ECON 102 Lecture Notes - Lecture 12: Diminishing Returns, Marginal Product, Production Function

1

ECON 102 Full Course Notes

Verified Note

1 document

Document Summary

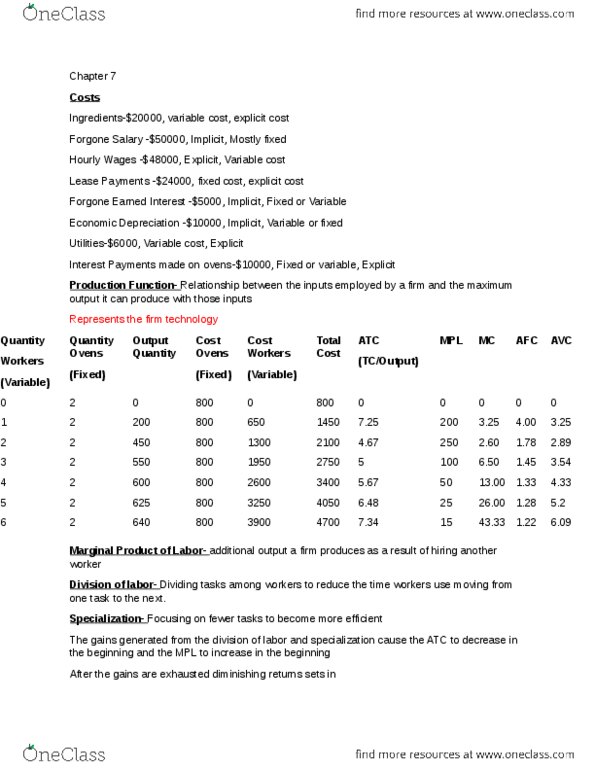

Production function- describes the relationship between the quantity of inputs and the quantity of output it produces. Quantity of input is xed for a period of time. If we can easily change the amount at any time, it"s considered variable example: water, aluminum, labor, insurance, electricity. The relationship between inputs and output is positive but not constant: marginal product of labor changes along the production function (diminishing returns) Marginal product of an input- the additional quantity of output that is produced by using one more unit of that input. Marginal product of labor = change in quantity of output / change in quantity of labor. Diminishing returns: we have diminishing returns on the assumption that all else is held equal. If other inputs are xed, each successive unit of an input will raise production by less than the last. With more space, each worker can produce more.