ACCT 421 Lecture Notes - Lecture 6: Flexible Spending Account, Itemized Deduction, Plastic Surgery

21 Oct 2016

School

Department

Course

Professor

Document Summary

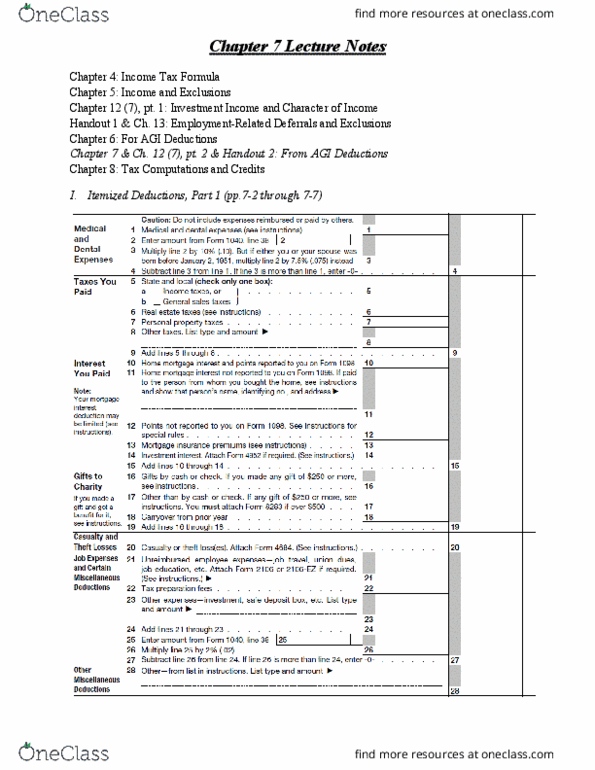

Important to understand the differences between: business expenses- deductible under 162 and are deductions for. Agi: expenses uncured for the production of income-itemized deductions under 212, except rent/royalty expenses, itemized deductions- expenses that are essentially personal but either subsidize desirable activities or consider the wherewithal to pay. Allowed for: care, prevention, diagnosis or cure of injury, disease, or bodily fu(cid:374)ctio(cid:374) to exte(cid:374)t a(cid:373)ou(cid:374)ts exceed (cid:1005)(cid:1004)% of agi ((cid:1011). (cid:1009)% if (cid:1010)(cid:1009) through. Includes: prescription medication, medical aids, payments to providers, transportation, hospitals, ltc, premiums. Does not include: amounts reimbursed or paid for through flexible spending account, unnecessary cosmetic surgery. Local and foreign income taxes: sales tax in lieu of state and local. Tax fees: fees are not deductible. Investment interest: limited to net investment income. Qualified residence interest: only allowed on principal residence + one other, acquisition indebtness: Secured by the property and used to acquire, construct or substantially improve.