ACC 252 Lecture Notes - Lecture 4: Contribution Margin, Robust Statistics, Earnings Before Interest And Taxes

17 Aug 2016

School

Department

Course

Professor

Document Summary

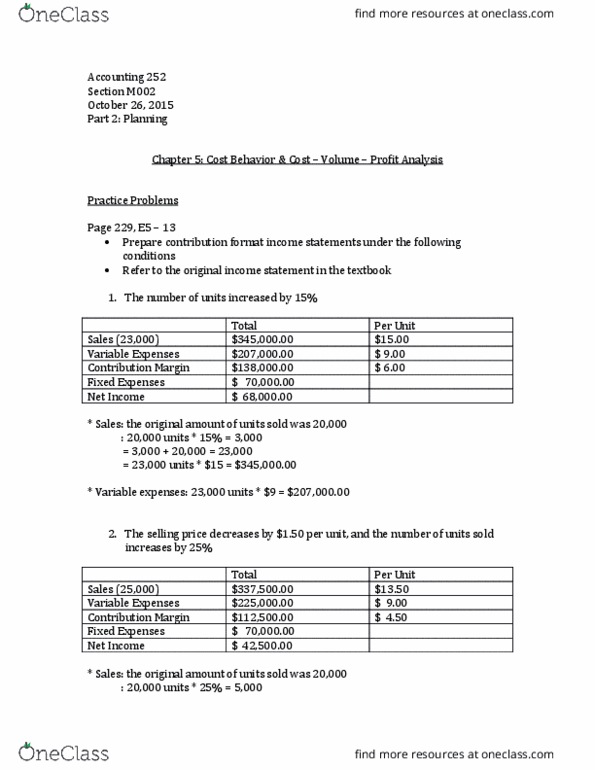

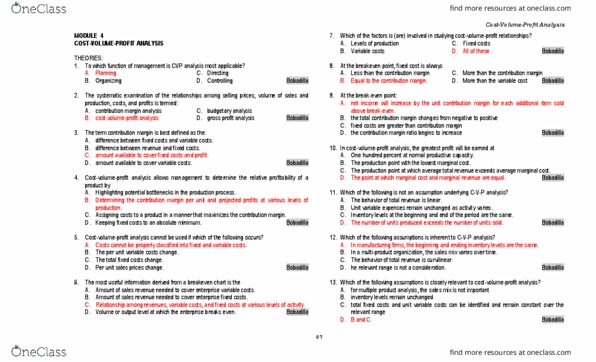

Chapter 5: cost behavior & cost volume profit analysis. Examines cost behavior patterns that underlie the relationships among cost, sales, volume and profit. What if analysis > assists decision making -> relies on the contribution format of the i/s. The behavior of variable and fixed costs can be measured accurately. Costs and revenues have a close linear approximation. The sales mix does not change during periods. Production and sales volume are roughly equal. * breakdown point and target profit go hand in hand. Number of units sold at which total revenue equals total costs. Unit sales to break even = fixed costs/cm per unit. Dollar sales to break even = fixed costs/cm ratio. Number of units that must be sold to generate a targeted/desired level of profit. Unit sales to attain the target profit = (fixed costs + target profit)/cm per. The degree of operating leverage: a measure of how much percentage change in sales volume will affect profits.