ACCT 1209 Lecture Notes - Lecture 32: Cash Flow Statement, Income Statement, Accounts Receivable

15 Apr 2016

School

Department

Course

Professor

Document Summary

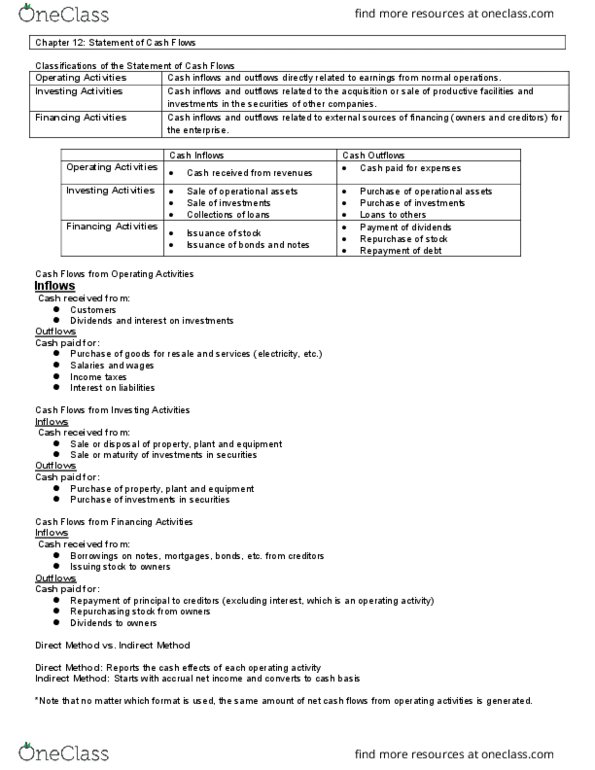

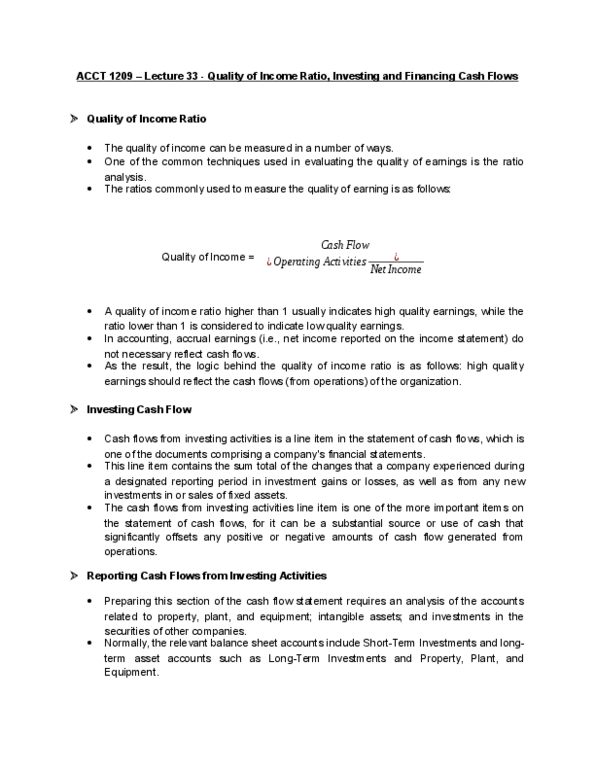

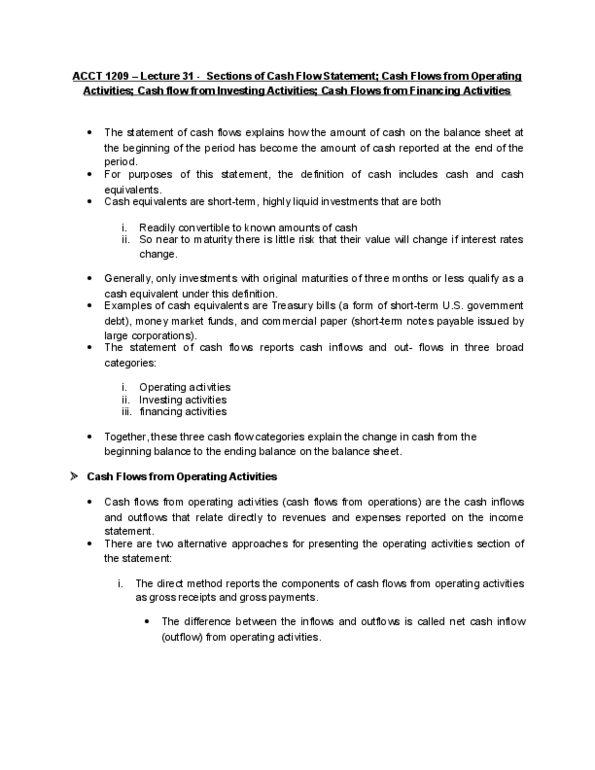

Acct 1209 lecture 32 net increase (decrease) in cash; reporting and interpreting. The combination of the net cash flows from operating activities, investing activities, and financing activities must equal the net increase (decrease) in cash for the reporting period. Reporting and interpreting cash flows from operating activities. Cash flow from operating activities is always the same regardless of whether it is computed using the direct or indirect method. The investing and financing sections are always presented in the same manner regardless of the format of the operating section. The indirect method starts with net income and converts it to cash flows from operating activities. This involves adjusting net income for the differences in the timing of accrual basis net income and cash flows. The general structure of the operating activities section is: Completing the operating section using the indirect method involves two steps: