ACCT 2000 Lecture Notes - Lecture 9: Deferral, Financial Statement, Income Statement

Document Summary

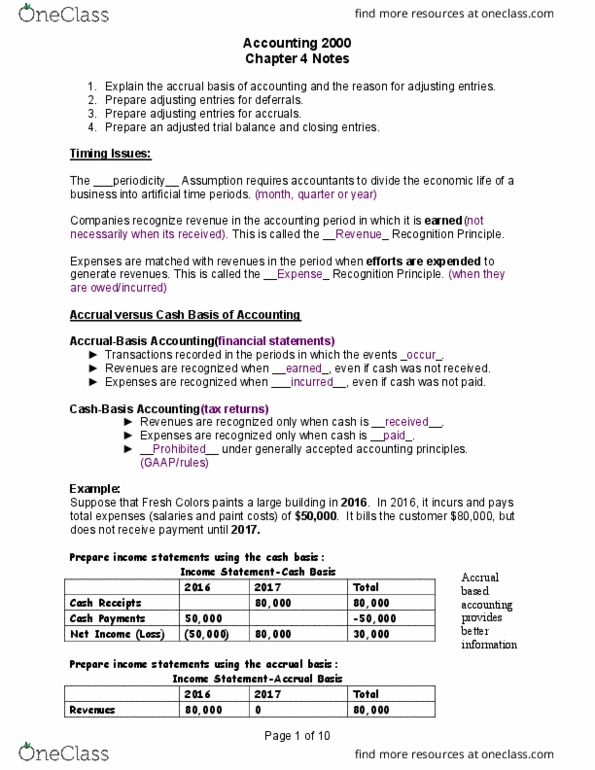

Adjusting entries are the movement of money between the balance sheet and income statement in order to get the account balances correct before financial statements are prepared. Adjusting entry one side of the entry (debit/credit) must come from the balance sheet (asset or liability) and one side of the entry (debit/credit) must come from the income statement (revenue/expense). Once account balances are correct (after adjusting entries), financial statements can be produced. Deferrals: prepaid expenses (examples prepaid insurance, supplies, depreciation) For amount used up: unearned revenue (example unearned ticket revenue) Accruals : accrued revenue revenue earned but not received (or billed) For amount earned: accrued expenses - expenses incurred (owed) but not yet paid. (example - interest, salaries, utilities)