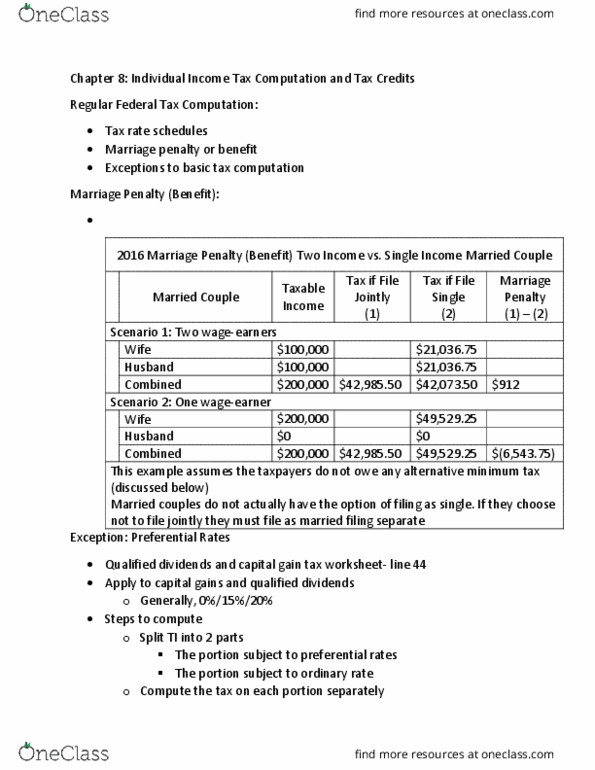

ACCT 421 Lecture Notes - Lecture 3: Adjusted Gross Income, Alternative Minimum Tax, Child Tax Credit

17 Sep 2016

School

Department

Course

Professor

Document Summary

Chapter 4: individual income tax overview, exemptions, and filing status. Income from all sources exclusions = gross income. Gross income for agi deductions = adjusted gross income (agi) Adjusted gross income (agi) from agi deductions = taxable income: from agi deductions. Taxable income x tax rates = income tax liability. Income tax liability + other taxes = total tax. Total tax credits prepayments= taxes due or refund. Realization: all-inclusive irc 61, exclusions vs deferrals. Exclusion- income that you never pay taxes on (permanent) Character- how the income is taxed (not all income is taxed the same way: ordinary. Wages, rental income, interest income: capital. Income that comes from the disposition of assets that is taxed at preferential rates (lower rate) For agi: known as above the line . End of page 1: tend to be associated with business activities and certain investing activities. From agi: known as below the line , tend to be personal in nature.