BUS 201 Lecture Notes - Lecture 3: Accrual, Financial Statement

15 May 2020

School

Department

Course

Professor

Document Summary

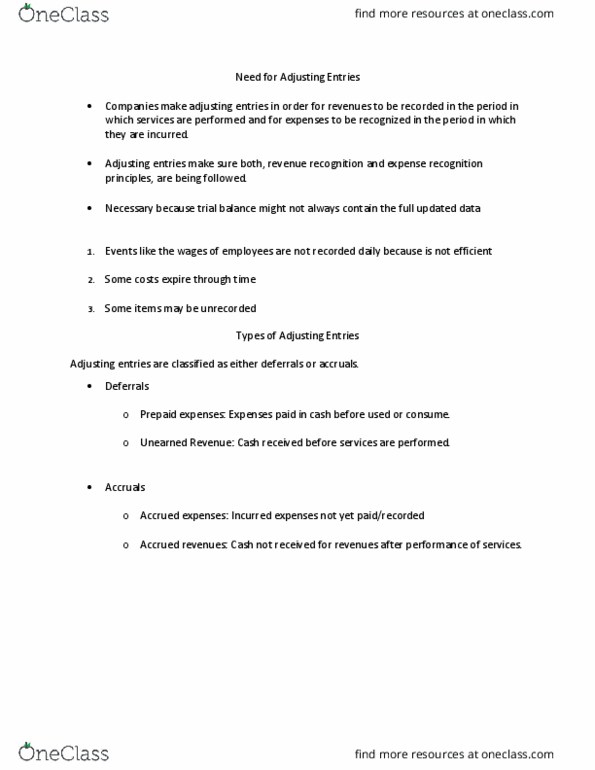

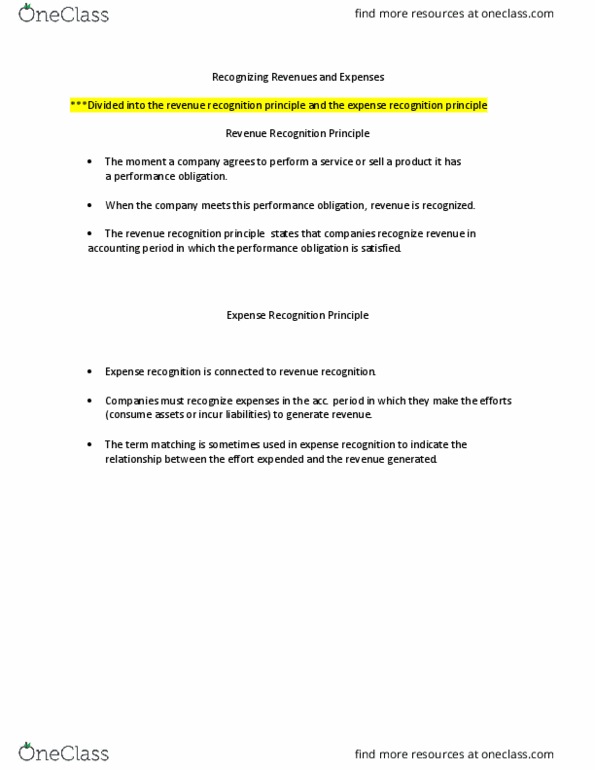

Companies record transactions and recognize revenues when they perform services, instead of receiving cash: same goes for expenses. Expenses are recognized when incurred rather than when paid): cash basis, revenue is recorded at the time cash is received, expenses are recognized at the time they pay out cash. It may produce misleading financial statements: for example, it fails to record revenue for a company that has performed services but has not yet received payment. ***in conclusion, accrual basis accounting is more compatible with accounting principles (gaap). ***small companies use cash basis because they often have few receivables and payables.