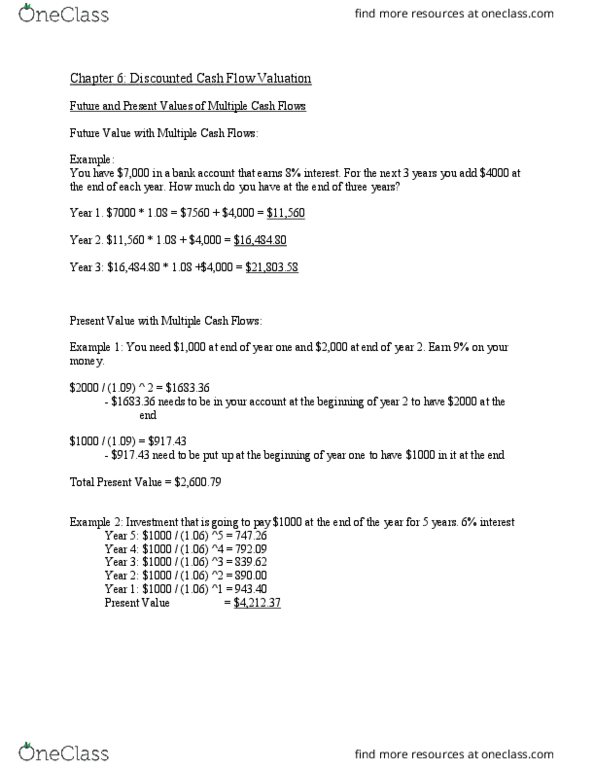

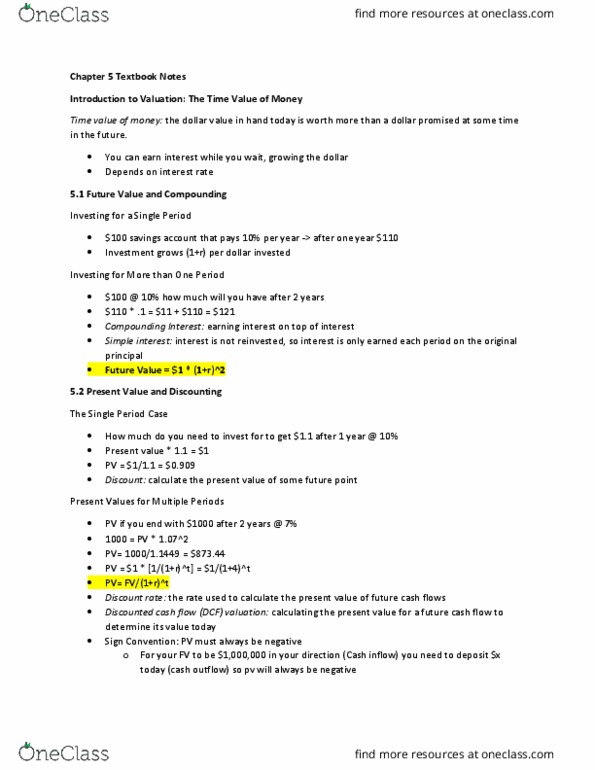

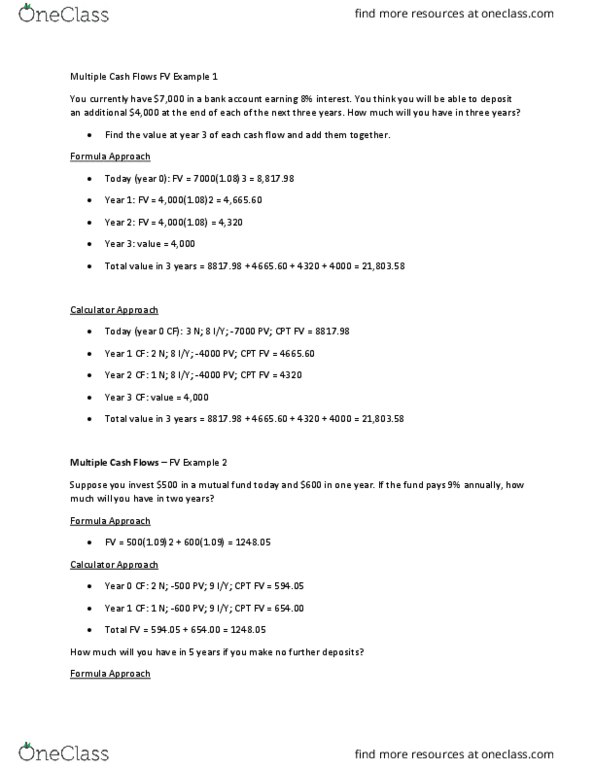

33:390:310 Lecture 6: Chapter 6 Multiple Cash Flows 9-19 Class notes

Document Summary

Get access

Related Documents

Related Questions

Question 1 5 pts

0 multiple_choice_question 22046808

The internal rate of return (IRR) is the interest rate that sets the net present value of the future cash flows equal to ________.

The internal rate of return (IRR) is the interest rate that sets the net present value of the future cash flows equal to ________.

| zero |

| one |

| one hundred |

| none of the above |

Question 2 5 pts

On a timeline, the space between date 0 and date 1 represents the _______ between dates. Letâs assume it is the first year of the loan. Date 0 is the beginning of the first year, and date 1 is the end of the first year.

On a timeline, the space between date 0 and date 1 represents the _______ between dates. Letâs assume it is the first year of the loan. Date 0 is the beginning of the first year, and date 1 is the end of the first year.

| dollar amount |

| present value |

| time period |

| future value |

Question 3 5 pts

As the interest rate __________, present value decreases.

As the interest rate __________, present value decreases.

| decreases |

| increases |

| remains unchanged |

| is unrelated |

Question 4 5 pts

The present value (PV) of a stream of cash flows is the _______ the present values of each individual cash flow

The present value (PV) of a stream of cash flows is the _______ the present values of each individual cash flow

| difference between |

| product of |

| sum of |

| same as |

Question 5 5 pts

When a constant cash flow will occur at regular intervals for a finite number of periods of time, it is called a(n) __________.

When a constant cash flow will occur at regular intervals for a finite number of periods of time, it is called a(n) __________.

| annuity |

| perpetuity |

| interest payment |

| principle payment |

Question 6 5 pts

Edit this Question Delete this Question

