ACCT 209 Lecture Notes - Lecture 7: Compound Interest, Cash Flow, Interest

26 Mar 2017

School

Department

Course

Professor

Document Summary

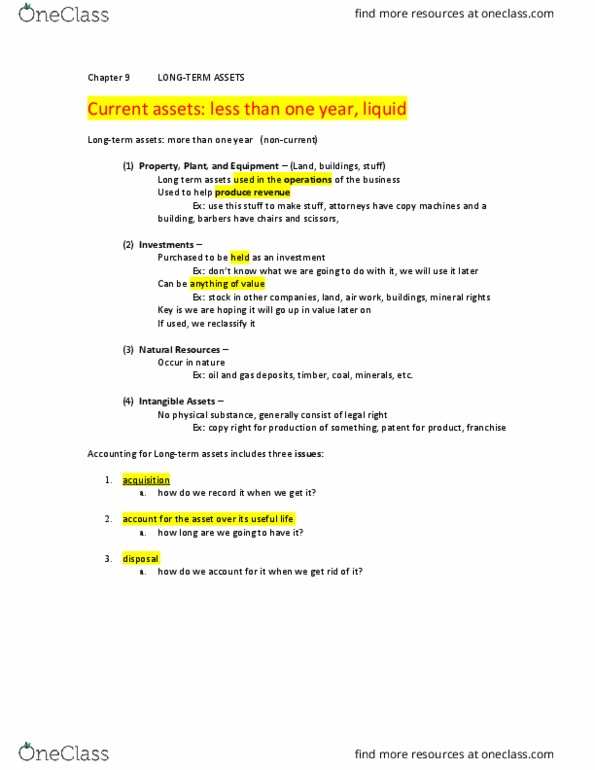

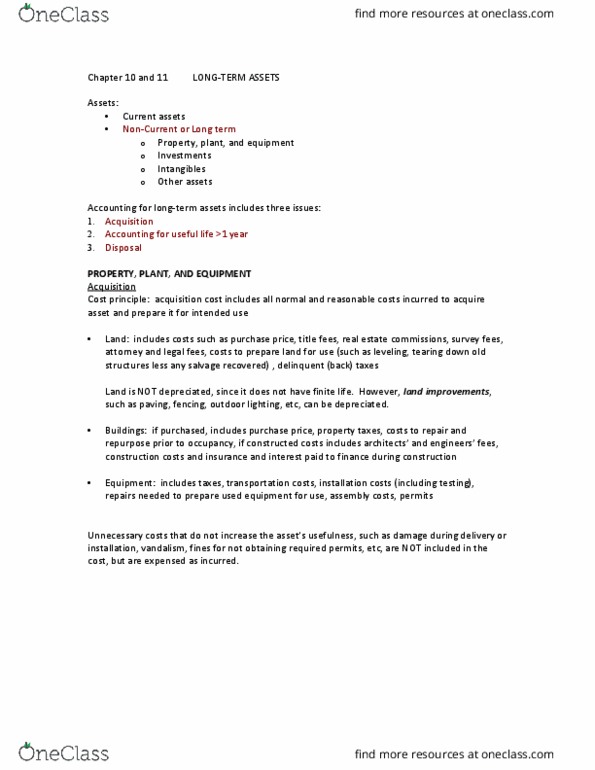

Current assets: cash, short term investment, accounts receivable, inv, prepaids, supplies. Long term assets: assets expected to benefit the firm for several accounting periods; relatively permanent. Accounting for long term assets includes three issues: acquisition, use over its service life. Cost principle: acquisition cost includes all normal and reasonable costs incurred to acquire asset and prepare it for intended use. Have a service life greater than one year. Are owned by the company for use in operations. Are not held for resale as part of the company"s normal operations (that is, they are not included in inventory) The cost of a long term asset generally includes the purchase price plus amounts incurred to get the asset in place and ready for use. Unnecessary costs that do not increase asset"s usefulness = expense. Ex: mistakes, damage during shipping or installation, vandalism, fines. Long term assets are used over several periods to produce revenue.