ECN 203 Lecture Notes - Lecture 4: Competitive Equilibrium, Economic Equilibrium, Perfect Competition

Document Summary

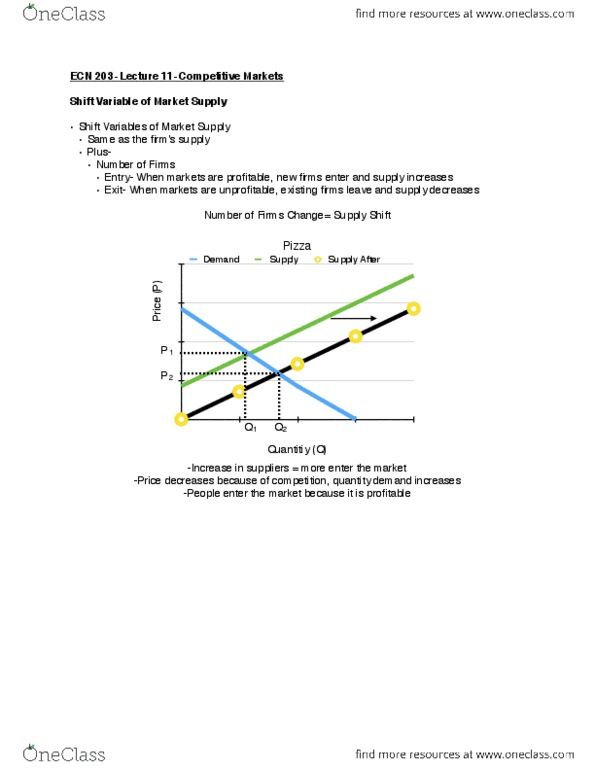

Steps to demonstrating how competitive markets reach a long-run competitive equilibrium: Representative firm showing marginal cost curve (the upward portion of the marginal cost is the firm"s supply line) Step 2: determine the price the individual firm faces. The price the firm receives is a horizontal line from the equilibrium price set in the market. Price is determined in the market so many buyers and sellers, the individual firm is a price-taker must take the price as given (conditions #1 and #2) Step 3: determine the demand facing the individual firm. Demand is horizontal at the price line (it"s also the marginal revenue and average revenue). Implies the firm will sell some quantity of the good at the going market price. If try to sell for a higher price, the buyers will go elsewhere (many competitors) perfectly elastic. Step 4: determine the quantity (q) the firm will produce. The firm will produce the quantity where mc=p.