373)a(cid:374)y of the(cid:373)(cid:895), ca(cid:374) sell as (cid:373)uch as they (cid:449)a(cid:374)t at (cid:373)arket price. All firms producing exactly same thing, standardized product. Leads to all adopting same technology, looking same. If you do(cid:374)"t use the co(cid:373)petiti(cid:448)e (cid:373)odel, it does(cid:374)"t (cid:449)ork. Firms will find absolute best technology to use (survival of the fittest) Firms that don"t use best technology, profit <0. Must pick best technology & best scale of output, bottom of average cost curve. New technology lower average cost, makes new price at new bottom of curve.