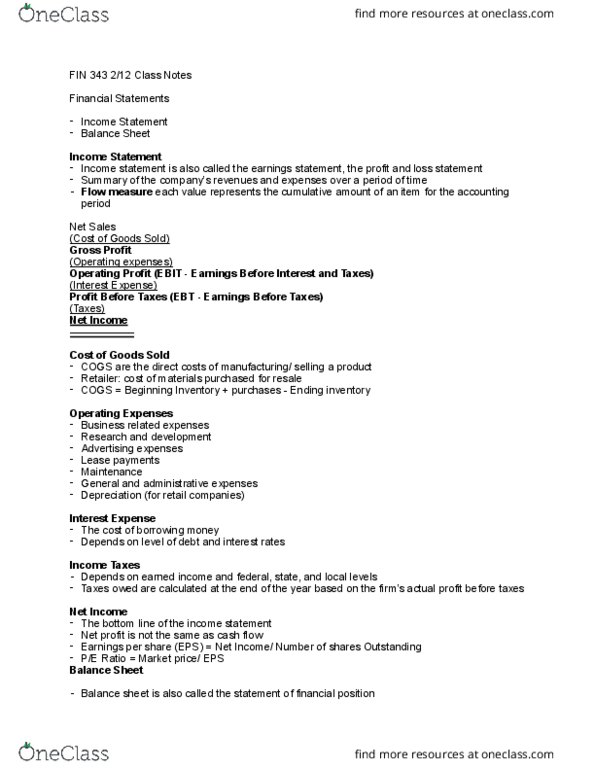

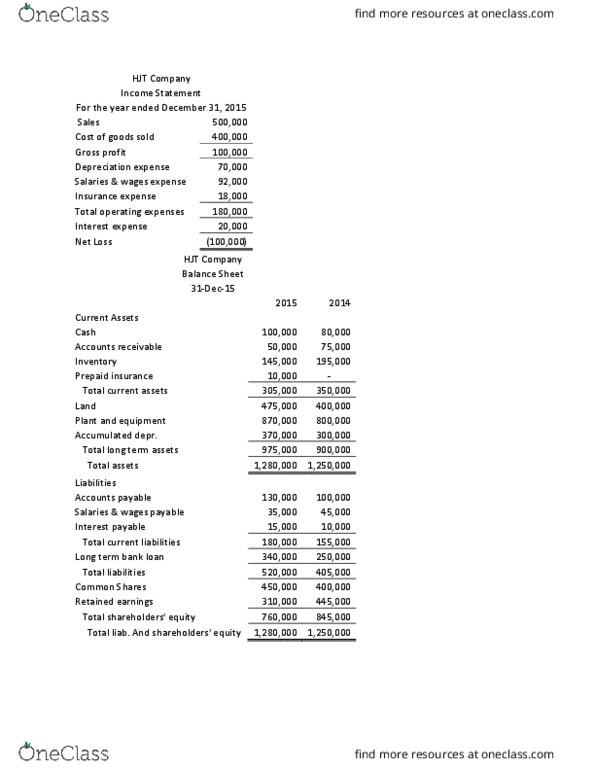

FIN 343 Lecture 3: FIN 343 2:14 Notes

Get access

Related Documents

Related Questions

The balance sheet and income statement shown below are for Pettijohn Inc. Note that the firm has no amortization charges, it does not lease any assets, none of its debt must be retired during the next 5 years, and the notes payable will be rolled over.