0 multiple_choice_question 22047052

There are two basic types of annuities:

There are two basic types of annuities:

| Discounted and compounded annuities |

| Ordinary annuities and annuities due. |

| Future value and present value annuities |

| None of the above |

Question 7 5 pts

The NPV measures the ______ change in shareholder wealth that arises from undertaking a project.

The NPV measures the ______ change in shareholder wealth that arises from undertaking a project.

| consistent |

| dollar |

| annual |

| semi-annual |

Question 8 5 pts

The Net Present Value rule implies that we should compare a projectâs net present value (NPV) to ________

The Net Present Value rule implies that we should compare a projectâs net present value (NPV) to ________

| zero |

| one |

| 100 |

| none of the above |

Question 9 5 pts

To endow a perpetuity is the same as calculating the present value (PV) of a perpetuity. Say you want to endow an annual graduation party at your alma mater. You want the event to be a memorable one, so you budget $30,000 per year forever for the party. If the university earns 8% per year on its investments, and if the first party is in one yearâs time, how much will you need to donate to endow the party?

The formula for PV of a perpetuity = C\r; = $30,000 \ 0.08; =

To endow a perpetuity is the same as calculating the present value (PV) of a perpetuity. Say you want to endow an annual graduation party at your alma mater. You want the event to be a memorable one, so you budget $30,000 per year forever for the party. If the university earns 8% per year on its investments, and if the first party is in one yearâs time, how much will you need to donate to endow the party?

The formula for PV of a perpetuity = C\r; = $30,000 \ 0.08; =

| $3,750 |

| $37,500 |

| $375,000 |

| $3,750,000 |

Question 10 5 pts

With an Ordinary Annuity, payments are required at the ________ of each period. An example of this is bonds which usually pay coupon payments at the end of every six months until the bond's maturity date.

