MGMT 20000 Lecture Notes - Lecture 9: Accounts Receivable, Income Statement

13 Feb 2019

School

Department

Course

Professor

Document Summary

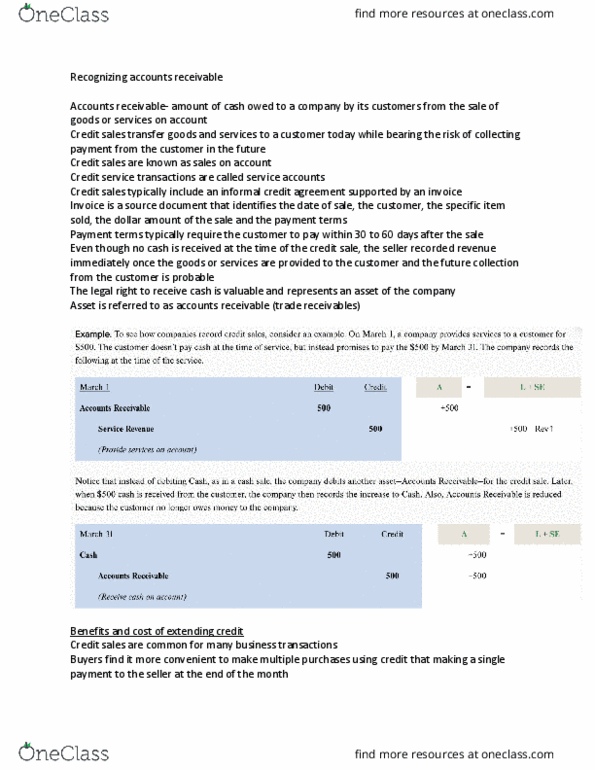

Cash owed to the company by its customers from sales or services on account (trade receivables) Nontrade-receivables that originate from sources other than customers. Notes receivable-formal credit arrangements evidenced by written debt instruments. Calculate net revenue using discounts, returns, and allowances. Reduction in a list price of a product or service. Used to provide incentives to larger customers or certain customer groups. Recognized by recording revenue for lower amount. Sales allowance-customer does not return a product and a portion of sales price refunded. Seller issues a cash refund if original sale was for cash. Seller reduces balance of accounts receivable if original sale was on account. Reported with total revenues in the income statement. Offer a customer a reduction if payment is made within a specific period of time. ,000 credit sale with terms 2/10, n/30 (2% discount if paid in 10 days or full in 30) Sales discounts are recorded as a contra revenue account.