ACCT20100 Lecture Notes - Lecture 10: Income Statement, Contribution Margin, Cost Driver

17 views2 pages

21 Sep 2020

School

Department

Course

Professor

Document Summary

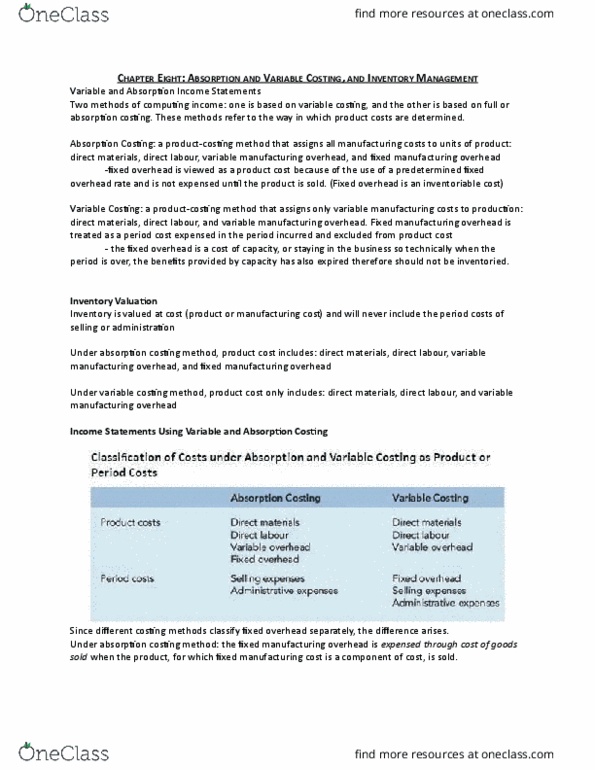

A cost driver is a factor, such as machine-hours, beds occupied, computer time, or flight- hours that causes overhead costs. Absorption costing is required under gaap but variable costing helps with operational decision making. Relationship between variable and absorption income based on production and sales: Segment: any part or activity of an organization about which a manager seeks cost, revenue, or profit data. Examples: an individual store, sales territory, service center. Traceable fixed costs: arise because of the existence of a particular segment and would disappear over time if the segment itself disappeared. Common fixed costs: arise because of the overall operation of the company and would not disappear if any particular segment were eliminated. Hiring and firing decisions are made on segment margin. Computed by subtracting traceable fixed costs from the segment"s contribution margin. Best gauge of long-run profitability of the segment. Common costs (are not allocated to the divisions) For the company analysis, include common costs.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers