ACCT 498 Lecture Notes - Lecture 9: Undue Influence, Professional Responsibility, Critical Thinking

23 Feb 2017

School

Department

Course

Professor

Document Summary

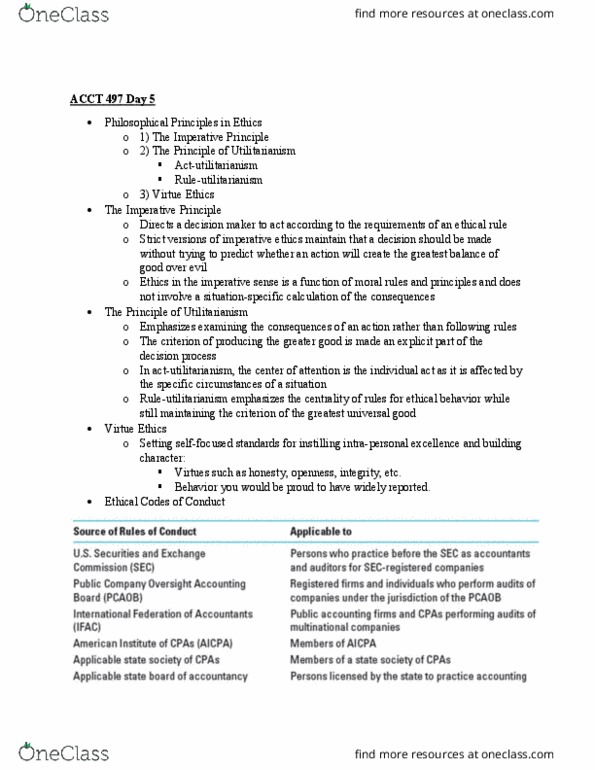

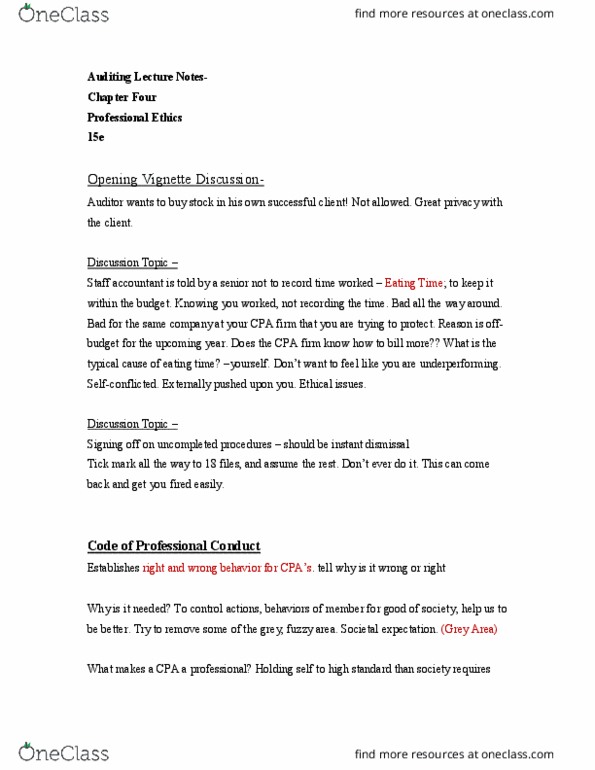

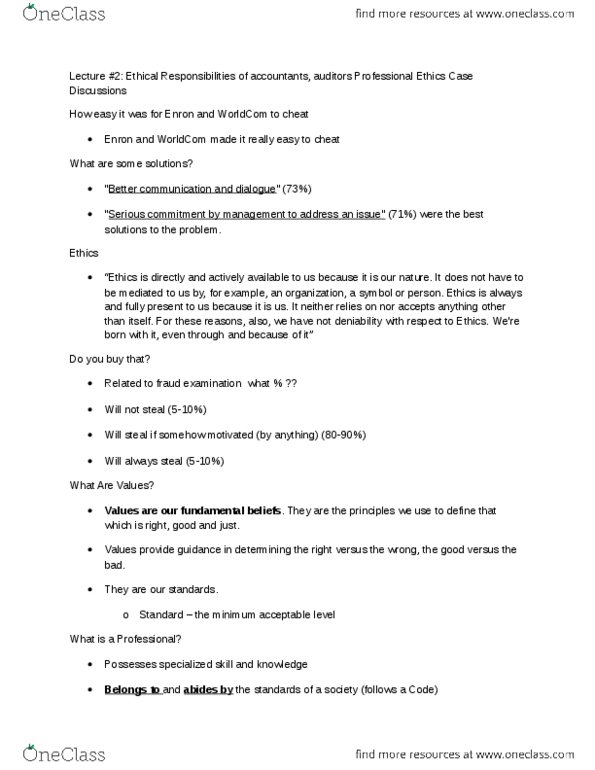

Critical thinking assignment: email electronic copy by 9am monday, february 13, a paper copy is handed in at the beginning of class, it is about the quality of your paper, not the length of your paper. Code principles: responsibilities principles (principle i, public interest principle (principle ii, integrity principle (principle iii) To maintain and broaden public confidence, members should perform all professional responsibilities with the highest sense on integrity [aicpa. The code defines integrity in sections 0. 300. 040. 02-04. However, this interpretation is quite general and does not tell us what integrity is. Members should observe both the form and spirt of technical and: objectivity and independence principle (principle iv) ethical standards. A member should maintain objectivity and be free of conflicts of interest in discharging professional responsibilities. A member in public practice should be independent in fact and appearance when providing auditing and other attestation services. [aicpa code section 0. 300. 050. 01: due care principle (principle v)