ACC 101 Lecture 4: Chapter 3 - Measuring Business Income_ Adjusting the Accounts

28 Jan 2019

School

Department

Course

Professor

Document Summary

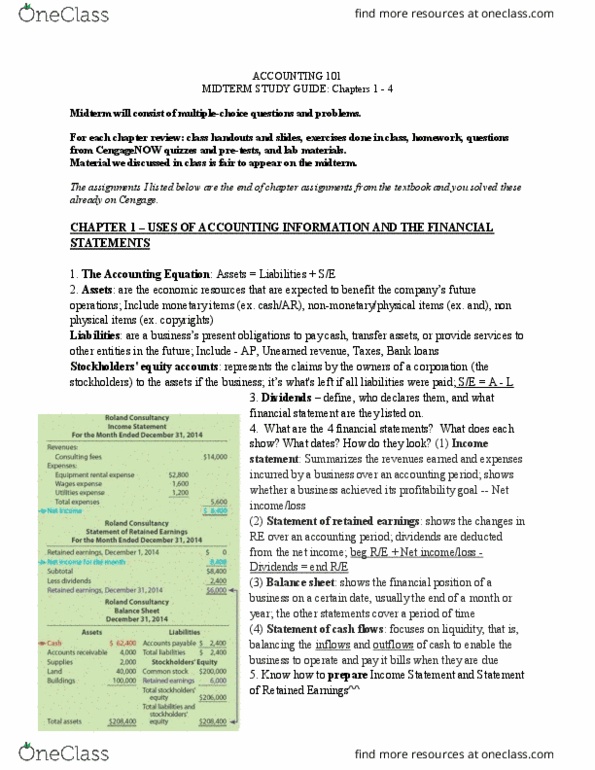

Chapter 3 - measuring business income: adjusting the accounts: 136 163. Lo 1define net income, and explain the concepts underlying income measurement. Lo 2distinguish cash basis of accounting from accrual accounting, and explain how accrual accounting is accomplished. Lo 3identify four situations that require adjusting entries, and illustrate typical adjusting entries. Lo 4prepare financial statements from an adjusted trial balance. Lo 5explain the importance of ethical measurement of net income and the relation of net income to cash flows. Net income - increase in stockholders" equity that results from a company"s operations. Revenues are increases in stockholders" equity resulting from selling goods, rendering services, or performing other business activities. Expenses are decreases in stockholders" equity resulting from the cost of selling goods or rendering services and the cost of the activities necessary to carry on a business, such as attracting and serving customers. Continuity - the difficulty associated with not knowing how long a business will survive.