With an Ordinary Annuity, payments are required at the ________ of each period. An example of this is bonds which usually pay coupon payments at the end of every six months until the bond's maturity date.

| beginning |

| middle |

| end |

| payments are not required |

Assume that you are nearing graduation and that you have appliedfor a job with a local bank. As part of the bankâs evaluationprocess, you have been asked to take an examination that coversseveral financial analysis techniques. The first section of thetest addresses time value of money analysis. See how you would doby answering the following questions:

a. Drawcash flow time lines for (1) a $100 lump-sum cash flow at the endof Year 2, (2) an ordinary annuity of $100 per year for threeyears, (3) an uneven cash flow stream of $50, $100, $75, and $50 atthe end of Years 0 through 3.

b. (1)What is the future value of an initial $100 after three years if itis invested in an account paying 10%annual interest?

(2) What is the present value of $100 to bereceived in three years if the appropriate interest rate is10%?

c. Wesometimes need to find how long it will take a sum of money (oranything else) to grow to some specified amount. For example, if acompanyâs sales are growing at a rate of 20%per year, approximatelyhow long will it take sales to triple?

d. Whatis the difference between an ordinary annuity and an annuity due?What type of annuity is shown in the following cash flow time line?How would you change it to the other type of annuity?

0 1 2 3

100 100 100

e. (1)What is the future value of a 3-year ordinary annuity of $100 ifthe appropriate interest rate is 10%?

(2) What is the present value of the annuity?

(3) What would the future and present values be ifthe annuity were an annuity due?

f. What is the present value of the following uneven cash flow stream?The appropriate interest rate is 10%, compounded annually.

0 1 2 3 4

100 300 300 150

g. Whatannual interest rate will cause $100 to grow to $125.97 in 3years?

h. (1)Will the future value be larger or smaller if we compound aninitial amount more often than annuallyâfor example, every 6months, or semiannuallyâholding the stated interest rateconstant? Why?

(2) Define the stated, or quoted, or simple, rate,(rSIMPLE), annual percentage rate (APR), the periodicrate (rPER), and the effective annual rate(rEAR).

(3) What is the effective annual rate for a simplerate of 10%, compounded semiannually? Compounded quarterly?Compounded daily?

(4) What is the future value of $100 after threeyears under 10%semiannual compounding? Quarterly compounding?

i. Will the effective annual rate ever be equal to the simple (quoted)rate? Explain.

j. (1) What is the value at the end of Year 3 of thefollowing cash flow stream if the quoted interest rate is 10%,compounded semiannually?

0 1 2 3

100 100 100

(2) What is the PV of the same stream?

(3) Is the stream an annuity?

(4) An important rule is that you should nevershow a simple rate on a time line or use it in calculations unlesswhat condition holds? (Hint: Think of annual compounding,when rSIMPLE = rEAR = rPER.) Whatwould be wrong with your answer to parts (1) and (2) if you usedthe simple rate 10%rather than the periodic raterSIMPLE/2 = 10%/2 = 5%?

k. (1)Construct an amortization schedule for a $1,000 loan that has a10%annual interest rate that is repaid in three equalinstallments.

(2) What is the annual interest expense for theborrower, and the annual interest income for the lender, duringYear 2?

l. Suppose on January 1 you deposit $100 in an account that pays asimple, or quoted, interest rate of 11.33463%, with interest added(compounded) daily. How much will you have in your account onOctober 1, or after 9 months?

m. Now suppose youleave your money in the bank for 21 months. Thus, on January 1 youdeposit $100 in an account that pays a 11.33463%compounded daily.How much will be in your account on October 1 of the followingyear?

n. Suppose someone offered to sell you a note that calls for a $1,000payment 15 months from today. The person offers to sell the notefor $850. You have $850 in a bank time deposit (savings instrument)that pays a 6.76649%simple rate with daily compounding, which is a7%effective annual interest rate; and you plan to leave this moneyin the bank unless you buy the note. The note is not riskyâthat is,you are sure it will be paid on schedule. Should you buy the note?Check the decision in three ways: (1) by comparing your futurevalue if you buy the note versus leaving your money in the bank,(2) by comparing the PV of the note with your current bankinvestment, and (3) by comparing the rEAR on the notewith that of the bank investment.

o. Suppose the note discussed in part n, above, costs $850, but callsfor five quarterly payments of $190 each, with the first paymentdue in 3 months rather than $1,000 at the end of 15 months. Wouldit be a good investment?