33:010:272 Lecture Notes - Lecture 11: Current Liability, Accrual, Negative Number

25 Aug 2016

School

Department

Course

Professor

Document Summary

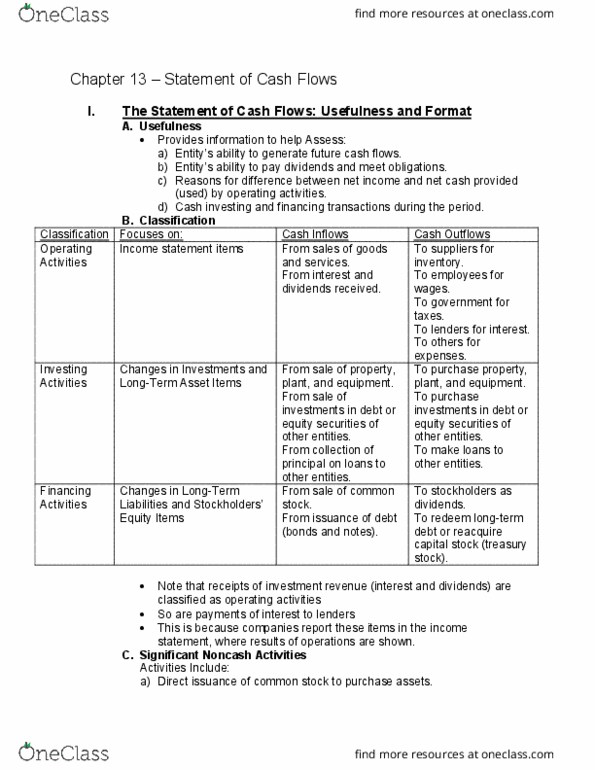

Chapter 13 statement of cash flows: usefulness of the statement of cash flows, reasons for difference between net income and net cash provided by operating activities, classification of cash flows -> memorize, operating activities a. i. Stockholders" equity: for noncash activities, reported at the bottom as footnote, examples b. i. Exchanges of plant assets: format and method a. 99% indirect method: preparing, three sources of info a. i. Tells you more about what happen to cash. Will be given: (1) operating activities section, purpose a. i. To convert net income from accrual basis to cash basis: steps b. i. Add back any losses and subtract any gains on sale of plant assets/ investments (income statement) b. iv. Calculate the changes in current assets and current liabilities (comparative balance sheet) b. iv. 1. Increase in asset -> decrease in cash b. iv. 1. b. Increase in liabilities and equity-> increase in cash b. iv. 1. d. Decrease in liabilities and equity -> decrease in cash: tips c. i.