ACCT-110 Lecture Notes - Lecture 5: Fifo (Computing And Electronics), Weighted Arithmetic Mean

Document Summary

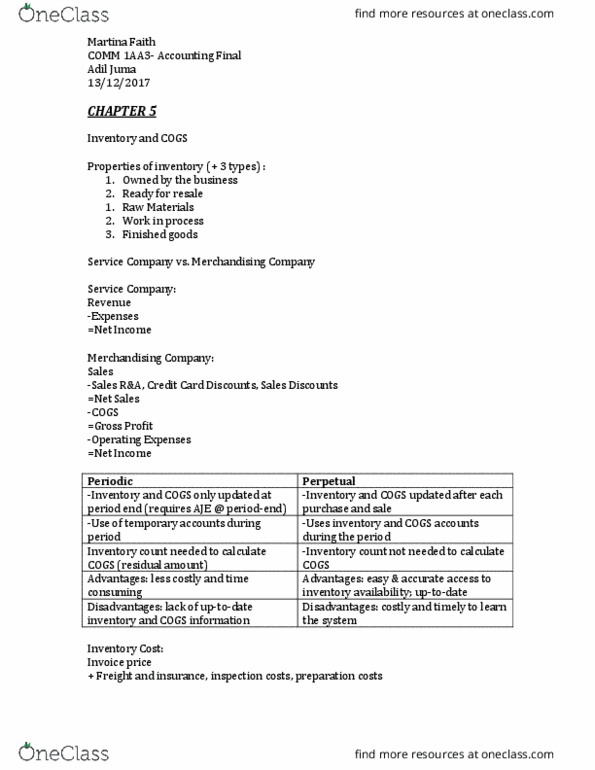

Companies must periodically inspect and write off those items. Freight & storage costs to get the items to the saleable location (not warehousing costs). Inventory = all goods owned by the company, regardless of location. Fob shipping point = buyer pays freight; title transfers at sellers dock. Fob destination = seller pays freight; title transfers at buyers dock. Inventory must not include damaged or obsolete goods. Inventory = invoice cost - discounts + insurance + import duties + freight + storage. Most companies take physical inventories (count) on a regular basis and compare the counts to what is on the books (balance sheet). Discrepancies result in write offs (expense) or add backs (increase inventory). Perpetual inventory systems = updated in real time. Periodic inventory system = updated regularly but not real time. Fifo = first in, first out = oldest items charged to cogs first. Lifo = last in, first out = newest items charged to cogs first.