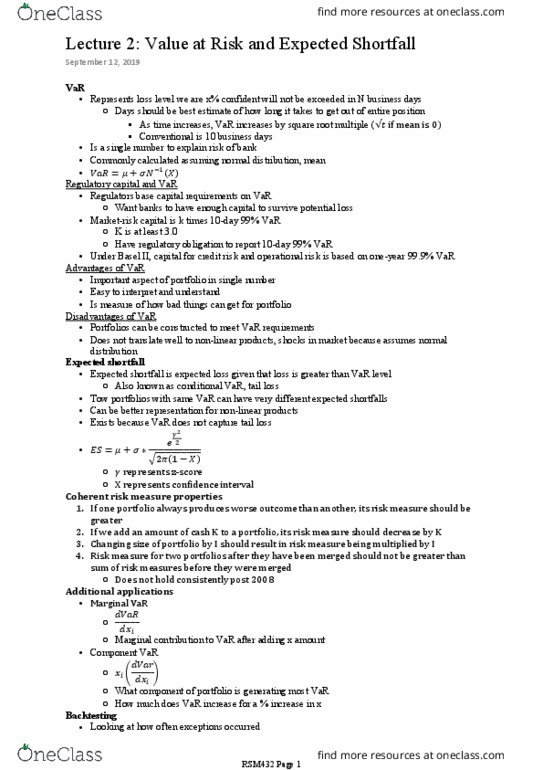

Can you tell me What does this article tell us about the bond markets performance and the interest rate environment?

Long-Term Government Bonds Shine as Fed Goes Slow

Pimco, Vanguard funds with focus on long-term debt beat out other bond funds in the 1st quarter

For investors, one of the best bets of 2016 has been a wager via U.S. Treasurys on falling interest rates.

A Pimco long-term government-bond fund was the best performer among bond funds in the first quarter. Above, Pimco offices in Newport Beach, Calif. PHOTO: MIKE BLAKE/REUTERS

The $460 million Pimco Extended Duration Fund posted a total return of 11.8% in the first quarter, making it the best performer among 2,015 U.S.-based bond mutual funds, according to data from Morningstar. Total return reflects price gains plus periodic payments.

The runner-up was $1.3 billion Vanguard Extended Duration Treasury Index Fund, which returned 11.7% during the quarter, according to Morningstar.

Both funds posted their best returns since the last quarter of 2014 and have extended those gains in the early days of the second quarter. Duration refers to a fundâs exposure to interest-rate risk, meaning its prices will rise more when rates fall and fall more when rates rise.

Analysts have warned repeatedly that bets on duration are risky, given the long decline in interest rates over recent years. The gains are striking at a time when stocks and other riskier assets have rebounded from an early-year selloff that at one point left the Dow industrials down 10%. The Dow fell 20.55 points, or 0.1%, on Monday, but is up 0.8% for the year.

Advertisement

While safer securities such as U.S. Treasurys and German bunds tend to decline in price when stocks and low-rated corporate bonds rally, many analysts say the simultaneous rise of safer and riskier assets this spring is tied to the unexpectedly slow pace of policy tightening by the Federal Reserve, along with signs the global economy continues its slow healing.

MORE IN MARKETS

A Measure of Stock-Market âFearâ Just Hit an All-Time High

Spreads Point to Growing Stress in Japanese Government Bond Market

By One Measure, U.S. Rates Are Already Negative

At the same time, many investors are concerned that the rally in stocks, bonds and commodities off Feb. 11 lows may have gone too far too fast.

âWe are still stuck in low growth,ââ Jack Flaherty,portfolio manager at money manager GAM, which has over $119 billion in global assets under management. âIt may be time to lighten up a bit and pauseâ on purchases of riskier assets, he said.

The uncertainty is why many investors are buying long-term U.S. government bonds, even though analysts have warned that slim yields leave bondholders vulnerable to potentially large capital losses if interest rates do rise.

The average U.S. equity mutual fund posted a total return of minus-0.4% between January and March, according to Morningstar. The average return for all U.S.-based bond funds tracked by Morningstar was 2.1% for the period. Quarter-end data for all funds are typically finalized in the early days of the following period.

âIt has been a good start for bond funds,ââ said Jeff Tjornehoj, head of Americas research at Lipper. That performance âmay be hard to repeat this quarter.â

Stock funds on average returned 4.4% in the fourth quarter last year, according to Morningstar. Bond funds posted a negative 0.1% return in the final quarter of 2015.

U.S. Treasury bonds overall have posted a total return of 3.6% this year through Friday, according to data from Barclays. U.S. bonds sold by lower-rated firms, or junk bonds, have returned 3.8% over the same period. S&P 500 has returned 0.8%, according to FactSet.

The Vanguard fund passively tracks an index of long-term Treasury bonds. The fund âwill tend to have extreme resultsâboth on the up and down sideââ given its focus on buying government bonds with very long-term maturity, said a representative of Vanguard in a written statement.

The Pimco fund is actively managed by three fund managers at Pacific Investment Management Co.: Stephen Rodosky, Michael Cudzil and Josh Thimons. A representative at Pimco declined to comment.

The Pimco fund attracted $19.7 million of new cash between January and February, topping the $11.9 million it obtained for the whole year of 2015, according to the latest data from fund tracker Lipper.

The Vanguard fund attracted $20.4 million of new cash during the first two months of the year, after suffering a net withdrawal of $115.7 million in 2015, according to Lipper.

The Vanguard fund posted a loss of 20.9% in 2013, according to Morningstar, when worries about the Fed reducing bond purchases rattled the bond market. The Pimco fund lost 21.2% that year.

But U.S. bond yields have largely been on a downward trend since the financial crisis. The two funds both posted an annualized return of about 17% on average over the past five years through Friday, according to Morningstar.