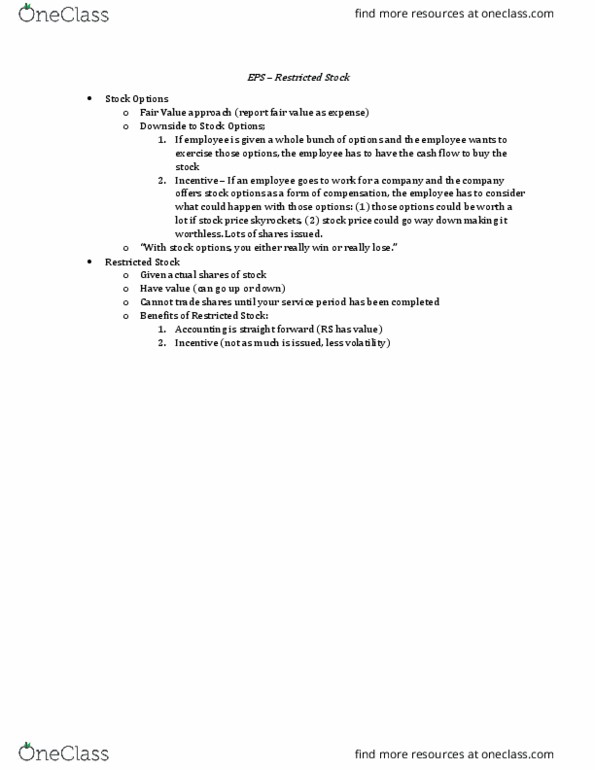

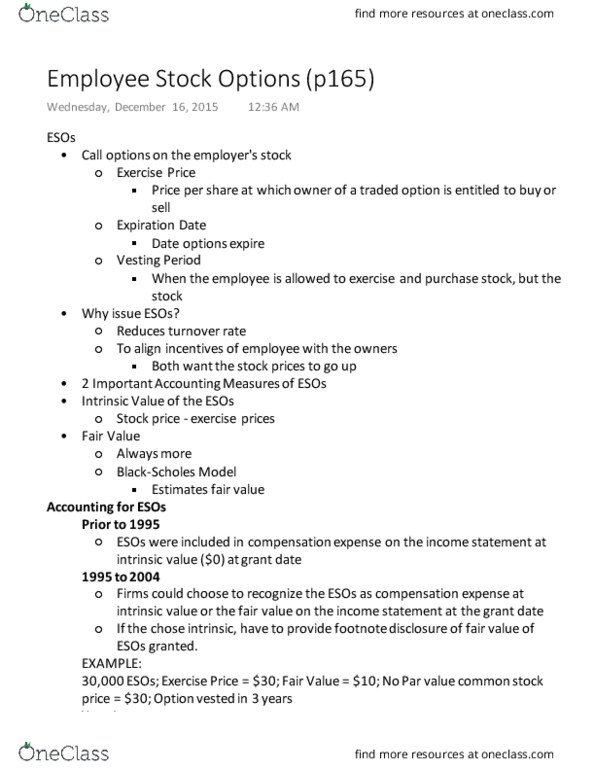

ACCT 361 Lecture 6: Stock Options

Get access

Related Documents

Related Questions

On January 1, 2014, Camp Co. grants options that permit keyexecutives to acquire 25 million of the companyâs $1 par commonstock within the next six years, but not before December 31, 2016[the vesting date]. The exercise price is the market price of theshares on the date of the grant, $10 per share. The fair value ofthe options, estimated by an appropriate option pricing model, is$3 per option.

1. | Determine the total compensation cost pertaining to the optionson 1/1/2014. |

2, | Prepare the journal entry at the Grant Date, 1/1/2014. |

3. | Prepare the appropriate journal entry to record compensationexpense on December 31, 2014. |

4. | Unexpected turnover during 2015 caused the forfeiture of 6% ofthe stock options, Determine the adjusted compensation cost andprepare appropriate journal entries on December 31, 2015 andDecember 2016. |

Walters Audio Visual, Inc., offers a stock option plan to its regional managers. On January 1, 2016, options were granted for 40 million $1 par common shares. The exercise price is the market price on the grant date, $8 per share. Options cannot be exercised prior to January 1, 2018, and expire December 31, 2022. The fair value of the options, estimated by an appropriate option pricing model, is $2 per option. Because the plan does not qualify as an incentive plan, Walters will receive a tax deduction upon exercise of the options equal to the excess of the market price at exercise over the exercise price. The income tax rate is 40%.

Required: 1. Determine the total compensation cost pertaining to the stock option plan. (Enter your answer in millions (i.e., 10,000,000 should be entered as 10).)

| 2. Prepare the necessary journal entries. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Enter your answers in millions (i.e., 10,000,000 should be entered as 10).) 1. Record compensation expense on December 31, 2016. 2. Record any tax effect related to compensation expense recorded in 2016. 3. Record compensation expense on December 31, 2017. 4. Record any tax effect related to compensation expense recorded in 2017. 5. Record the exercise of the options on March 20, 2021 when the market price is $12 per share. 6. Record any tax effect related to the exercise of the options. |