| Tax rate | 40% | |

| Stock price | $17.00 | |

| Shares outstanding | 3,800,000 | |

| Dividends are 50% of net income | ||

| Income Statement | ||||||

| Period Ending | 31-Dec-13 | |||||

| Total Revenue | 148,239,000 | |||||

| COGS | 118,094,000 | |||||

| Selling General and Administrative | 13,384,000 | |||||

| Depreciation | 72,000 | |||||

| Earnings Before Interest And Taxes | 16,689,000 | |||||

| Interest Expense | 829,000 | |||||

| Income Before Tax | 15,860,000 | |||||

| Income Tax Expense (40%) | 6,344,000 | |||||

| Net Income | 9,516,000 | |||||

| Balance Sheet | ||||||

| Date | 31-Dec-13 | |||||

| Assets | ||||||

| Current Assets | ||||||

| Cash | 14,468,000 | |||||

| Net Receivables | 98,359,000 | |||||

| Inventory | 18,758,000 | |||||

| Total Current Assets | 131,585,000 | |||||

| Property Plant and Equipment | 70,441,000 | |||||

| Total Assets | 202,026,000 | |||||

| Liabilities | ||||||

| Current Liabilities | ||||||

| Accounts Payable | 22,446,500 | |||||

| Accruals | 14,315,500 | |||||

| Notes Payable | 3,631,000 | |||||

| Total Current Liabilities | 40,393,000 | |||||

| Long Term Debt | 134,919,000 | |||||

| Total Liabilities | 175,312,000 | |||||

| Stockholders' Equity | ||||||

| Common Stock | 40,000 | |||||

| Retained Earnings | 26,674,000 | |||||

| Total Stockholder Equity | 26,714,000 | |||||

| Total Assets | 202,026,000 | |||||

| Question/Problem Calculate the common size balance sheet and the common size income statement for the company. | ||||||

Selected data for Kris Corporationâs comparative balance sheetsfor Year 1 and Year 2 are as follows:

| Year 1 | Year 2 | |||||||

| Assets | ||||||||

| Cash | $ | 100,000 | $ | (50,000) | ||||

| Accounts receivable (net) | 50,000 | 100,000 | ||||||

| Inventory | 100,000 | 250,000 | ||||||

| Equipment (net) | 300,000 | 350,000 | ||||||

| Total assets | $ | 550,000 | $ | 650,000 | ||||

| Liabilities and Equity | ||||||||

| Accounts payable | $ | 150,000 | 100,000 | |||||

| Income taxes payable | 80,000 | 30,000 | ||||||

| Bonds payable | 100,000 | 80,000 | ||||||

| Common stock | 100,000 | 200,000 | ||||||

| Retained earnings | 120,000 | 240,000 | ||||||

| Total liabilities and Equity | $ | 550,000 | $ | 650,000 | ||||

1. The change in the equipment balance would berecorded on the statement of cash flows as:

A) a decrease of $50,000 under investing activities.

B) an increase of $50,000 under investing activities.

C) a decrease of $150,000 under investing activities.

D) an increase of $150,000 under operating activities.

2. The change in the balance of the Bonds Payableaccount would be recorded on the statement of cash flowsas:

A) an increase of $20,000 under financing activities.

B) an increase of $80,000 under investing activities.

C) a decrease of $20,000 under financing activities.

D) a decrease of $80,000 under operating activities.

MG770- Financial Reporting, Financial Statement Analysis, andValuation

Homework Assignment

Week # 3

__________________________________________________________________________

Create the statement of cash-flow with indirectmethod

Interpret the result of the statement of cash flow withpercentage

Instruction:

[1] Please use the balance sheet as follows to classify eachactivity (operating, investing, and financing) from the column ofdifferent.

[2] please create a new statement of cash-flow from yourclassification on balance sheet.

[3] The statement of cash flow will be provided to measure thecompanyâs cash flow situation. Also, you need to interpret theresult of your measurement.

Balance sheet | ||||||

SILVERT CORPORATION | ||||||

Balance Sheet | ||||||

December 31 | ||||||

Different | Operating | Investing | Financing | |||

2012 | 2011 | |||||

ASSET | ||||||

Cash | $ 28,000 | $20,000 | $8,000 | |||

Receivable (net) | 70,000 | 62,000 | $8,000 | |||

Other current assets | 90,000 | 73,000 | $17,000 | |||

Long-term investment | 62,000 | 60,000 | $2,000 | |||

Plant and equipment (net) | 510,000 | 470,000 | $40,000 | |||

Total Assets | $760,000 | $685,000 | $75,000 | |||

LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||

Current liabilities | $75,000 | $70,000 | $5,000 | |||

Long-term debt | 80,000 | 90,000 | ($10,000) | |||

Common stock | 330,000 | 300,000 | $30,000 | |||

Retained earnings | 275,000 | 225,000 | $50,000 | |||

Total liabilities and stockholdersâ equity | 760,000 | 685,000 | $75,000 | |||

]2] Create the statement of cash-flow by using the indirectmethod. Company has net income as starting point of $80,000.

STATEMENT OF CASH FLOW

Operating Activities | |

Net Income | $ 80,000 |

Cashflow from Operations | |

Investing Activities | |

Cashflow from Investing | |

Financing Activities | |

Cashflow from Financing |