Need help revising, and recommendation for a conclusion.

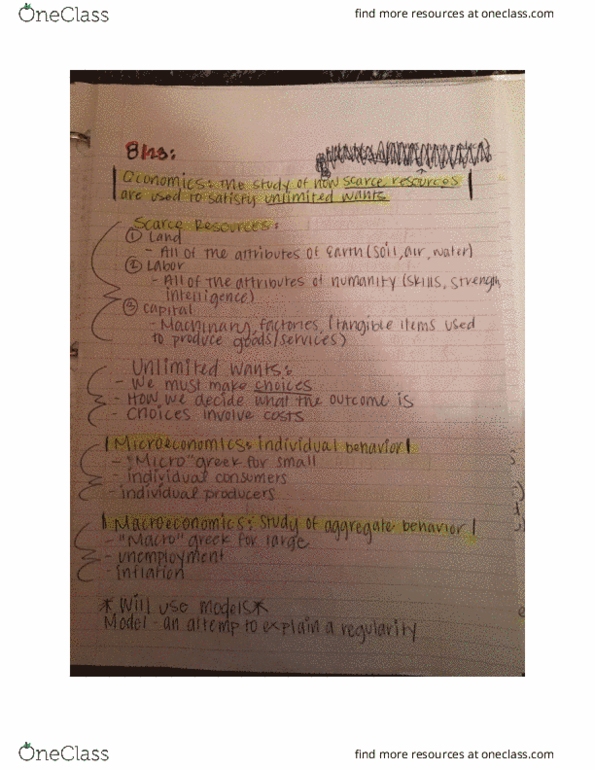

Throughout this paper is my understanding of what I have learned in class chapters 1-4, expressing my understanding and opinions. Economics is the study of how we deal with scarce resources. Microeconomics specially deals with business in the home country exclusively. This type of economics affects small businesses in the home country only. On the other hand, macroeconomics concerns our national welfare concerning trade and international business.

I believe that many things affect our economy on a microeconomics level. Things such as our understanding of our country in reflection to the world are very important. That is why we study ourselves before we study the macroeconomic principle of the world. Understanding ourselves is what microeconomics teaches us. Working from the inside out. The world is a place where there are differences in our wants and what we get. That is what makes items scarce. That is what positive economics is. Positive economics deals with what is and what we have. The other type of economics is called normative statements. This deals with what we should receive instead of what is and deserved to some extent. It's our scarce resources that determine our allocation of resources and how we use our resources and time. This is where opportunity costs come in, giving up something to do something. A successful business or country never ignores opportunity costs. We must ensure that we have a comparative advantage instead of the absolute advantage. Our resources must be used to achieve maximum output. Comparative is met when we have fewer opportunity costs to make some certain products than the other person or entity.

My initial understanding was scarcity was oil potentially running out, but we have so much of it that you can always find more with techniques such as fracking. Now it's obvious to me, one of our most scarce resources is time. You cannot avoid the 8,760 hours in a year. I understand that people have unlimited wants but limited resources. Everything has a cost and we must make a choice as we don't have unlimited farms, factories workers, etc. scarcity forces choices and this ties in with opportunity cost, for every gun made, a theft from the hungry is made. The opportunity cost not being used to feed the poor, but to make guns. And I find it easy to understand no one can have everything choices must be made on benefits. If I'm going to school, imp giving up making cash, as I'm giving up money for an education, I value education more. Scarcity is also related to the invisible hand. As it's an achievement that leads free markets and capitalism through competition for scarce resources.

My understanding of the invisible hand is a person neither intends to promote public interest and does not know how much he is promoting it. Only intending on his own gain. Without being his intention a person can be lead by the invisible hand to do good for society by pursuing one's own self-interest. Going into equity and efficiency the invisible hand does ensure both equity and efficiency. People work in their selfish ways to maximize profit while also contributing to the economy as a whole. It can also be argued that as the invisible hand wants to ensure efficiency, it cannot guarantee efficiency, because it can fail to produce an efficient allocation of resources, which in turn lead to a market failure. It can also be argued that it can't guarantee equity because not everyone gets a fair price. The way I like to remember efficiency is with a real-life example, like a reduction in the number of workers needed to produce a particular good for a particular amount. Equity refers to the ownership interest in an asset, for example, if a person owns a house with a market value of $800,000 and owes $100,000 on the mortgage leaving a $700,000 equity in the home.

It can be predicted that if the price of beef increases - ceteris paribus-the quantity of beef demanded by buys will decrease. In other words, if the price of beef increases, then the quantity of beef increases, then the quantity of beef demanded will decrease because all things have to be equal. In-class lecture thought me all other things remaining the same. Economists use ceteris paribus to determine the effect of a factor when all other factors have been held the same and helps simplify the study and get a more refined data set.

Economists deal with many issues that pertain to assuring that both a countries domestic output is efficient and that there is an effective trade balance. This means that there are a balance and limit on the amount of imports. Also, this means home production must be able to meet export demands. There are many factors that affect the production of goods and their effect on shifting the production possibilities frontier. This involves evaluating every detail including knowing the products and any close substitutes and compliments. It also involves knowing how an action or other external force will affect demand. This is called price elasticity; Substitutes are products that can replace any given product or service. An example of this would be Coke and Pepsi. The presence of substitutes affects price elasticity because if there are other options, then any change to the price or quality of the product will cause a shift of the demand curve. O course, price is a huge reason why the demand for a product decreases or increases yet it doesn't shift the curve because of the price only. This price change will cause a domino effect that will end with the shifting of the demand curve because it will cause an increase or decrease in demand of the substitute good if the price change is either lower or higher respectively. This price change serves as a catalyst that will change people's desire to spend more money on a more expensive product and that will instead choose to buy the substitute good for cheaper or buy more of the desired product. The change in the price of actual products will not shift the demand curve yet the change of the price of substitutes will because it serves to change people's purchasing behavior. On the other hand, compliments serve to boost demand when there is a decrease in price. The use of complementary goods is dependent upon another product. An example of this would be hot dogs and buns. If the price of hotdogs decreases then, conversely, the demand for hot dog buns will increase because of this change in price. In this scenario, the decrease in price will cause a positive shift in the demand curve because of people's desire and willingness to buy more buns. This is an example of a demand shifter. There are a few other demand shifters. The shifters of the demand curve are changes in expectations, disposable income, price of substitute goods and complements, tastes and preferences, and population size and composition. Changes in income affect the demand curve because if income is lower then people tend to save any extra income instead of wasting it. Disposable income is minimized and spending is lower. This also causes people to see a perceived value of things and distinguishing between what is necessary and what is a relative luxury. The lower the income, the higher the saving and avoidance to spend. An example of this would be if someone needs to buy some medication and it is relatively expensive, that doesn't mean that someone won't buy the medication just because it is expensive. It is necessary. Other factors that contribute to spending and demand are having a price ceiling and price floor. Having a price ceiling is a limit on the price of the product this is a government-imposed idea that is meant to protect consumers from unfair pricing and other conditions that may be malicious or obscure. This affects demand because if there is a price ceiling there is a limit on profit on a unit-to-unit basis. The other factor is the price floor. This price floor was created to encourage competition and affect consumers' willingness to pay because sometimes this new price may be higher than the original price. This causes a negative impact on a product that has a less than wanted perceived value. Many factors contribute to economic prosperity and certainly do help assure that information is analyzed and implemented into an economic and business plan.