CO SCI 136 Lecture Notes - Lecture 24: Arbitrage Pricing Theory, Capital Asset Pricing Model, Risk Premium

Document Summary

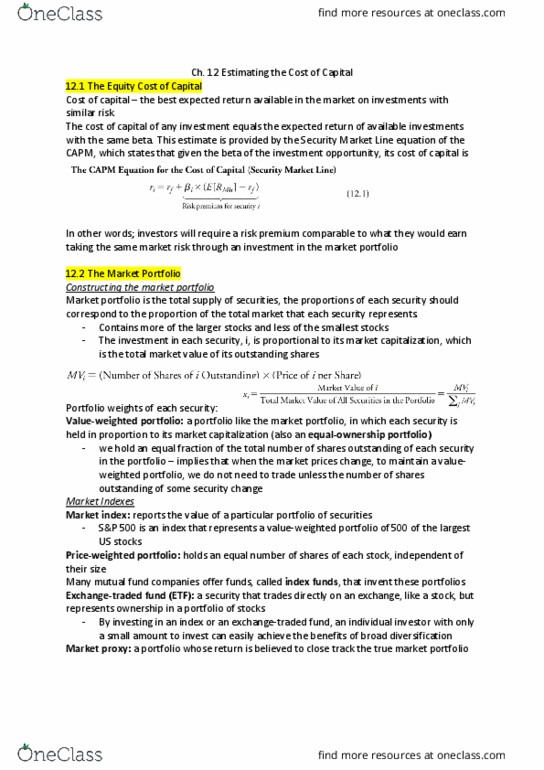

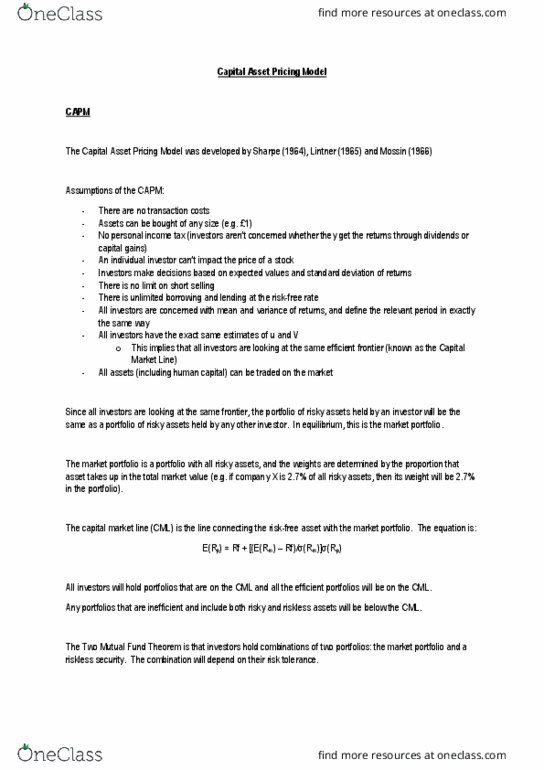

Chapter 7 - capital asset pricing and arbitrage pricing theory. The capm assumes investors are rational, single-period planners who agree on a common input list from security analysis and seek mean-variance optimal portfolios. These assumptions mean that all investors will hold identical risky portfolios. The capm implies that, in equilibrium, the market portfolio is the unique mean variance efficient tangency portfolio, which indicates that a passive strategy is efficient. The capm implies that the risk premium on any individual asset or portfolio is the product of the risk premium of the market portfolio + the asset"s beta. The security market line shows the return demanded by investors as a function of the beta of their investment. This expected return is a benchmark for evaluating investment performance. In a single-index security market, once an index is specified, a security beta can be estimated from a regression of the security"s excess return on the index"s excess return.