ECON 174 Lecture Notes - Lecture 13: Autoregressive Integrated Moving Average, Independent And Identically Distributed Random Variables

14 Feb 2020

School

Department

Course

Professor

Document Summary

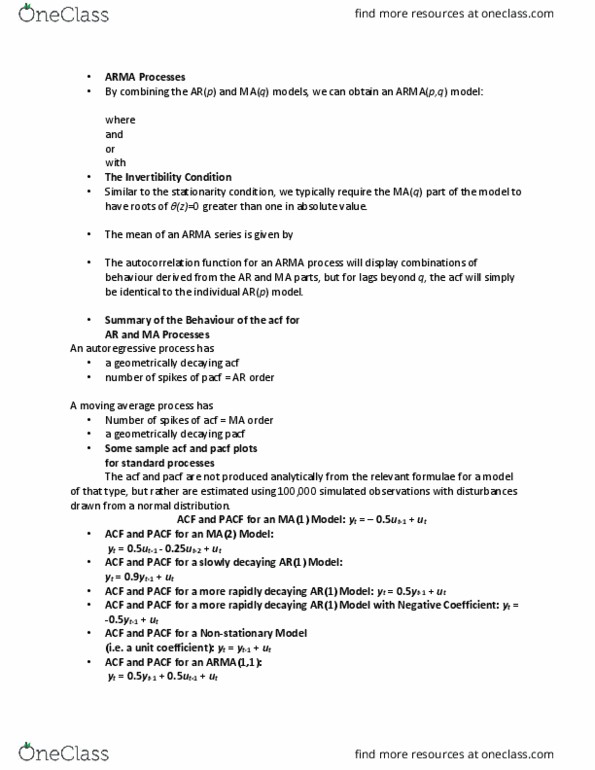

Ma (1) : yt = c + et + 1et-1. Depends on outcome of shock process (of last period) and the shock period. Ma(2): yt = c + et + 1et-1 + 2et-2. Ma(q) : yt = c + et + 1et-1 + 2et-2 + + qet-q. For all, assume that et is some iid(o, 2) & every ma process is stationary with mean c. Acf of an ma(1): corr (yt, yt-1) = corr (c + et + 1et-1, c + et-1 + 1et-2 ) = 1. 2nd lag: corr (yt, yt-2) = corr (c + et + 1et-1, c + et-2 + 1et-3 ) = 0. Ma(q) process has significant acf up to lag q, drops to zero for lags > q. C s cancel out b/c they"re constants and don"t affect correlation. Et are independent of each other and can also be cancelled out. All cancel out and aren"t correlated so =0.